")

")

Spotify Technology S.A. (NYSE:SPOT) released their Q1 FY24 result on April 23rd, meeting market expectations and sending the stock higher after the release. Recently, Spotify raised subscription prices in the U.S. for the first time since 2011. In addition, they cut their workforce to optimize the cost structure.

I am optimistic about their business growth and margin expansion trajectory in the near future, considering growth from both subscribers and price. I initiate with a “Strong Buy” with a one-year price target of $392 per share.

Price Increase & Layoff

Spotify had 9,646 employees in Q1 FY23, and they cut the total to 7,721 in Q1 FY24, indicating 20% year-over-year decrease. During the earnings call, management admitted that the workforce reduction caused more business disruptions than initially anticipated; however, they stated that their operations are back on track currently. I view the cost optimization as a positive move for Spotify, as it is likely to enhance productivity and maintain an entrepreneurial spirit within the firm. Of course, the layoff could enhance their operating margin in the near term.

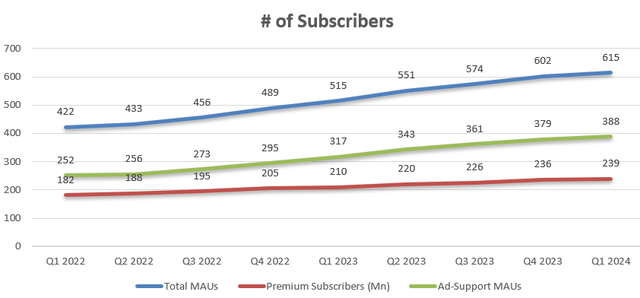

Their recent price increase attributed to 7% year-over-year growth in ARPU. As depicted in the chart below, the total number of monthly active users increased by 19.4% year-over-year, and the total number of premium subscribers was up 13.8% year-over-year. The price increase hasn’t affected their subscriber growth, at least for now.

Spotify Quarterly Results

Growth From Advertising

Ad-supported revenue only accounts for around 13% of total revenue; however it has been outpacing overall revenue growth lately. As illustrated in the chart above, Spotify has experienced rapid growth in Ad-support MAUs. For Spotify, Ad-supported service is a different business model, charging zero subscription fees but generating revenue from advertising businesses.

The Ad-supported service is not something new in the streaming industry. For instance, both Netflix (NFLX) and Disney (DIS) have introduced ad-supported streaming services to broaden their potential customer base.

In February 2021, Spotify launched the Spotify Audience Network (SPAN), an audio advertising marketplace that connects advertisers to listeners. I think their SPAN network is a very efficient and powerful platform for target marketing in the audio/music industry. Spotify has vast amounts of data to understand their subscribers, including their preferred music genre and the artists they follow.

As a result of multi-year investments, Spotify’s advertising business has experiencing robust revenue growth over the past quarters, increasing by 17% in Q4 FY23 on a constant currency basis, followed by 19% growth in Q1 FY24. I anticipate Ad-supported business will continue to outpace overall business growth in the near future.

Recent Result and FY24 Forecast

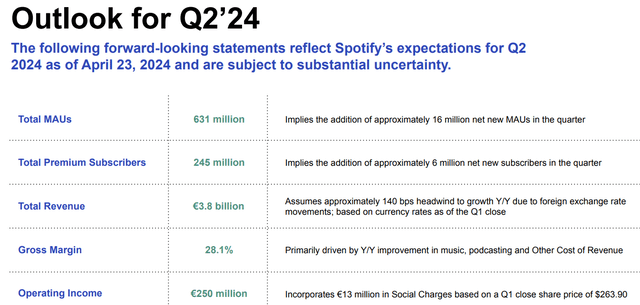

In Q1 FY24, the total revenue increased by 21% in constant currency, and the company anticipates the revenue will grow over 22% in Q2 FY24. My biggest takeaway from the quarter is their management’s confidence in the improving margin and cash flow from operations.

Spotify Investor Presentation

They delivered a record high gross margin of 27.6% in Q1 FY24, and plan to reach 28.1% in Q2 as illustrated in the slide above. The improving gross margin is driven by disciplined content spending, as indicated over the conference call. Spotify provides various types of revenue sharing model: direct revenue share, per-user model, and per hour model. With different revenue sharing models, Spotify can optimize their content costs leveraging their data analytics results.

Spotify generated EUR 207 million of FCF in Q1 FY24, a big improvement from the level of EUR 57 million in Q1 FY23. The primary driver for their FCF growth is their margin improvement and revenue growth in my view. As the company continues to focus on cost management, their cash flow generations may potentially continue to improve in the near future.

For FY24’s growth, I am considering the following factors:

- Industry Growth: BusinessWire forecasts the music streaming market will grow at a CAGR of 13.57% from 2022 to 2026. Spotify is the dominate player with 239 million premium subscribers, representing around 31% of total market share according to Musical Pursuits report. I think the industry growth is primarily fueled by the ongoing market transition from physical records to digital streaming. In addition, the availability of Ad-supported music streaming is attracting new listeners to the market, in my view.

- Price Increase: The $1 dollar price increase presents a 10% increase year-over-year. Spotify’s ARPU growth will get a boost in FY24 due to the recent price increase. However, it is just a one-time event, and investors should not anticipate the similar additional growth to occur in the near future.

- Advertising Growth: The Ad-supported revenue represents around 13% of total, and assuming it grows at 20%+, the business could contribute 2%-3% of growth to the topline.

As such, I assume 7% ARPU growth in FY24, 11% growth from subscriber growth, 2% growth from advertising, the combined revenue growth is expected to be around 20% in FY24. For FY25 and beyond, I adjust the ARPU growth rate to 2% to align with the overall inflation, resulting in a projected revenue growth of 15%, according to my calculations.

Valuation

For the operating margin, my considerations are as follows:

- Sales and marketing expenses: Spotify reduced their marketing expenses in FY23 to address macroeconomic uncertainties. The company has been seeking a balance between marketing expense growth and revenue growth. As communicated over the earnings call, they are going to increase some marketing spending in Q2; however, they won’t return to the heavy spending pattern seen before FY23. Spotify spent 11.6% of total revenue in sales and marketing in FY23, compared to 13.4% in FY22. When their business scales, the company is expected to generate some operating leverage from sales and marketing expenses, in my view.

- Gross Margin: as discussed previously, Spotify continues to optimize their content cost structure, and they are on the right track to expand their gross margin. Considering their advantage of data insights, I think Spotify is well positioned to expand their gross margin through content cost optimization.

- Price Increase and Layoff: the ARPU increase, and layoff could benefit their gross margin in FY24. But as mentioned, it is a one-time event.

I assume 100bps margin expansion for gross profits, 20bps leverage from R&D, and 30bps leverage from sales and marketing. Based on my calculations, the total operating expense will grow by 13.3% annually.

Spotify DCF – Author’s Calculations

I estimate the free cash flow from equity by adjusting the net income with depreciation/amortization, net change in working capital, and net borrowings.

Spotify FCFE- Author’s Calculations

The cost of equity is calculated to be 14.4% assuming: risk-free rate 4.32% (US 10Y treasury yield); market risk premium 7%; beta 1.44 (SA’s DATA). After discounting all the future FCFE at the rate of 14.4%, the one-year price target is calculated to be $392 per share.

Risks

New CFO: Spotify announced the appointment of Christian Luiga as the new CFO on April 4th 2024. Christian plans to join Spotify in Q3 FY24. As Luiga’s experience was in the defense and security industry, I expect he will need some time to familiarize himself with Spotify’s business model.

Competition from Apple, Amazon and Others: While Spotify holds the largest market share in the music streaming market, Apple (AAPL) and Amazon (AMZN) are significant competitors. Apple possesses the advantage of a massive smartphone user base, and Amazon can capitalize on their Prime subscriber base.

Musical Pursuits Report

Licensing Agreements: Spotify has the agreements with three major music companies: Universal Music Group, Sony Music Entertainment, and Warner Music Group. According to FY23 10K, these licensing agreements represent 74% of streams of audio content. When Spotify renews these agreements, they will negotiate the terms with these music companies, and any pushback from music companies would potentially pose some near-term risks for Spotify’s streaming services.

Conclusion

I am bullish on Spotify Technology S.A. due to their leadership position in the music streaming industry, ongoing cost optimization initiatives, and the capabilities of price increase and subscriber growth. I am optimistic about their margin expansion and free cash flow growth in the near future. Therefore, I initiate with a “Strong Buy” rating with a one-year price target of $392 per share.

")