Q3 2024 Earnings Call Transcript")

")

Roper Technologies’ (NASDAQ:ROP) business has changed enormously in recent years, with the company now generally focusing on vertical SaaS businesses. In many ways this is a positive as Roper’s margins are now higher and its revenue is more predictable. Given Roper is acquiring these businesses rather than building them, it is less clear how compelling the real benefits are though.

This situation is compounded by Roper’s valuation, which has increased significantly over the past decade. While it is feasible that Roper continues to outperform the market, any outperformance is likely to be fairly modest and there is significant downside risk.

Market Conditions

While the macro environment has been difficult for many businesses due to a combination of higher interest rates and elevated uncertainty, Roper’s mission-critical solutions continue to see robust demand. Roper has suggested that the macro environment is solid, in large part because its end markets (government, insurance, brokerages, healthcare, education) are somewhat insulated. Performance varies significantly across businesses though due to idiosyncratic factors.

Neptune is one of Roper’s largest and most important businesses and it has been benefitting from secular trends that include:

- Labor shortages

- Aging infrastructure

- Regulations

- Water conservation

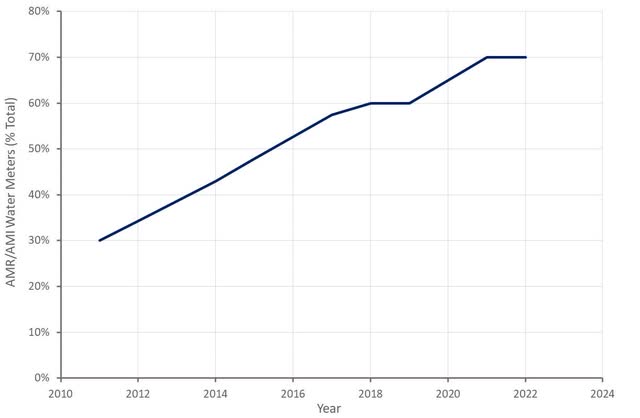

Roper has stated that Neptune is seeing strong demand for residential and commercial ultrasonic meters and increased adoption of data management software. Adoption of smart water meter solutions continues to increase, as they are more efficient and help to address resiliency and sustainability issues. The industry also continues to undergo a conversion from manually read water meters to meters with radio technology, and for AMR systems to be upgraded to digital AMI solutions.

Figure 1: Penetration of AMI/AMR Water Meters (source: Created by author using data from Badger Meter)

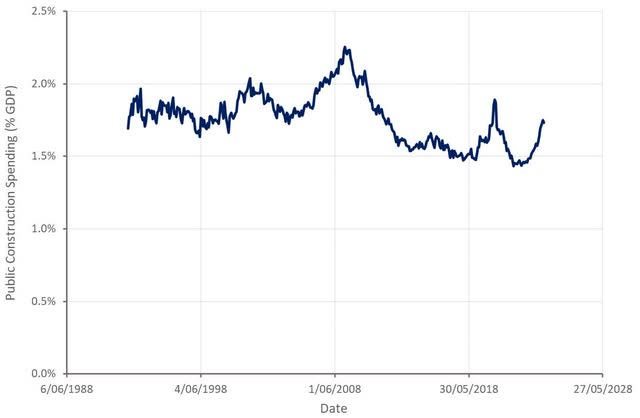

The recent strength of Badger Meter’s (BMI) business is not surprising given the amount of fiscal stimulus being poured into infrastructure. The Bipartisan Infrastructure Law has made over 850 billion USD in total funding available, which is being directed toward areas like water, road, rail, airports, and power infrastructure. The law has an authorizing period of five years, but spending is likely to last beyond this.

Figure 2: Public Construction Spending (% GDP) (source: Created by author using data from The Federal Reserve)

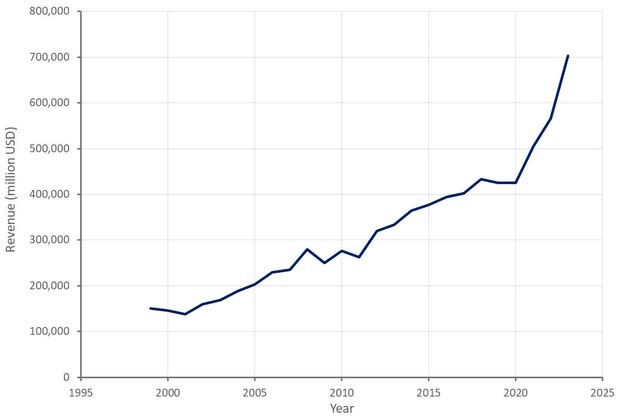

The enormous impact that the current wave of fiscal stimulus and technology upgrades is having can clearly be seen from Badger Meter’s revenue.

Figure 3: Badger Meter Revenue (source: Created by author using data from Badger Meter)

Roper’s freight matching businesses have been faced with relatively soft demand in comparison to the exceptionally strong conditions in 2021 and 2022. While DAT and Loadlink have aligned costs with reduced carrier subscriber numbers, supporting margins, growth is still weak.

The writer and actors strike was also a headwind for Roper’s media and entertainment business in 2023.

Roper

Roper is a serial acquirer that tries to compound cash flows from niche technology businesses. Desired properties of acquisition targets include:

- Market-leading businesses

- Operating in a defensible niche

- Resilient organic growth

- Low churn

- Recurring revenue

- High margins

Roper generally avoids horizontal software as they don’t believe there is any customer loyalty.

Roper has tried to upgrade its portfolio in recent years, focusing on quality, growth and recurring revenue. The company has also been shifting focus toward asset light and less cyclical businesses. Roper recently completed a multi-year portfolio transformation in pursuit of this objective, divesting 34% of its 2019 revenue base between 2021 and 2022.

Roper entered into an agreement to divest its TransCore, Zetec and CIVCO Radiotherapy businesses in 2021. The company also completed the divestment of a 51% equity stake in its industrial business in 2022. This included Alpha, AMOT, CCC, Cornell, Dynisco, FTI, Hansen, Hardy, Logitech, Metrix, PAC, Roper Pump, Struers, Technolog, Uson, and Viatran. Roper retained a 49% equity interest in the new standalone parent company, Indicor.

As a result, the nature of Roper’s business has changed significantly in recent years:

- Revenue from cyclical businesses declined from 34% in 2019 to nearly zero in 2022.

- Approximately 75% of Roper’s revenue comes from vertical software.

- Approximately 56% of Roper’s revenue is recurring in nature.

- Approximately 42% of Roper’s revenue is from SaaS software.

After recent acquisitions and divestitures, Roper now owns 28 businesses, which are segmented under Application Software, Network Software and Technology Enabled Products.

Figure 4: Roper’s Portfolio (source: Roper)

Application Software

- Aderant – management software for law and other professional services firms

- CBORD/Horizon – support software for foodservice operations in education

- CliniSys – laboratory information management software

- Data Innovations – enterprise management software for hospitals and independent laboratories

- Deltek – enterprise software for government contractors, professional services firms and other project-based businesses

- Frontline Education – school administration software

- Intellitrans – transportation management software for commodity producers

- PowerPlan – financial and compliance management software

- Strata – financial analytics and performance management software for healthcare providers

- Vertafore – software for the property and casualty insurance industry

Network Software

- ConstructConnect – software for pre-construction contractors

- DAT – electronic freight marketplace for North America

- Foundry – software for creating visual effects and 3D content

- iPipeline – software for the life insurance and financial services industries

- iTradeNetwork – electronic marketplace and supply chain software for the food sector

- Loadlink – electronic freight marketplace for Canada

- MHA – health care service and software solutions

- SHP – data analytics and benchmarking information for the post-acute healthcare provider marketplace

- SoftWriters – software solutions for pharmacies

Technology Enabled Products

- CIVCO Medical Solutions – accessories for ultrasound procedures

- FMI – metering pumps for high precision fluid control

- Inovonics – wireless sensor network

- IPA – surgical scrub and linen dispensing equipment

- Neptune – remotely monitored water meters

- Northern Digital – optical and electromagnetic precision measurement systems

- rf Ideas – RFID card readers

- Verathon – medical devices that enable airway management and bladder volume measurement solutions

Acquisitions

Between 2020 and 2022 Roper deployed over 10 billion USD towards acquisitions, including 3.7 billion USD for Frontline Education (school administration software) and 5.4 billion USD for Vertafore (property and casualty insurance software). More recently, Roper deployed 2.1 billion USD into vertical software acquisitions in 2023, led by Syntellis and Replicon.

Roper also recently acquired Procare Solutions. Procare is the leading provider of management software to 37,000 owners and operators of early childhood education centers. Procare’s software provides all the necessary functionality to run childcare centers, ranging from parents and family engagement to staff and teachers scheduling, classroom management, tuition billing and payment processing.

Procare reportedly has high gross/net retention rates and Roper believes the company is capable of delivering mid-teens growth and long-term margin expansion. Procare doesn’t currently have a meaningful international business which could support growth in the long run. The end market is relatively small though, only having a 750 million USD TAM, which is growing in the low double digits. Procare is around 1.5x larger than its next largest competitor, with Roper characterizing the market as fragmented and predominantly made up of legacy technology players.

Roper paid 1.85 billion USD for Procare and expects the company to contribute roughly 260 million USD of revenue and 95 million USD of EBITDA in the next 12 months. This acquisition could generate something like a 15% IRR, but reasonably aggressive assumptions need to be made. Roper is a quality company, and this will likely prove to be a solid acquisition, but it is far from an obvious home run.

The primary concerns with Roper’s business from an investment perspective are the number of attractive acquisition opportunities and the price the company will potentially have to pay. Roper has stated that it still has a large pipeline of attractive opportunities and seemed particularly bullish about M&A on the Q1 earnings call. While Roper is now targeting larger companies and companies offering more growth, it is still focused on businesses that are sub-scale for the IPO market, potentially capping valuations. Roper is also now looking at less mature businesses, introducing a greater element of execution risk and making it more difficult to assess acquisitions in the short run.

Financial Analysis

Roper generated 6.2 billion USD revenue in 2023, an increase of 15% over 2022, with 8% organic growth. Acquisition growth was driven by Frontline and Syntellis. Roper’s average organic growth rate over the past 3 years has been around 8%.

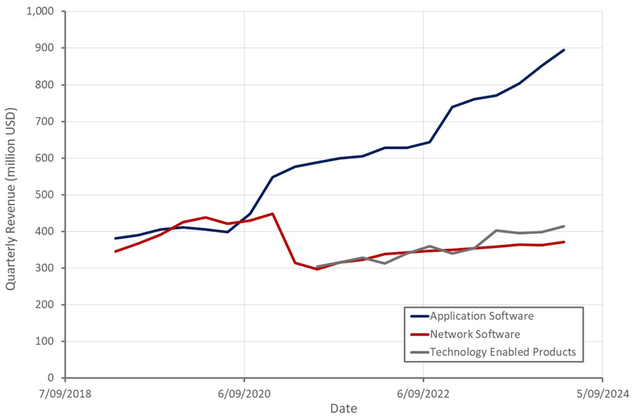

Roper’s revenue in the first quarter of 2023 was 1.68 billion USD, up 14% YoY, with 8% organic growth. Organic growth was driven by the TEP segment, particularly Neptune and Verathon. Neptune is benefitting from fiscal stimulus and an upgrade of water infrastructure. Verathon is potentially benefitting from pandemic backlogs. Application Software revenue increased 17% YoY to 895 million USD, while Network Software revenue was 371 million USD, up 5% YoY. TEP revenue grew 17% to 415 million USD.

Roper expects approximately 12% total revenue growth in 2024 and 6% organic revenue growth. This guidance is based on subdued large customer activity in Roper’s Application Software segment and ongoing weakness in its freight matching business. Syntellis, Replicon and Procare are expected to make material contributions to Roper’s business in 2024 though.

In the long-term, Roper is targeting:

- Double-digit revenue growth

- 8-9% organic revenue growth

- Mid-teens free cash flow growth

Figure 5: Roper Revenue (source: Created by author using data from Roper) Figure 6: Roper Revenue by Segment (source: Created by author using data from Roper)

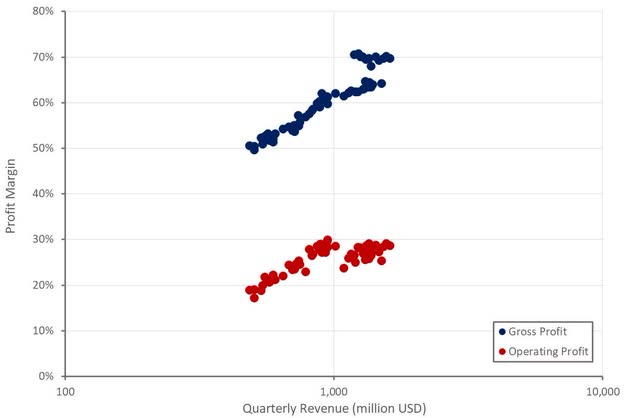

Roper’s gross profit margin was approximately 70% in Q1, up slightly YoY. Roper’s gross profit margins have been trending up over time as the company has shifted its focus towards vertical application software. This is likely to continue going forward, although given that much of this revenue is from SaaS businesses, there may not be that much more room for improvement.

Roper’s operating profit margin was approximately 29% in Q1. The company’s operating profit margins have also been rising over time, driven by gross profit margin improvements. Roper’s operating expenses have actually generally been growing faster than revenue, which is unsurprising given the mix sift towards SaaS.

Figure 7: Roper Profit Margins (source: Created by author using data from Roper)

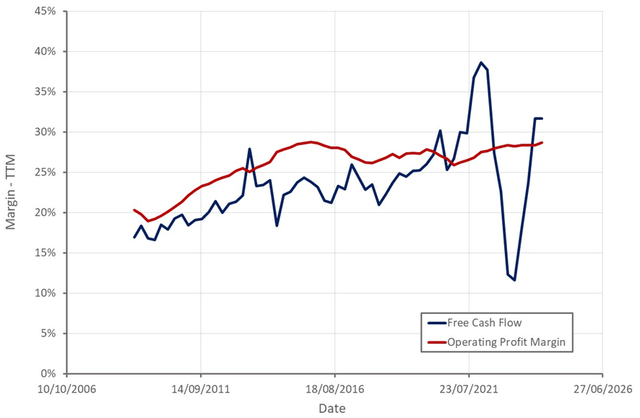

Roper’s free cash flow margin was approximately 32% in 2023, supported in part by negative net working capital. With supply chain pressures easing, Roper also believes that it can free up more working capital from inventory, supporting cash flows going forward.

Figure 8: Roper Free Cash Flow (source: Created by author using data from Roper)

Roper believes that it still has an attractive acquisition pipeline and is well positioned to continue deploying capital in a disciplined manner. Pursuing large growth acquisitions places more goodwill on the balance sheet and may ultimately be to the detriment of shareholders if acquired companies do not grow into their valuations.

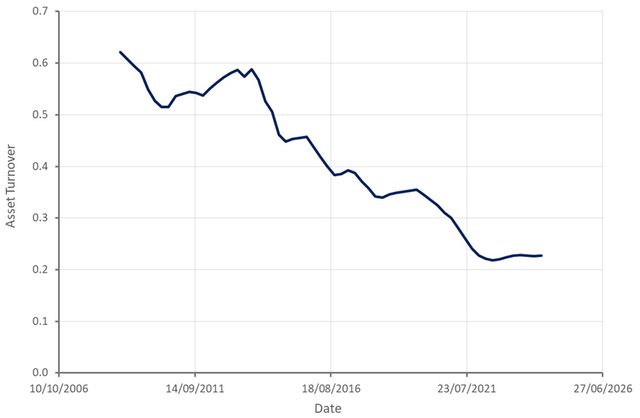

Roper’s asset turnover suggests that the strength of the company’s business model has deteriorated significantly over time. This is complicated for a number of reasons though, including:

- Roper’s margins have improve significantly over time

- Roper is pursuing acquisitions with more growth potential, which will generally entail paying more upfront

- Roper is targeting vertical SaaS businesses, a relatively high-quality source of revenue

Roper also stands to benefit from the migration of over 900 million USD of on-prem maintenance revenue to the cloud. The company believes that as on-prem maintenance spend converts to SaaS, ARR tends to increase by more than 2x.

Figure 9: Roper Asset Turnover (source: Created by author using data from Roper)

Roper’s gross debt was approximately 7.7 billion USD at the end of Q1 and the company had around 200 million USD cash on the balance sheet. The company’s net debt-to-EBITDA ratio is 2.9, below the long-term target of 3-3.5. Roper believes that it can still deploy around 4 billion USD in the near term.

Conclusion

The real benefit of the serial acquirer strategy comes from taking cash flowing businesses that are unable to redeploy capital and using that as fuel for an acquisition engine. Roper’s focus on larger companies with higher organic growth potential means that it is paying a higher multiple and limiting acquisition benefits. I think the shift towards higher quality companies with more growth opportunities increases the risk of underperformance in the future. There is also the question of whether the acquirer or the target company capture the value created.

This situation is exacerbated by Roper’s high valuation, which can only be justified by efficient growth over the long run. While Roper’s valuation appears high, it should be noted that this is supported by improved margins and a greater contribution from recurring revenue.

Figure 10: Roper EV/S Multiple (source: Seeking Alpha)