")

It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.

Despite the quote above being widely attributed to Mark Twain, scholars at the Center for Mark Twain Studies at Elmira College have found no evidence that he ever said or wrote it. Twain wrote something similar in his book Following the Equator, published in 1897, “Faith is believing what you know ain’t so.” Both quotes mean that ignorance, or things one does not know, is rarely the real problem. The true danger is false certainty or confidently believing something is true when it is not. Those mistaken “facts” lead one to poor decisions, errors, and even trouble. There are always dangers lurking in those predisposed to overconfidence, presumption, and the illusion of knowledge, particularly those who put their capital at risk in markets. Wisdom begins with recognizing when one might be wrong, rather than doubling down on flawed assumptions—it encourages humility, skepticism, and a willingness to change one’s beliefs when evidence contradicts them. Acknowledging gaps in one’s knowledge usually outweighs the errors from remaining stubborn but wrong.

On February 17, 2026, a massive avalanche hit a group of 15 backcountry skiers in the Sierra Nevada mountains near Lake Tahoe, California. The skiers were part of a guided three-day trip organized by a professional tour company that ventured into the backcountry to do “storm skiing,” a risky activity involving skiing fresh powder during or immediately after intense winter storms for the thrill of untouched snow, despite increased avalanche dangers. The incident occurred amid a powerful multi-day blizzard that hammered the region with heavy snowfall, high winds, and extreme cold. Forecasts indicated “high to extreme” avalanche risk due to unstable snowpack layers weakened by recent warm weather, followed by the rapid accumulation of new snow. The group consisted of experienced skiers returning from their outing when the avalanche triggered around midday, burying nine members under several feet of snow and debris.

Rescue operations started immediately but faced serious challenges due to ongoing storm conditions, including whiteout visibility, gale-force winds exceeding 60 mph, and additional snowfall of over two feet in some areas. Authorities located and evacuated six survivors that day, but ultimately, nine bodies were recovered by February 21. This tragedy was one of the worst single-incident avalanche disasters in the United States. The victims included a mix of locals and out-of-state adventurers aged 30 to 52, all with prior backcountry experience. The event highlighted the dangers of guided storm-skiing tours, with experts noting that although participants carried beacons, probes, and shovels, human factors like group decision-making under pressure likely influenced the outcome. While the group probably did not expect an avalanche, they understood the risks.

No one knows what triggered the avalanche; all one knows is that it occurred. Austrian economist Ludwig von Mises wrote that laws of probability do not govern human action. 1 He noted that when people act, they carry out plans in the realm of uncertainty: “Whether this was or was not the most appropriate plan depends on the development of future conditions which at the time of the plan’s execution cannot be forecast with certainty.” Mises further noted: “Future needs and valuations, the reaction of men to changes in conditions, future scientific and technological knowledge, future ideologies and policies can never be foretold with more than a greater or smaller degree of probability. Every action refers to an unknown future. It is in this sense always a risky speculation.”

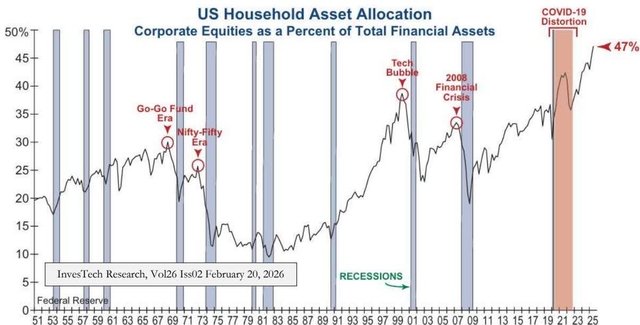

Just as investors often remain fully invested in an overvalued stock market, chasing short-term thrills at the expense of mounting risks, these backcountry skiers ventured into “storm skiing” amid blizzard conditions and explicit avalanche warnings. In both cases, psychology is driven by a mix of overconfidence, group dynamics, and a fear of missing out. The skiers, experienced and well-equipped, rationalized their decision through shared optimism or the guide’s assurance, much like market participants who remain “all in” during a bull market, betting on continued momentum despite fundamentals and valuations signaling caution. The outcome in the Sierras was catastrophic, with nine lives lost because the group pressed on despite the risk. Heading into 2026, many investors remain heavily allocated to a narrow set of popular stocks, lured by relentless gains and the familiar conviction that “this time it’s different.” The result is unprecedented: U.S. households now commit a greater share of their financial assets to equities than at any prior peak, including 1999. But the world is changing.

Following World War II, the U.S. Navy maintained unrivaled dominance over the world’s oceans. By patrolling key sea lanes, deterring threats from state actors and pirates, and ensuring freedom of navigation for all nations, regardless of alliances, the U.S. laid the groundwork for modern commerce with less operational friction, resulting in greater global economic profits. Reinforcing Pax Americana was the 1956 Suez Canal Crisis, a geopolitical clash rooted in regional tensions in the Middle East. The crisis erupted in July 1956 when Egyptian President Gamal Abdel Nasser nationalized the Suez Canal, a 120-mile waterway critical to global trade, which handled approximately 1.2 million barrels of oil daily via tanker and facilitated at least 8% of world seaborne commerce.

Completed in 1869 with support from Britain and France, the canal symbolized imperial legacies, as Britain maintained significant operational control despite Egypt’s nominal sovereignty. Prompted by the withdrawal of Western funding for the Aswan High Dam on the Nile River, Nasser seized the canal. In response, Israel invaded the Sinai Peninsula on October 29, 1956, which provided a reason for British and French intervention. Anglo-French forces launched airstrikes on October 31, followed by paratroopers and amphibious assaults, aiming to seize the canal zone and possibly overthrow Nasser. The operation, called “Musketeer,” was framed as a peacekeeping effort to separate the warring sides but was widely viewed as a colonial throwback meant to reclaim lost territory. The canal’s closure followed, with Egypt sinking vessels to block passage and disrupting trade for months. Diplomatic pressure increased at the United Nations, where the U.S. and the Soviet Union condemned the aggression. A ceasefire ensued on November 6, with British and French withdrawals completed by December 22, 1956, under the supervision of the UN Emergency Force. Egypt reopened the canal in April 1957, maintaining full control and collecting tolls that supported its economy.

The immediate economic impact included trade disruptions across Europe, with oil shortages prompting rationing in Britain and France. Freight rates surged up to 300%, intensifying inflationary pressures. For Britain, the crisis amplified preexisting frailties: post-WWII reconstruction burdened the country with $3.5 billion in dollar-denominated debt, while industrial competitiveness eroded against U.S. and German rivals. The United States, under President Dwight D. Eisenhower, wielded decisive influence, opposing the intervention amid Cold War calculations to court Arab nationalism and avert Soviet inroads. Britain sought U.S. support, including debt waivers, oil shipments, or loans, to defend the pound sterling, but Eisenhower’s administration conditioned the financial aid on compliance with the UN ceasefire. On November 6, as speculation intensified, the U.S. Treasury abstained from stabilizing interventions, allowing Britain’s reserves to dip dangerously low.

The crisis came to a head on December 3, 1956, when the International Monetary Fund (IMF) provided Britain with $561 million along with a $739 million standby credit, supplemented by U.S. Export-Import Bank loans. This resolution was predicated on Britain’s diplomatic retreat, highlighting its subordination to American financial architecture. While the intervention temporarily stabilized the sterling, it symbolized Britain’s debtor status and loss of autonomy. The crisis did not trigger an immediate collapse in Britain’s currency, but rather it initiated a gradual erosion of confidence—countries began diversifying their reserve holdings away from Britain. Trade invoicing shifted toward the U.S. dollar, and Britain endured recurring economic crises. The Suez Crisis served as a “stress test,” one that Britain failed, revealing how its overambition exposed its hidden vulnerabilities, and demonstrated U.S. dollar dominance. The episode highlighted how a hegemon’s status hinges on perceived invincibility, which can fracture suddenly.

The U.S.-Israel strikes on Iran beginning February 28, 2026, present some interesting parallels to the Suez Crisis, beginning with two allies overreaching against a sovereign state, provoking international condemnation, and growing economic strains. The current conflict also highlights an important structural change in warfare; controlling the sky is no longer the monopoly of the richer or more industrially advanced countries. In that context, this conflict likely casts a much longer shadow than the markets currently discount. This conflict could potentially change perceptions of U.S. military and economic hegemony, particularly regarding the dollar’s reserve status. Just as Suez exposed Britain’s vulnerabilities as a debtor and its dependence on U.S. goodwill, a protracted engagement with Iran only exacerbates U.S. fiscal strains, including its multi-trillion-dollar deficits. Perhaps without realizing it, the United States may have jeopardized its privilege of financing exponentially growing deficits with low interest rates.

Hopefully, this current conflict does not morph into the U.S.’s Suez moment, a possible inflection point at which the U.S.’s strategic hegemonic decline becomes apparent. Britain and France lost the Suez because they overestimated their own military and economic strength. For decades, investors have cited Middle East geopolitical risk and the Strait of Hormuz as critical risk factors. Now that risk has finally metastasized, markets shrug it off. If someone predicted six months ago that U.S. President Donald Trump would launch an oil embargo on Venezuela and snatch its president, collaborate with Israel to launch another preemptive strike against Iran; that Iran would respond by effectively closing the Strait of Hormuz, destroying numerous oil tankers, and bringing the war to every Gulf nation that hosts a U.S. military base; one would have reasonably assumed that global markets would be under far more stress than they currently exhibit.

According to Jeff Currie, Chief Strategy Officer of Energy Pathways at The Carlyle Group (CG), perhaps the real crisis is developing far from the Strait of Hormuz as markets realize that “oil is the rare earth of the macro system.” 2 Markets remain reassured that the world is less dependent on oil than it was in the 1970s. True, oil’s share of the global economy has fallen steadily for fifty years. That decline has made oil less expensive per unit of economic output (GDP) but more irreplaceable in function, according to Currie. In 1973, the American economy consumed 4.4 barrels of oil per $1,000 of GDP, but today it consumes just 0.25 barrels per $1,000 of GDP. 3 Fifty years of conservation have harvested the low-hanging efficiency fruit.

Today, there are no substitutes for the remaining barrels of oil demand: petrochemical feedstocks, aviation fuel, marine bunker fuel, and agricultural inputs. Remove these barrels of oil, noted Currie, and one does not get “demand destruction” but production shutdowns. When China restricted rare-earth exports, the threat was not the cost of a particular rare-earth metal, but rather that, without it, certain products could not be manufactured at any price. Oil and gas now sit at chokepoints in petrochemicals, aviation, shipping, power grid balancing, and fertilizer production that cannot be rerouted. The pricing consequence is not a gradual pass-through but rather a series of volatile moves, as the market must compensate for both physical scarcity and the irreplaceability premium.

Driving this point home, independent analyst and author Shanaka Anslem Perera described a scenario farmers are now facing: whether to plant corn or soybeans. Corn needs 180 pounds of nitrogen per acre. Nitrogen now costs $680 per ton on the CBOT May futures settlement, a jump of over 40% in a month. Soybeans fix their own nitrogen from the atmosphere through root bacteria called rhizobia—they need nothing from the Strait of Hormuz. Farmers will choose soybeans, and once the tractors roll into the fields to plant millions of acres, the choice cannot be reversed until next year. In February, the U.S. Department of Agriculture (USDA) projected corn acreage at roughly 94 million acres for 2026, down from 98.8 million acres in 2025, and soybeans at 85 million acres, up from 81.2 million acres. Those projections were published on February 19, before urea (nitrogen fertilizer) surged in price. 4

This process is the unfolding of the inflation transmission channel. The current conflict in the Middle East impacts the planting economics for 90 million acres of the world’s most productive farmland. Through the price of a single molecule that corn cannot grow without, and soybeans do not need, a series of events may potentially unfold. The EPA’s Renewable Fuel Standard mandates 15 billion gallons of corn ethanol annually, which consumes roughly 43% of the entire US corn crop. The EPA sets the mandate fourteen months in advance and does not deviate when corn acres shrink. 5 It is an inelastic demand consuming a fixed share of a declining supply. When supply tightens against an inelastic demand, corn prices rise. Higher corn prices squeeze every margin downstream; cattle, poultry, and pork operations face profit compression. Feed is the single largest cost in livestock production. When feed prices rise, protein prices rise. When protein is repriced, every grocery shelf in America absorbs the increase and passes it on to consumers at checkout.

For decades, the Efficient Market Hypothesis (EMH) has led to trillions of dollars flowing into passive investments, based on the belief that beating a broad index is impossible. The reasoning is that since thousands of analysts monitor the stock market, prices should already reflect all available information. However, the paradox is that the success of passive investing interrupts the very mechanism that initially made markets efficient. Today, the stock market operates within a self-reinforcing cycle where the main strategy is to keep pouring more money into the largest companies. This shift has systematically hindered price discovery. Currently, passive investment vehicles control nearly 60% of U.S. equity fund assets, up from only 6% in 1996. As a result, company-specific research is increasingly seen as unnecessary and outdated.

An efficient market used to mean that informed investors competed to find fair value. Now, passive investment funds buy indiscriminately, while a shrinking pool of active investors conducts price discovery. The concentration of passive investing may have unintentionally created the most crowded trade in market history. When millions own the same group of technology stocks in identical proportions through index funds, downside risk during a reversal is increased by the same mechanical process that pushed prices higher. In fact, it can be argued that when most of the market invests passively, it paradoxically makes the entire stock market more fragile, even though it might be a reasonable strategy for individual investors.

Nassim Taleb coined the term “antifragile” in his 2012 book Antifragile: Things That Gain from Disorder . He introduced the term because he could find no other word that captured the exact opposite of “fragile,” meaning, something that does not merely survive or resist disorder, but improves because of it. Taleb organizes the state of systems into three categories. A fragile system suffers from shocks, while a robust system remains unchanged and is unaffected by volatility and disorder. However, an antifragile system benefits from volatility, disorder, stressors, and randomness. An antifragile system gains and grows stronger when subject to stress. As Taleb succinctly summarized: “The fragile wants tranquility, the antifragile grows from disorder, and the robust doesn’t care too much.”

Using Taleb’s antifragile framework, one would initially see today’s stock market as robust, if not antifragile: the market always “rebounds.” An antifragile market grows stronger from small failures, asset mispricing, and company-specific shocks, leading to better capital allocation and a healthier overall market ecosystem. In contrast, a fragile system constantly suppresses volatility, allowing hidden risks and weaknesses to accumulate until a large shock triggers disproportionate damage. Taleb uses the classic analogy of how preventing small forest fires results in a buildup of tinder, eventually causing a catastrophic blaze. A healthy, antifragile market needs exposure to ongoing, decentralized trial and error. Active investors and analysts examine company fundamentals, sell overvalued or poorly managed companies, and direct capital toward stronger firms. This creates volatility at the individual-stock level—”small fires” that eliminate the weak while efficiently reallocating capital.

Passive strategies eliminate this feedback loop. Capital flows automatically into or out of entire indices based on inflows, outflows, or rebalancing, rather than on company-specific strength. Weak firms remain supported simply because they are in the index; overvalued large-cap stocks get mechanically bid up. Small corrective stresses are overlooked. Over time, misallocations and hidden leverage accumulate within the system. When a real shock occurs, such as a recession, a sharp shift in monetary policy, or a conflict in the Middle East, the correction becomes much larger and more damaging—just as Taleb warned about. A stock market dominated by passive investing does not benefit from chaos; it becomes fragile in its presence. Passive investing results in synchronized, monoculture-like behavior, even though complex systems depend on diversity.

By January 2026 the energy sector had shrunk to less than 3% of U.S. equity market value, while technology and services had grown to 53%. Passive flows have continually devalued energy and concentrated wealth in energy-consuming sectors, ironically, on the eve of another Middle East conflict. In the 1970s, energy stocks made up 25% of the S&P 500 Index (SPY) and offered a natural hedge. As oil prices increased, energy stocks climbed along with them, partially protecting diversified investors. Market participants view energy as a declining asset and technology as a perpetual growth engine. The Strait of Hormuz now challenges this efficient market hypothesis. Passive investing keeps reinforcing the “buy the dip” mindset, which has worked well for over two decades but has also increased market fragility. Widespread passive investing tends to homogenize the market—everyone essentially holds the same portfolio.

At an Allied checkpoint during the Battle of the Bulge in December 1944, U.S. General Omar Bradley was detained as a possible spy when he correctly identified Springfield as the capital of Illinois. The American military police officer who questioned him mistakenly believed the capital was Chicago. Bradley later jested about the incident, but it captured the surreal paranoia of the brutal winter, where even the right answer could lead to trouble. The prudent investor surveys today’s investment landscape and believes markets are fragile, whereas most market participants see them as efficient and antifragile. Only in hindsight will we know the “correct” answer, but we believe the investor remains best served by simply avoiding what the crowd is mechanically forced to own and capitalizing on underappreciated investment opportunities.

Value investors do not need to predict market movements. The same passive flows that have inflated the prices of the largest index constituents have simultaneously starved capital from well-run companies in sectors like energy, staples, industrials, and materials — businesses with real earnings power, durable competitive advantages, and valuations that reflect pessimism rather than fundamentals. By focusing on these overlooked companies, active value investors can acquire productive assets at a discount precisely because no index algorithm is bidding them up. The biggest risk today is the gradual realization among market participants that their expectations have been too optimistic and that current market levels will not deliver the promised investment returns. Slowly at first, passive investors may realize that they bid prices up too high and that, even in the best circumstances, these valuations will not generate the returns they expect. The opportunities, as always, lie where the crowd is not looking.

In a world filled with uncertainty, people often turn to experts for guidance, forgetting that expertise in a particular field does not guarantee good results. The ski guides who lost their lives in the snowslide were trained, certified, and experienced in avalanche detection and rescue, yet they and six of their clients perished just the same. The real danger is false certainty—thinking something is true when it is not. Overconfidence and the illusion of knowing can be risky, particularly for those risking their capital in volatile markets. Recognizing what one does not know is often better than stubbornly clinging to false beliefs that could affect one’s accumulated savings.

With kind regards,

St. James Investment Company

References

- Ludwig von Mises, “Human Action: A Treatise on Economics,” Page 105.

- Jeff Currie and James Gutman, “A Crude Awakening,” Carlyle, March 2026.

- https://www.eia.gov/dnav/pet/hist/LcalfHandler.ashx?n=pet&s=mttupus2&f=a

- Shanaka Anslem Perera, “The Nitrogen Trap,” Substack, March 16, 2026.

- Renewable Fuel Annual Standards | US EPA

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

")