& Ethena (ENA) both pump 12% in 24 hours, but MAGA VP ($MVP) is the one with 1100x potential")

")

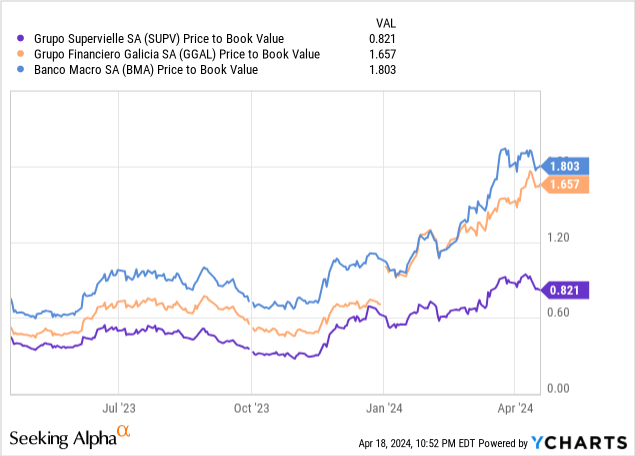

Even relative to its Argentine banking peers, many of which have also rallied quite significantly since the election, Grupo Supervielle S.A. (NYSE:SUPV) has been the standout. The next leg of the rally might not be quite as straightforward, however, with execution risk heightened after current CEO Alejandro Stengel’s surprise departure (see press release here).

Still, the overarching direction of travel, both at the macro and banking levels, is positive and assuming it continues, SUPV could be a very attractive ‘higher beta’ play on a recovery. Yes, SUPV stock has also re-rated quite significantly on the back of a Q4 report, helped mostly by securities gains rather than structural improvements. I don’t think expectations are all that high on a forward basis, though, at the current ~20% book value discount (vs 70-80% premia for its peers). Hence, faster-than-average earnings growth (off a very low base) and a higher return on equity (ROE) could still see the stock grind a lot higher. While playing the Argentina recovery via one of the bigger local banks like Galicia (GGAL) might be the safer bet (see Grupo Financiero Galicia: HSBC Argentina Acquisition Adds New Fuel To The Bull Case), investors looking for more risk/reward asymmetry should also find a lot to like with SUPV.

Management Reshuffle at a Turbulent Time

After four years at the helm and multiple senior stints in the last fourteen years, Supervielle has announced that current CEO Alejandro Stengel will vacate his position by the end of this year. Curiously, Supervielle does not yet have a successor, though is actively looking for a replacement. Whether Stengel remains as a Board member post-2024 or where future priorities lie now that the bank has “accelerated its journey towards a digital transformation and customer-centric operating model” remains to be seen. All eyes will also be on Patricio Supervielle, the key constant through all of this and still the Chairman and major shareholder, who will assist with the transition.

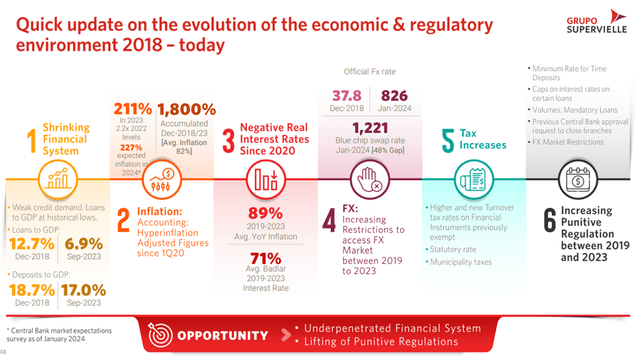

On the one hand, a management reshuffle now might not seem ideal given the heightened macro uncertainty post-election. But if recent developments are any indication (e.g., BCRA removing the minimum remuneration requirement for deposits), the operating backdrop for banks is set to change significantly – for the better. In the likely scenario that we also see Argentina’s macro stabilize further under President Milei, a multi-year ‘goldilocks’ period of deregulation and credit growth could well be on the cards. A vastly different economic and regulatory environment means a change at the top is perhaps justified – even if it adds execution risk to the Supervielle story.

Grupo Supervielle S.A.

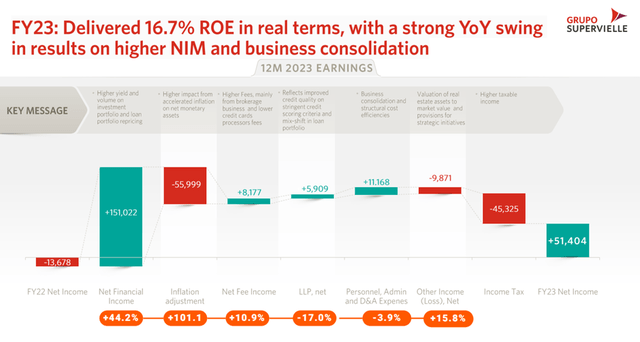

Ending 2023 on a High, with Help from One-Offs

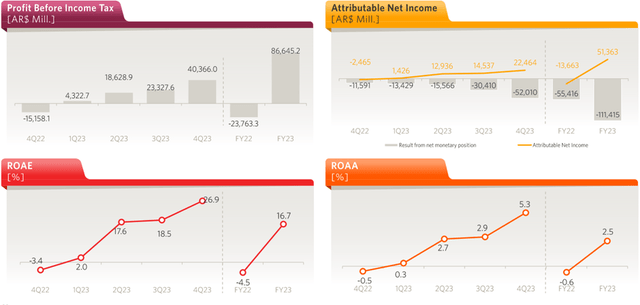

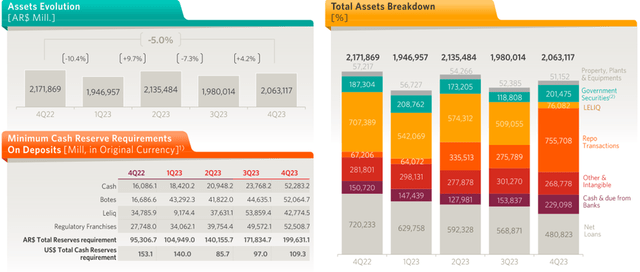

As for the fundamentals, Supervielle hasn’t yet shown as much improvement as you’d expect by looking at its stock performance. To recap, Q4 2023 did see headline net income get back to black (reversing last year’s net loss), though this was, to a large extent, due to one-off gains from Supervielle’s hedged balance sheet (against both currency devaluation and inflation) rather than any big structural improvements.

Grupo Supervielle S.A.

Still, the underlying numbers offer a solid foundation to work off, with real loan growth and deposits outperforming the industry – even if they were down sequentially (understandable given the macro turbulence). Net interest margins (NIMs) were relatively resilient as well, even net of the one-off currency gains and securities income. The result is a bank now delivering a significantly improved high teens percentage return on its equity base. While still below its cost of equity (likely around 20% after accounting for Argentina’s risk premia), the fact that Supervielle’s direction of travel has begun to turn before the benefits of Argentina’s economic/regulatory turnaround have kicked in is a big positive.

Grupo Supervielle S.A.

Near-Term Guidance Bar Keeps Expectations in Check

From here, management has set reasonable expectations, starting with peso loan growth running slightly above inflation for the full year – even after assuming a pick-up in the back half once the macro stabilizes. Peso deposits are also expected to increase at a similar ‘inflation-plus’ pace, so a stable near-term net interest margin outlook makes sense at face value. What management left out, though, is the potential for a massive cost of funding benefit following the BCRA’s recent decision to remove a regulatory minimum yield. Assuming we see more regulatory loosening from the central bank, I suspect there’s a lot more upside to both Supervielle’s NIM path and return on equity profile.

In the meantime, Supervielle, along with its banking peers, have made positive steps to adapt to the broader macro and fiscal turbulence, most notably by rebalancing the balance sheet away from Leliqs (i.e., BCRA-issued, local currency debt). Instead, the capital allocation focus has turned to alternative inflation and dollar-linked securities, essentially hedging the balance sheet against Argentina’s key macro risks. Given inflation is also still running hot (albeit below expectations), expect this hedging policy to add a nice boost to Q1/Q2 2024 results.

Grupo Supervielle S.A.

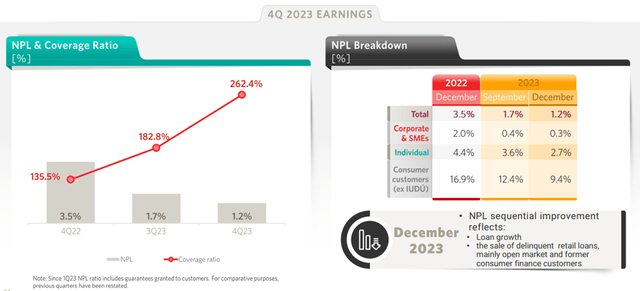

The bank also appears well insulated from any post-election fiscal consolidation impacts, with Q4 asset quality ratios remaining at low levels. This, in turn, leaves SUPV well-placed to capitalize on a future loan growth rebound – a very likely outcome in light of Argentina’s low credit penetration levels currently.

Grupo Supervielle S.A.

A ‘Higher Beta’ Play on the Argentine Bank Recovery

Execution risks are as high as they’ve ever been, but for investors with the right risk tolerance, SUPV represents an attractive play on Argentina’s latest regime shift. Supervielle might lack the scale, but given its higher leverage to credit growth in one of the most under-penetrated countries in LatAm, there’s arguably more earnings growth and, most importantly, ROE expansion potential here. Valuations are also less demanding, even after the big re-rating post-election, so the expectations bar is a lot lower here than for the big bank stocks. Key monitoring points going forward include further market-friendly regulatory updates by the BCRA, as well as the new administration’s progress on stabilizing Argentina’s broader macro instability.

Q1 2024 Earnings Call Transcript")