")

Introduction

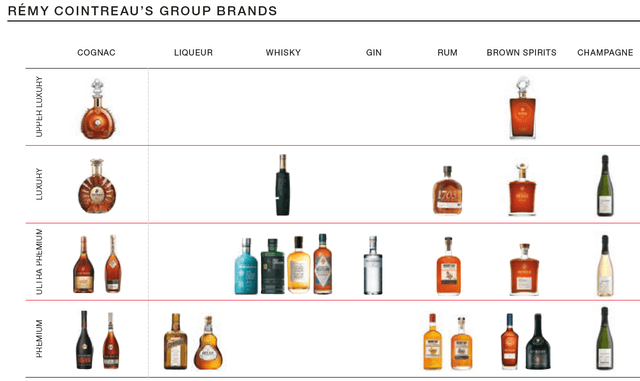

Although the name Rémy Cointreau (OTCPK:REMYF) (OTCPK:REMYY) may not sound familiar to everyone, its portfolio of brands will likely ring a bell. As close to 75% of the total revenue is generated by cognac sales, cognac is the most important part of the portfolio. Cointreau has a worldwide market share of approximately 14% in the cognac market. Despite its strong position, the share price lost about a third since my last article on the group.

Remy Cointreau Investor Relations

That being said, the company has been diversifying as well and it now also owns some champagne brands as well as single malt whiskies.

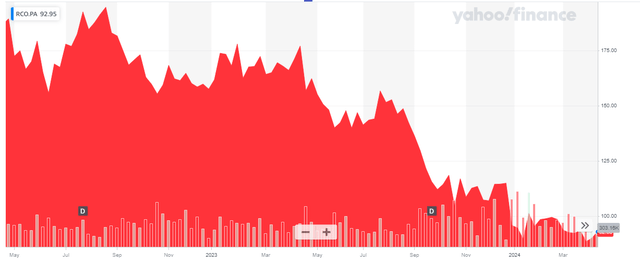

Yahoo Finance

Remy Cointreau has its primary listing in France where it’s trading with RCO as ticker symbol. The average daily volume is approximately 100,000 shares per day, so the French listing clearly is pretty liquid. The most recent share price was 92.95 EUR and considering there are just over 50M shares outstanding, the market capitalization is just below 5B EUR.

The first nine months of the year were tough – as expected

The company’s financial year runs from April 1 until March 31 which means Remy Cointreau’s financial year has just ended. It will report its full-year financial results in June (a sales result will be published next week) but I thought it made sense to already have a look at the company using the H1 report and Q3 trading update.

As the Q3 update is just a trading update which does not contain any detailed numbers or results, I wanted to go back to the H1 report as that paints a god picture of the performance of the company.

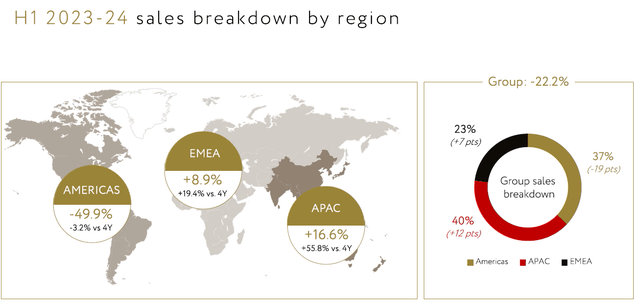

And that picture wasn’t nice. In the first half of the year, total revenue decreased by approximately 27% of which 22% was an organic revenue decrease. Fortunately the company was able to protect its margins as the gross margin increased slightly but that obviously wasn’t a big help. Remy Cointreau is very cognizant of the disappointing performance and refers to short-term headwinds (mainly cyclical headwinds) while it fully counts on its long-term vision. While the performance in the Asia-Pacific region remained strong with a 17% revenue increase and even Europe showed a 9% revenue increase, the Americas division performed pretty poorly with a YoY revenue decrease of almost 50%.

Remy Cointreau Investor Relations

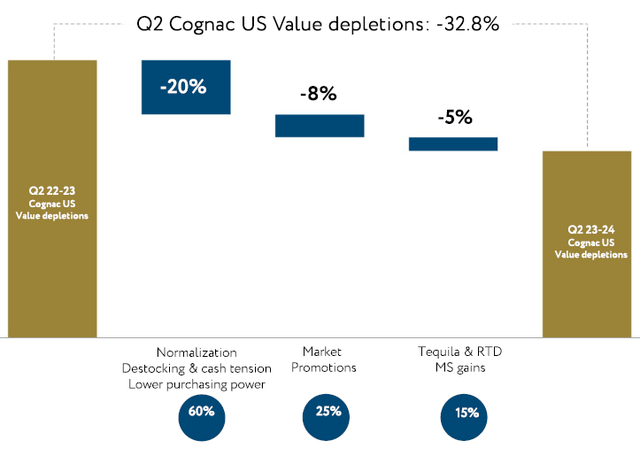

That was a headscratcher but fortunately Remy Cointreau spent some time to explain the situation. The company thinks the current downturn is cyclical and refers to a structural normalization of the demand and inventory levels. The volume depletion came in at almost 33% in the first half of the year and the company thinks 60% of this is due to destocking while about 25% of the depletion is caused by promotions to keep on pushing the brands forward.

Remy Cointreau Investor Relations

And finally, Remy Cointreau doesn’t have any entry level spirits as it only offers premium and luxury brands.

As the revenue decrease in the first half of the financial year was predominantly related to a destocking push, one would expect the volumes and revenue to pick up again when the tide turns. This may already have happened in the third quarter as in its trading update, Cointreau mentioned a slight decline in the third quarter representing a “sharp sequential improvement” compared to the second quarter. On the other hand, the third quarter performance in the APAC region deteriorated pretty substantially due to a destocking push ahead of Chinese New Year, so the second half of FY 2024 will likely still be a mixed bag.

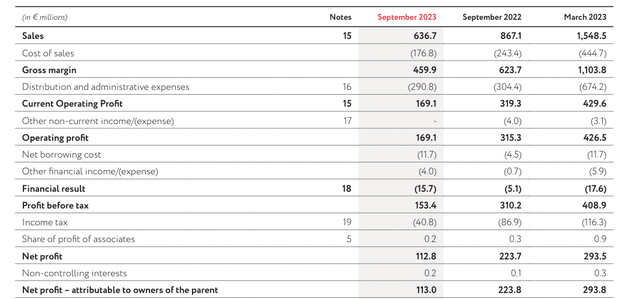

To put this into perspective, let’s go back to the detailed H1 2024 results. As the income statement below shows, the total revenue in the first semester came in at 637M EUR, resulting in a gross margin of approximately 460M EUR. The total distribution and admin expenses decreased as well (but by just over 4%), allowing the company to record a 169M EUR operating profit.

Remy Cointreau Investor Relations

After deducting the 16M EUR net finance result and the 41M EUR in taxes, the bottom line showed a net profit of 113M EUR which represents an EPS of 2.24 EUR based on the average share count of 50.5M shares.

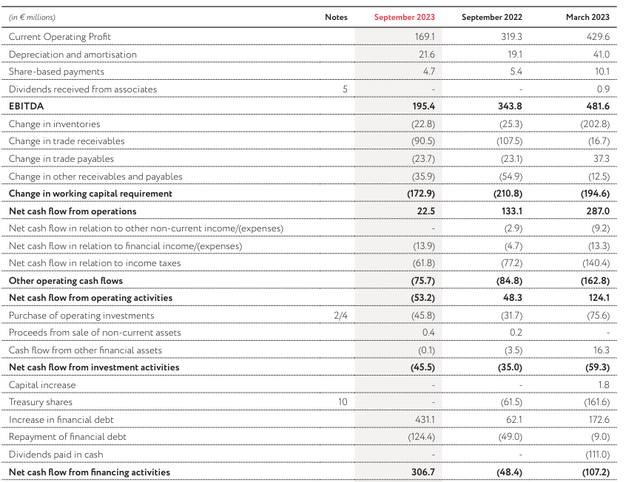

The cash flow result was pretty much in line with reported earnings. As you can see below on the cash flow statement, the operating cash flow was a negative 53M EUR. However, this includes 173M EUR in working capital buildup while the company also spent 21M EUR on cash tax payments which weren’t owed based on the H1 income statement. We also should deduct approximately 4M EUR in lease payments.

Remy Cointreau Investor Relations

All those adjustments result in an adjusted operating cash flow of 137M EUR. Meanwhile the total capex was approximately 46M EUR as Cointreau is still investing in growth (its total capex was almost three times the depreciation expenses on tangible assets). The free cash flow result was approximately 91M EUR which is approximately 1.80 EUR per share. Low, but that was to be expected given the disappointing earnings result in combination with a relatively high capex.

Unfortunately the visibility in the near term remains limited for Remy Cointreau. The company has confirmed its full-year guidance and the company now still expects an organic revenue decrease of around 20%. Cointreau’s main focus is on protecting the margins and the company is successful in doing so.

Cointreau also confirmed its long-term guidance for 2030 remains valid. It wants to bump its gross margin to 72% on a consistent basis while it expects to increase its operating profit margin to 33% (up from just under 27% in the first half of FY2024). But of course 2024 still is a way’s away and the company will first have to get through the current more difficult period.

Investment thesis

The main risk now is the recently opened investigation in China which is investigating if Cointreau overstepped the anti-dumping regulations. This likely is just a political retaliation from China, but it obviously has the potential to weigh on the share price and I hope Cointreau can find an amicable solution.

I currently have no position in Cointreau as I always found the stock to be a bit too expensive for my liking. The recent share price correction on the back of what will be a poor FY 2024 result and the reduced visibility for FY 2025 could perhaps create an interesting entry point for investors with a long-term horizon. The analyst consensus estimates are expecting the EBITDA to increase by approximately 10% per year in the next two years and I’m looking forward to the company’s presentation of the FY 2024 results to see if management shares that enthusiasm.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q1 2024 Earnings Call Transcript")