")

My last article about Toronto-Dominion Bank (NYSE:TD) was published on November 27, 2023 and in the article I was cautious about the bank as a potential investment – as I was cautious about the entire banking sector in the last few quarters. In the meantime, the stock lost about 9% in value, and we can ask the question once again if the stock is now cheap enough to be a good investment.

Quarterly Results

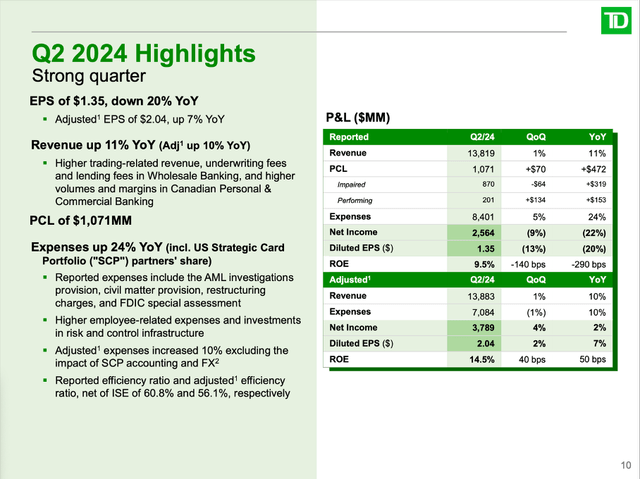

On May 23, 2024, the Toronto-Dominion Bank reported second quarter results for fiscal 2024 and the results were not bad but not great either. Total revenue increased from $12,397 million in Q2/23 to $13,819 million in Q2/24 – resulting in 11.5% year-over-year growth. However, diluted earnings per share declined from $1.69 in the same quarter last year to $1.35 this quarter – resulting in a 20.1% year-over-year decline. Adjusted earnings per share, however, increased 6.8% year-over-year from $1.91 in the same quarter last year to $2.04 this quarter.

TD Q2/24 Presentation

When looking at further metrics, we can look at total deposits, total assets, and total loans – all of which increased year-over-year and quarter-over-quarter. Total deposits in Q2/24 were $1,203.8 million – an increase of 1.9% quarter-over-quarter and an increase of 1.2% year-over-year. Total loans (net of allowance for loan losses) were $928.1 million this quarter, resulting in 2.6% quarter-over-quarter growth and 9.2% year-over-year growth. And finally, total assets were $1,966.7 million in Q2/24 resulting in 2.9% quarter-over-quarter growth and 2.2% year-over-year growth.

Valuation

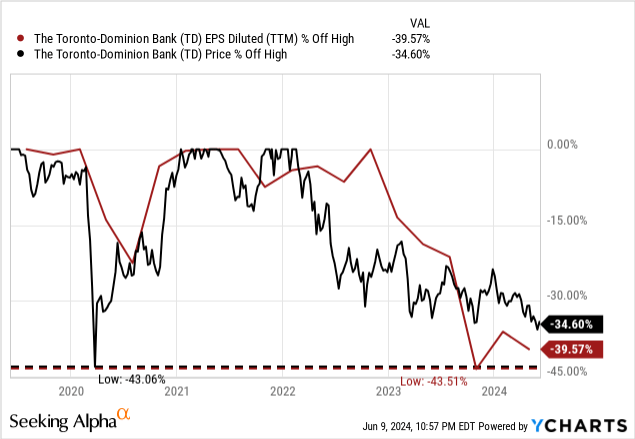

Aside from reporting more or less solid results for the second quarter, the low valuation and rather low stock price is still a strong argument for buying the stock. And as the stock is continuing to decline, it is also getting more interesting as an investment. The stock is now trading 35% below its previous high, and trailing twelve months earnings per share have declining 40% already.

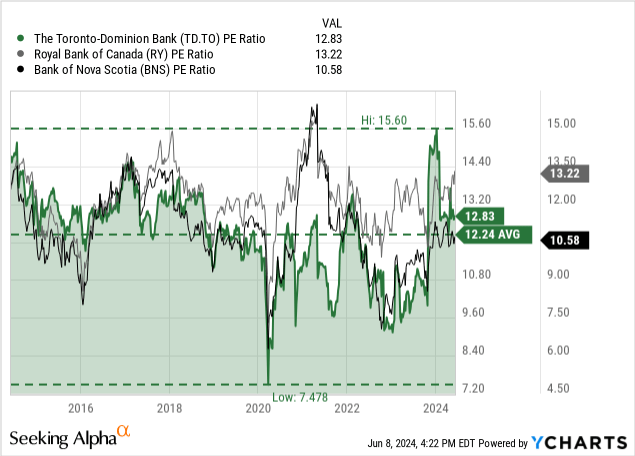

Due to the declining earnings per share, the stock is now trading for a higher valuation multiple than in the last few quarters. At the time of writing, the Toronto-Dominion Bank is trading for 12.8 times earnings and therefore slightly above the 10-year average of 12.2.

But we should not forget that banks overall are trading for extremely low valuation multiples (see valuation multiples for the Royal Bank of Canada (RY) and the Bank of Nova Scotia (BNS) in the chart). While the overall stock market is trading for a CAPE ratio of 21 in Canada and clearly over 30 in the United States, banks are often trading in the low double digits even if growth rates are in the mid-to-high single digits.

Dividend

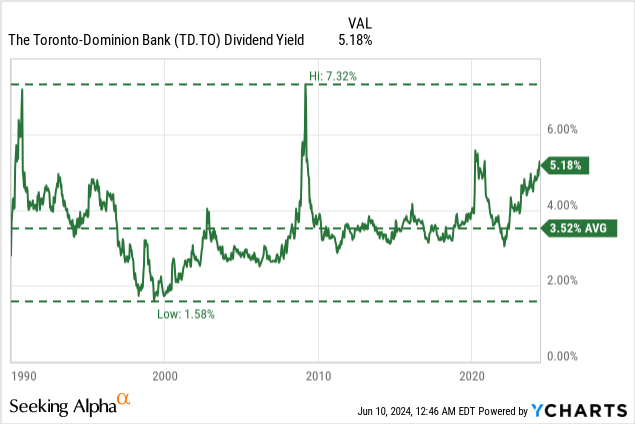

There is one more positive aspect worth mentioning – the dividend. Right now, the Toronto-Dominion Bank is paying a quarterly dividend of $1.02. This is resulting in an annual dividend of $4.08 and a dividend yield of 5.4% which is solid even in times of higher yields on treasury bonds. And although earnings per share have been declining, the dividend is still well covered and there is no reason to worry about a dividend cut right now. That being said, bank earnings can decline quickly resulting in a payout ratio well above 100% making the dividend not sustainable anymore. Additionally, banks often cut dividends in recessions – and this might happen again during the next recession.

Maybe we could argue that the Toronto-Dominion Bank is slowly becoming a “Buy” with a tempting dividend, but only under one condition. We should be as sure as humanly possible that the Toronto-Dominion Bank is able to weather every potential storm that might be coming. And for me, that is certainly a tricky question, almost impossible to answer – and you probably know that I rather stay on the side of caution.

Management Getting More Cautious

And while the solid results with revenue growing, the low valuation multiples and the high dividend yield are all compelling arguments, we should also look at some other important points and potential reasons why the Toronto-Dominion Bank maybe isn’t the best investment we can make at this point.

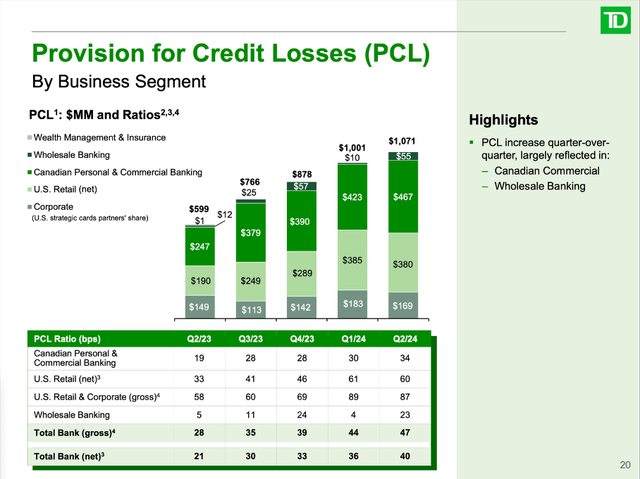

For starters, we can point out that management is getting more cautious. One of the reasons for the declining bottom line were the higher provisions for credit losses, which increased 78.8% year-over-year from $599 million in the same quarter last year to $1,071 million this quarter. And when looking at the chart we see management increasing provision for credit losses every single quarter in the recent past.

TD Q2/24 Presentation

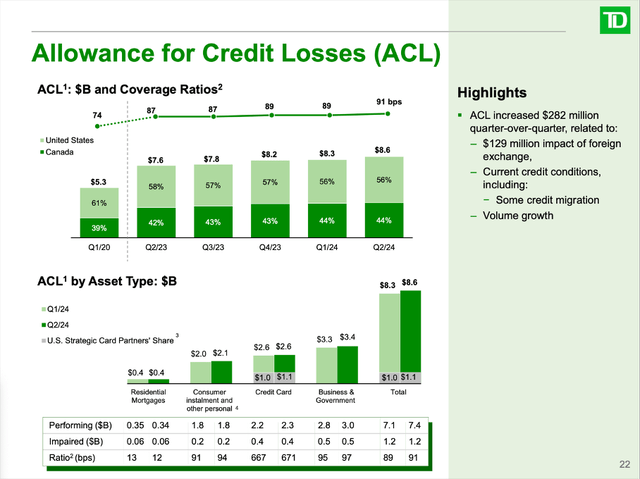

And hand-in-hand with an increasing provision for credit losses, allowance for credit losses also continues to increase from quarter to quarter. In Q2/24 it was $8.6 billion – resulting in an ACL ratio of 91 bps.

TD Q2/24 Presentation

And of course, this could be seen as positive as the bank is obviously trying to prepare for what is about to come and with higher amounts set aside for credit losses the negative effects might rather be limited, and liquidity problems can be contained.

When looking at the numbers in more detail, we see that the biggest part (56% of ACL) is set aside for loans in the United States, although loans made to customers in the United States make up only 34% of total loans. Canadian loans, on the other hand, make up 62% of total loans but only 44% of ACL is set aside for these loans. We can interpret these results as management considering the United States riskier than Canada at this point.

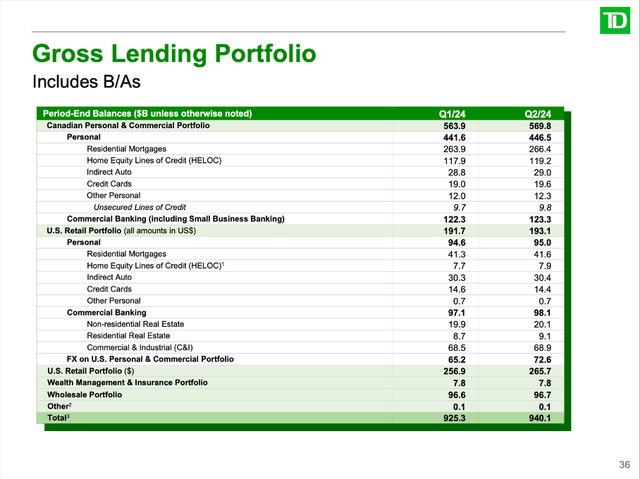

Aside from the discrepancy between loans in the United States and Canada, we also see that the Toronto-Dominion Bank only set aside $0.4 billion for residential mortgages, although these loans make up a huge part of the total loan portfolio. Residential mortgages in Canada are $266.4 billion and $41.6 billion in the United States, and together it is almost one third of the total loans. This is also telling us that management is seeing very little risk in residential mortgages at this point. Much higher risk is seen in business and government loans, with an ACL ratio of 97 bps and $3.4 billion in allowance for credit losses. And especially credit cards are seen as risky (but that is nothing new) and currently have an ACL ratio of 671 bps.

TD Q2/24 Presentation

So far, residential mortgages seem to perform quite well. And especially in the United States, the delinquency rate is surprising and at an extremely low level.

TD Q2/24 Presentation

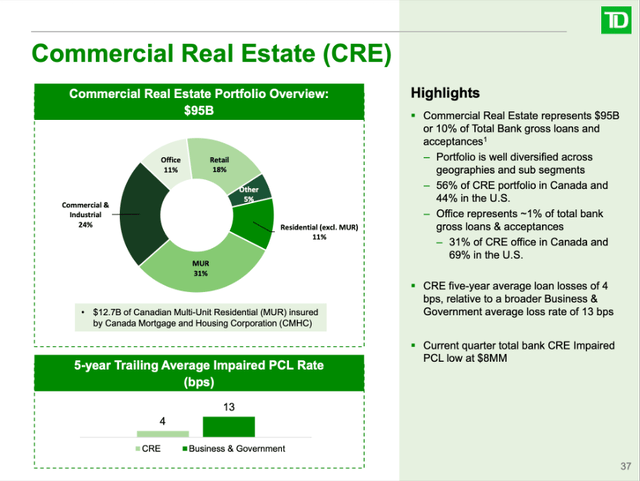

And in the last few months (and maybe quarters) the focus was rather on commercial real estate, which might create a problem for banks. The Toronto-Dominion Bank has a commercial real estate portfolio of $95 billion (about 10% of the bank’s total gross loans and acceptances). These loans are distributed between Canada (56%) and the United States (44%). And offices represent only 1% of total bank gross loans and acceptances, and the risk here seems to be manageable. Commercial real estate loans are in focus for good reason, but it seems like the Toronto-Dominion Bank can be excluding from the list of banks that have to be monitored closely for the CRE portfolio.

Overall Picture Getting Worse

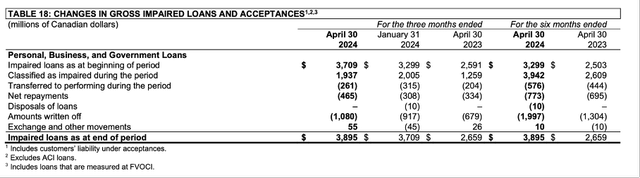

In my last article published in November 2023 I also looked at the amounts the Toronto-Dominion Bank had to write off. Back then, it was $687 million in the most recent quarter. However, in Q1/24 the Toronto-Dominion Bank already had to write off $917 million and in Q2/24 the write-offs were even $1,080 million.

TD Q2/24 Shareholder Report

Toronto-Dominion Bank also had to classify $1,937 million in loans as impaired during the last three months. In the quarter in which my last article was published, “only” $1,599 million in loans had to be classified as impaired and in the same quarter last year (in Q2/23) the amount was $1,259 million.

The tier 1 capital ratio of Toronto-Dominion also declined from 17.3% in the same quarter last year to 15.1% this quarter. And return on equity also declined from 12.4% in the same quarter last year to 9.5% this quarter. Summing up, there is certainly no reason to panic right now, and most reported metrics are still acceptable, but we see the situation slowly getting worse.

Situation in the United States

But not only when looking at metrics the Toronto-Dominion Bank is reporting, we see the picture slowly getting worse. When looking at reported metrics of the two major countries the bank is operating in – the United States and Canada – we see the picture also getting worse.

New York FED Credit Report

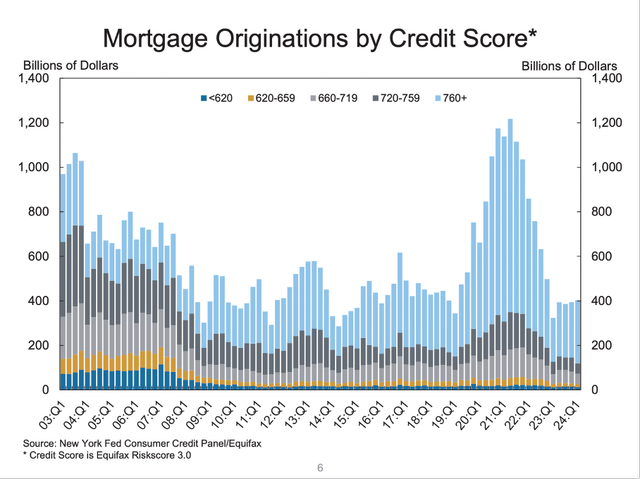

I mentioned above that only a fraction of allowance for credit losses is set aside for residential mortgages. This seems to go hand-in-hand with the delinquency rate reported in the United States. Despite a small uptick in the recent past, delinquency rates are at extremely low levels we haven’t seen in almost 20 years. And when looking at the mortgage originations by credit score, we see the subprime category (which contributed heavily to the Great Financial Crisis) is hardly playing a role today, which is a good sign. During the last few years, we saw a high origination volume of mortgages, but most of them were with a credit score of 760 or higher. I still would be cautious about the housing market, as the dangerous combination of high housing prices and rising interest rates is still out there. If we add rising unemployment rates (due to a recession) into the equation, it might turn ugly quickly. But so far, residential mortgages seem very resilient.

New York FED Credit Report

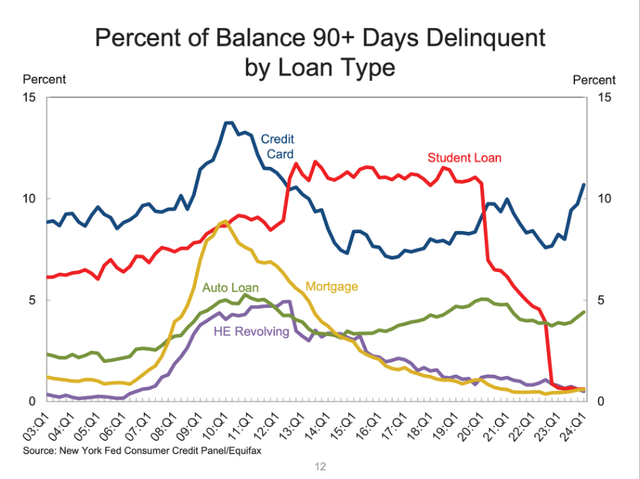

The bigger problem seems to be auto loans and credit cards. And of course, for student loans, we must see how the situations will be in a year or two. And in theory, delinquency rates for student loans could quickly be in the high single digits or even double digits again. At similar delinquency rates we also find credit cards (10.7% in Q1/24 and delinquency rates for auto loans are also increasing to 4.4% in Q1/24.

FRED

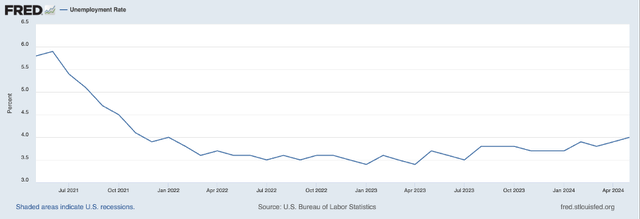

The unemployment rate is also slightly increasing over time. Compared to an unemployment rate of 3.4% in early 2022 the last reported number was 4.0%. Of course, this is still not a high unemployment rate (actually still one of the lower in history), but an increasing unemployment rate is not a good sign. Summing up, we are still nowhere close to delinquency rates or unemployment rates seen during the Great Financial Crisis, but the picture is slowly getting worse.

Situation in Canada

And in Canada, we also see metrics slowly getting worse. The unemployment rate in Canada is rising since mid-2022. Back then, the unemployment rate was 5.1% and over the last two years it rose to 6.1%. And the overall delinquency rate is also rising – from 0.14% in 2022 to 0.19% (latest reported number). However, these are still extremely low delinquency rates. And at this point we should remind everyone that Canada managed the Great Financial Crisis quite well, with the delinquency rate peaking at 0.45%.

Money Laundering Investigations

And there is one final topic we need to mention – the investigation about TD allegedly being linked to money laundering. In early May 2024 it was reported (among others by the Wall Street Journal) that international crime syndicates and drug traffickers used the Canadian bank to launder money. The company already reacted and has invested over $500 million to improve the company’s global anti-money laundering program. It hired recognized AML executives, onboarded hundreds of new AML professionals and deployed new enterprise-wide training.

During the last earnings call, management briefly commented on the situation and CEO Bharat Masrani made the following statement:

Before I get into the details, I want to spend a minute on our US AML program. As you read in the news release we issued on May 3rd, there were serious instances where the bank did not effectively monitor detect, report and respond to suspicious activity. Criminals are regularly targeting financial institutions. In these cases, TD did not effectively thwart their activity. This is unacceptable. TD has been cooperating closely with the authorities to help them prosecute these criminals. We have freely shared all information we have with the Department of Justice and other US regulators even when it demonstrated our weaknesses. As we advanced our own internal investigation, we took action against responsible employees, including termination where appropriate. Throughout, we strive to do what is right.

In my opinion, the accusations of money laundering are certainly important (for more information, A. J. Button wrote an extensive article on the subject) and something investors should consider. But compared to the risk of a recession, bear market and potential banking crisis, it seems not so relevant, and the risk and potential damage of a recession and banking crisis is more severe and can easily bring several banks to their knees.

Conclusion

Toronto-Dominion Bank is still taking one of the top spots in the list of banks I like to buy when I see the overall situation improve and when I am certain that a banking crisis either won’t occur or we can be certain that the Toronto-Dominion Bank will weather the storm.

But right now, I still see the risk of a recession and banking crisis as a major issue and the low valuation of Toronto-Dominion Bank and the high dividend yield is not enough to buy the stock. Of course, the stock is getting more and more interesting with declining stock price and at some price the risk-reward ratio is so compelling that we can buy the stock and take on the risk of a banking crisis. However, lower stock prices are necessary for that scenario.

Q2 2024 Earnings Call Transcript")