Q1 2024 Earnings Call Transcript")

")

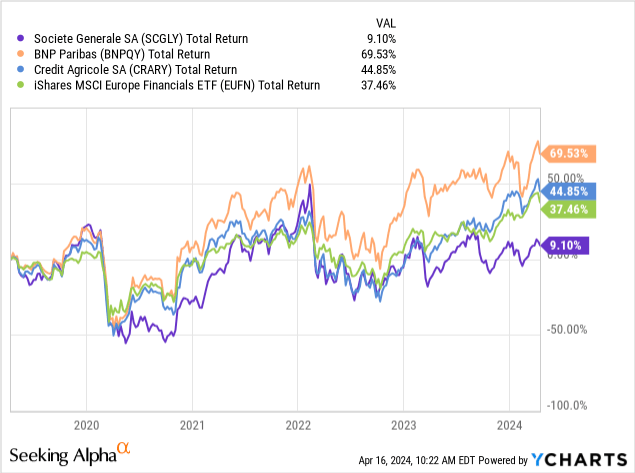

French universal banking giant Societe Generale (OTCPK:SCGLY)(OTCPK:SCGLF) (‘SocGen’ hereafter) has been a weak performer in recent years, meaningfully lagging both close French peers as well as the wider European financial space (EUFN) in that time. Indeed, SocGen’s share price remains lower than it was five years ago, with the stock de-rating from a then-valuation of around 0.5x prior-year tangible book value to less than 0.4x currently.

While the long awaited return of positive interest rates in the Eurozone may otherwise have provided a tonic for the bank’s ills, French retail banks, and SocGen in particular, have not been major beneficiaries. In fact, 2023 was a disastrous year for SocGen’s domestic retail business due to a combination of market and company-specific factors. As a result, the bank’s return on tangible equity (“RoTE”) remains heavily depressed in the low single-digit region, even as many of its continental peers saw RoTE surge on the back of much stronger interest rate sensitivity.

SocGen’s issues are also reflected in relatively tepid medium-term financial goals, with management only aiming to clear a 9-10% RoTE by 2026. While even this modest target looks ambitious, the stock’s current valuation more than reflects this, offering investors upside even if the bank ends up falling short of its goal. With a rebound in the domestic retail bank looking likely this year, I think the worst for SocGen is behind it, and I open on the bank with a ‘Buy’ rating.

SocGen Overview

SocGen reports through three core businesses, namely French Retail, Private Banking and Insurance (~30% of 2023 net banking income excluding the corporate center)(“FRPBI”); Global Banking and Investor Solutions (~37%)(“GBIS”); and International Retail, Mobility and Leasing Services (~32%)(“IRMLS”).

FRPBI largely explains itself. GBIS houses the bank’s trading, investment banking and securities services (e.g. custody, fund administration etc.) businesses. IRMLS is something of a catch-all segment that includes SocGen’s international retail banks, where it operates franchises across Africa and Eastern Europe. It has leading shares in select francophone African markets (e.g. Senegal, Cameroon and the Ivory Coast), and is #3 in more mature CEE markets like the Czech Republic and Romania. This business also includes Ayvens, SocGen’s majority-owned international vehicle leasing and fleet management business.

Domestic Retail Results To Improve

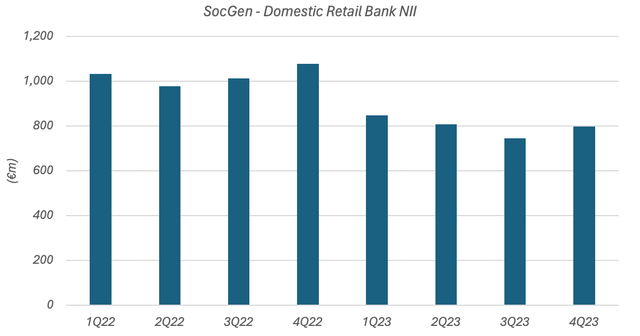

2023 was not a good year for SocGen, with the bank generating a meager RoTE of just 4.2%. While all of its core businesses faced headwinds, particularly in the latter half of the year, the French retail banking business was the worst performer, with reported net income declining from €1.4 billion in 2022 to just €610 million last year. Given that 2023 generally offered banks a very nice combination of higher interest rates and still-excellent credit quality, this was a major disappointment.

While cost of risk was indeed resilient in SocGen’s domestic retail unit, unchanged year-on-year at ~20bps of total lending, the top line was a major headwind, with FRPBI net banking revenue falling 13% last year to just over €8 billion. This was driven by very weak net interest income (“NII”).

Data Source: SocGen Results Releases

With Q1 2024 results a couple of weeks away, it is important to note that the structural and SocGen-specific issues that drove this poor result are both fading. In terms of the latter, SocGen has faced generic headwinds that pretty much all banks have faced in recent quarters, such as deposit migration from demand accounts to more expensive term accounts. In Q4 2023, SocGen reported around €138 billion in FRPBI sight deposits, down around 20% on the Q4 2022 level, while term balances had increased by around 70% to just under €60 billion over the same period. This trend should ease now that rates have topped out, with the bank guiding for a ~3ppt drop in sight deposit share of total deposit balances this year.

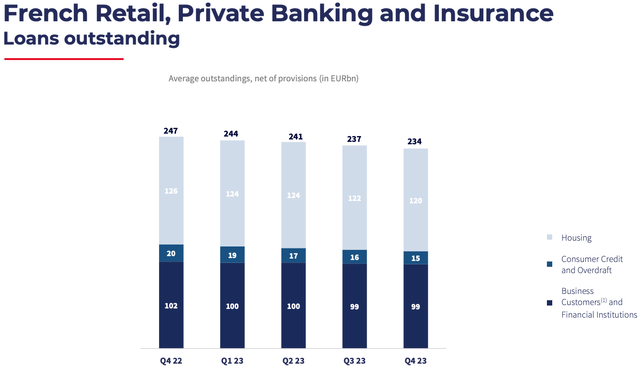

The bank has also faced some France-specific issues, chiefly in the form of regulated rates on certain savings and lending products. For instance, the legally-binding usury rate essentially caps the APR for various French loan types, including residential mortgages. Housing loans constitute around half of total loans in SocGen’s domestic retail unit.

This type of regulation has various effects, one of which is to severely limit short-term interest rate sensitivity. It has also led to a fall in loan balances, as margins in mortgage lending in particular have been squeezed hard by this dynamic. Housing loans in the FRPBI unit were down around 5% year-on-year in Q4 2023. I would also note that, as French mortgages are typically fixed for the duration of the loan, a large portion of FRPBI’s book will not have repriced to the higher rate environment, acting as a further headwind to NII. As regulated savings rates have been capped over the near-term, pressure on spreads and NIM should ease this year.

Source: SocGen 2023 Results Presentation

While the above sets out issues that all French retail banking businesses face, SocGen’s performance has been much worse than peers. For example, BNP Paribas (OTCQX:BNPQY)(OTCQX:BNPQF) saw roughly flat revenue last year in its domestic retail banking segment, with Credit Agricole (OTCPK:CRARY)(OTCPK:CRARF) performing similarly. In contrast, SocGen reported a ~13% decline in FRPBI revenue last year.

The driver of this relative underperformance was short-term interest rate hedges the bank took out back in 2022 before rates increased. These hedges will mature this year, resulting in meaningful net interest margin (“NIM”) expansion. Because the bank will only lap the worst affected quarters later in 2024 (around Q3), comps will be strong even if interest rate cuts materialize as expected. As with the Fed in the US, rate cut expectations have moderated in the Eurozone recently, albeit the forward curve is still pointing to around 75bps of cuts this year.

Hitting Medium-Term Targets Not Necessary

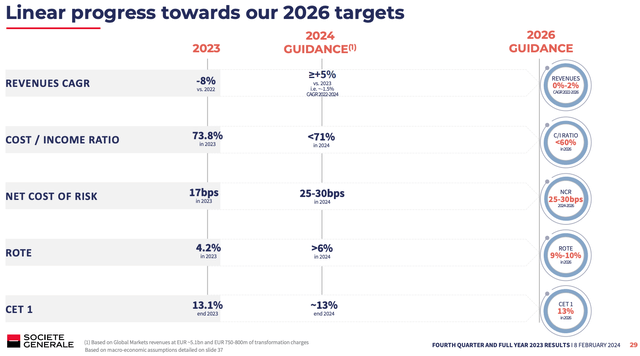

In broad terms, SocGen has two profitability targets: to generate a near-term (i.e. 2024) RoTE of around 6%, rising to 9-10% over the medium-term (2026). French retail banking should materially lift 2024 results as around €1 billion in lost NII should reappear this year. Other drivers of guidance, including a €500 million year-on-year fall in trading revenue, appear suitably prudent. I am also hoping that investment banking revenue sees a boost from better year-to-date industry performance.

SocGen’s longer-term profitability target looks slightly more challenging. With the low-end of revenue targets (0-2% CAGR growth) pointing to a static top line, management is relying on cost cutting to drive higher RoTE, targeting around €1.7 billion in gross savings by the end of that period. This is seen pushing the bank’s cost/income ratio below 60%, implying cost cuts can drive SocGen from being below average (versus European banks) to above average in terms of efficiency, all while keeping revenues at least flat. This looks like a big ask to me.

Source: SocGen 2023 Results Presentation

Importantly for investors, the market is not taking these targets at face value, with SocGen’s current share price of €24.26 (~$5.20 per ADS) equating to just under 0.4x tangible book value per share (“TBVPS”). That is commensurate with the mid-single-digit RoTE it should earn this year.

This looks like a good deal for investors. One reason why SocGen’s multiple remains depressed is that the bank’s 40-50% total payout ratio (balanced between cash dividends and stock buybacks) only corresponds to mediocre capital returns potential, roughly implying a 7% yield based on a 6% RoTE and 0.4x TBVPS multiple. Given its limited growth plans, this payout ratio appears much too low, but it is a result of the bank also seeking to beef up its capital ratio. Hitting this should unlock a higher level of capital returns from 2026.

Based on the implied level of retained earnings and around 3% per annum from buybacks, I would be looking for around 6-7% annualized balance sheet growth over the next three years (i.e. 2024-2026) on a per-share basis. Because SocGen’s RoTE profile is below its cost of equity, growth essentially destroys value and acts as a headwind to multiple expansion. Even so, factoring in around 1% annualized growth, a ~6% RoTE and an ~11% cost of equity gets me to a terminal TBVPS multiple of ~0.5x. This will end up higher if SocGen hits management’s 2026 RoTE target, though as per above this is not my base case. As SocGen should be in a position to ramp up capital returns by 2026, I see this as the catalyst for a modest re-rate.

The above gets me to a three-year price target of roughly €38 per share (~$8.10 per ADS at current FX), supplemented by roughly €3 per share in cash dividends for a ~€41 per share total return price (~$8.75 per ADS). With this implying ~20% annualized returns from the prevailing quote, I view SocGen as being cheap enough to offset both its lackluster current RoTE and the significant probability that it fails to hit management’s medium-term target. As such, I open on the stock with a ‘Buy’ rating.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")