")

Sega Sammy (OTCPK:SGAMY)(OTCPK:SGAMF) is one of our favourite ideas in the gaming space, which we’ve been covering for a year now. In our last article we focused on Pachinko, but now we are focused on the gaming and entertainment segment, which has been the reason for underperformance. We like Sega because it’s the discount Nintendo (OTCPK:NTDOY). It has strong franchises, but isn’t quite as consistent as Nintendo, which can almost do no wrong with Zelda and Mario continuing to lead their categories and impress critics and audiences. We hope for improvement, and indeed there is quite a lot going on. In chats with IR, the company has acknowledged that they are fully aware that newest titles from Creative Assembly, their UK studio famous for the Total War franchise, are not good. The audience rightfully thinks Pharoah was a lazy reskin. Creative Assembly was also responsible for HYENAS, which was a terrible idea to release a live-service shooter in an era where the space cannot possibly be more saturated. It had an interesting heist angle, and some beta testers even liked it, but despite being an already finished game with all money to develop it already spent, it was canned on the eve of release because apparently marginal benefit was exceeded by the marginal costs of running that live service game. The company is restructuring these underperforming businesses.

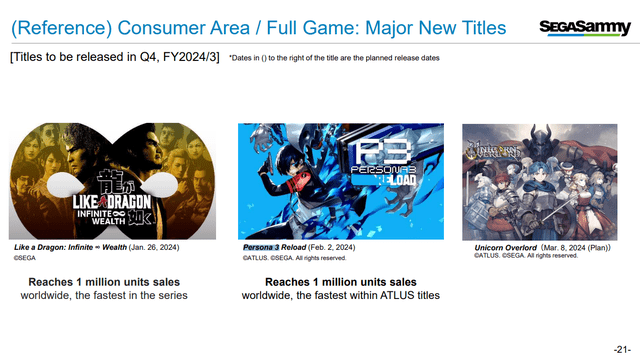

On the positives, Sega released two Yakuza games, both of which were loved by audiences and provided superb value. Particularly, the massive Infinite Wealth was released and will contribute to the Q4 results, along with the Persona 3 remake. Both games have achieved millions in unit sales. Sega Sammy has been underperforming due to downward revisions of forecasts, and that matters in Japan where market participants focus closely on income statements and earnings management. In addition to the fundamental discount, which attracts us as value investors, we think that Infinite Wealth and Persona 3 may over-perform and help beat the downward revised forecasts.

Forecasts for the FY

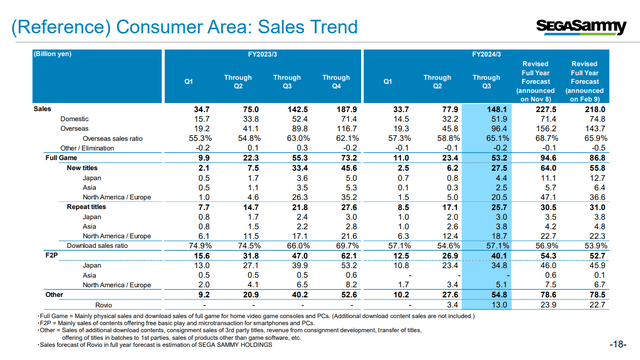

Likely the key impact on the stock comes from the changes in forecasts, where shortfalls in the entertainment business are driving overall downward revisions in FY operating income. Particularly, new title shortfalls are where the issues lie, not in repeat titles which seem to be performing well.

Headline Results (Q3 PR)

The new Total War: Pharoah, Sonic Superstars and Endless Dungeon were apparently the elements that were driving the declines in the forecasts by having sluggish sales. Note that overall like for like sales are still expected to rise, just not operating income on account of the restructurings. Relative fatigue with Total War titles and failure to include what the market wants has hit the franchise, and Sonic Superstars made a fatal mistake of releasing in the same week as Super Mario Wonder. We were already aware of the failure of Sonic Superstars, and assumed markets were as well and never had the game pegged for massive sales.

The Yakuza Gaiden game was well liked and released within Q3, but Infinite Wealth came out after the quarter close in January, and will reflect in the Q4 results only. It massively outperformed our forecasts, already selling a million across all platforms. Our estimate was that it would sell 357k in the first month, and around 700k in the first 6 months. It has already hit 1 million, and likely will hit more than 2 million over the next 6 months. The rule of thumb is that 40% of the unit sales occur in the first month, 80% in the first 6 months. Of course, prices also start to get discounted further out from release.

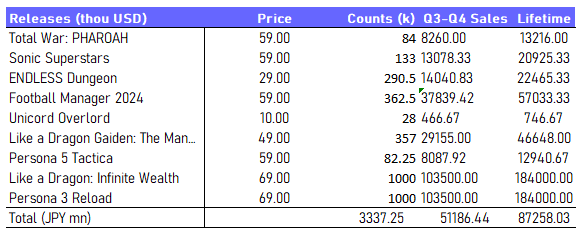

Our H2 Forecasts Based on standard game sales distributions (VTS and SGAMY Disclosure)

Using the updated figures, we can see what needs to happen in new releases to hit figures. To explain the above table a bit better, we use distribution of sales assumptions from release dates to build these figures, along with decays in prices as games become more likely to be purchased at discounts away from release. Lifetime sales column is self-explanatory, but the Q3-Q4 sales are the forecasts for six month performance of the games towards the close of the FY. Q3 releases have already happened, so the wildcard is still the Q4 and that is where a beat may happen. The counts column is how many games were estimated to be sold across all platforms in the first month, from which all the other forecasts are imputed. We adjust for games that only have single platform release and so forth, and we use the data on SteamDB to imply overall first month download counts – so there is room for error there since the SteamDB data is also an estimate.

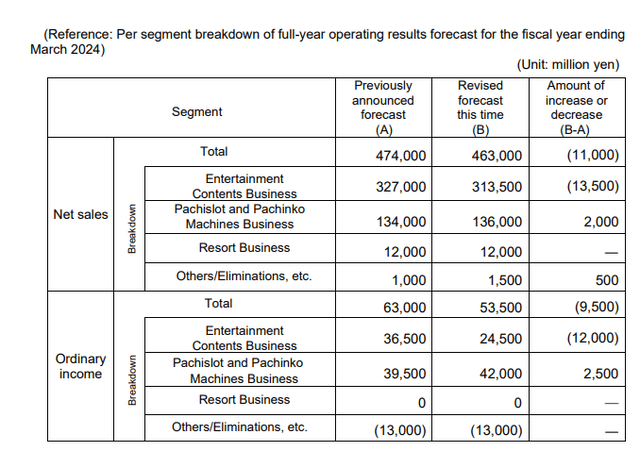

Consumer Segment Forecast Revisions (Q3 Pres)

From Q3 cumulatives, there needs to be a 37 billion JPY performance in new titles in order to hit the previously announced forecasts in November, and that’s the performance that is required in Q4. As of the previous Q2 figures, where our estimations are for a 6 month and not a quarterly period, the benchmark for new titles according to this chart is around 58 billion JPY (64-6.2 billion JPY).

Upcoming Releases (Q3 Pres)

Infinite Wealth and Persona 3 Reload both reached 1 million in unit sales, which was way above our previous forecasts, and it did so well within a month of release, which is where the bulk of sales will be happening. Infinite Wealth also had a slower player drop-off than we are used to seeing, meaning massive engagement and a lot of content in the game. Or it may be signaling more buying than we typically expect by the distribution we use. Adjusting for their contribution only in Q4, we have the data as in the table above.

58 billion may be tough to reach which was based on the previous forecast for the entertainment segment, where we have a 51 billion JPY for the H2 as possible given the large sales of P3 and Infinite Wealth. Around 49-50 billion JPY is what is implied for the H2 in current forecasts, so we are beating that in our estimates thanks to Infinite Wealth and Persona 3. However, we were conservative with pricing assumptions on some other games like Football Manager which released in November, and stills sells at full price now as an example. The unit sales have doubled since November and their release month counts recorded in the chart. Also, we have likely understated the Gaiden title’s sales as well. 58 billion JPY still might be possible. We think that Infinite Wealth in particular will have long legs. It’s a massive game, and player counts are staying rather in line with release counts, which is rare. The monster release of Infinite Wealth and continued burn from franchises like FM, which are keeping their pricing, could create a surprise in the coming quarter. It may have also recruited new players into the Yakuza franchise, as the critical reception of the game is excellent and becoming organically publicised.

Bottom Line

As said in our previous coverage which we don’t want to belabour here, Pachinko is doing better on improving parlour health, the end of COVID-19, better regulations and new game releases that are at the early stages of penetration. Pachinko is a recurring market since laws require that parlours replace the machines every couple of years to new standards. Every time that happens Sega Sammy makes money.

Sega Sammy is at around a 12x adjusted multiple for the restructuring charges, which is far less than Nintendo at 17x. They have need to improve, but some of their IPs like Yakuza are at the top of their game, and Sonic remains a bankable IP even in Hollywood.

Sega Sammy has an opportunistic buyback programme in place, and it is also expanding its explicit resorts, physical and online gambling businesses with the acquisition of GAN Limited (GAN), with interest to start moving into the large US online gambling market which has gone from grey to white.

With a long-term oriented value thesis, but also the possibility for a beat in upcoming earnings, we think that not only is the value thesis sound, but also the trading thesis, and that it is a buy today.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")

")