")

In December 2023, I initiated coverage for Redwire Corporation (NYSE:RDW), marking the stock a Hold with a speculative buy opportunity, noting the potential risk of dilution. That call has worked out rather well, as share prices have more than doubled. In this report, I will be discussing the most recent earnings and revisit my rating for Redwire Corporation.

Redwire Topline Surge Does Not Translate To Bottomline

Redwire Corporation

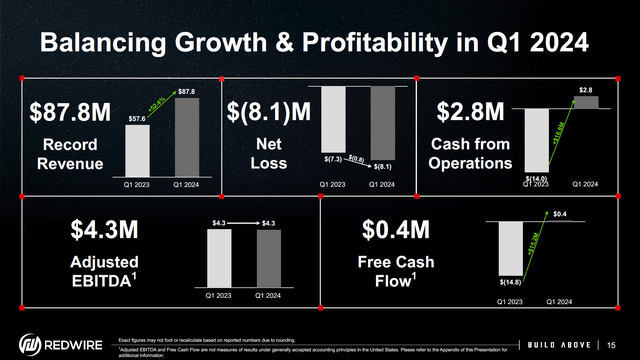

What is interesting to note is that in the first quarter, we saw strong revenue growth but on none of that translated to the adjusted EBITDA level. Revenues surged by 52% to $87.8 million, driven by bigger contract sizes as well as higher volumes in power generation, structures and mechanisms. This was partially offset by negative catch up adjustments that were $3.3 million higher year-on-year, driven by additional design and testing required to meet customer requirements.

Gross margin increased by 4% and that already shows where the lack of top line growth to EBITDA growth is caused. Gross margins fell from 25% to 17% and that is driven by the contract mix. What hold for many companies is that when they start producing new products or are in the development phase of contracts, the margins are slow. That creates the situation in which the company is growing, but margins are falling due to the margin mix. Those are not necessarily bad developments and can be seen as an investment in the future being made now.

Overall, the net loss widened driven by the margin pressure, higher share-based compensation, higher R&D and interest costs. The positive is that cash flow from operations and free cash flow improved.

Is Redwire A Good Stock To Buy?

For 2024, the company is expecting revenues to hit $300 million. I have included the forward projections and current balance sheet data into my model, but the results are not quite reflective of what I would deem to be reasonable. Due to the negative EV/EBITDA for Redwire, the model generates a sell rating with 7% downside with the preferred convertible stock included and 11% upside if the preferred convertibles are excluded. I believe that the company is a hold with little to no upside for 2025. For 2026, there would be significant upside. However, we are also mindful about the risks.

The risk I see remains the debt load maturing in 2026. Virtually all of the company’s $89.7 million in debt matures in 2026. If financial results would permit, the company could refinance the debt. If that is not the case, we could see the company issuing common or preferred stock. Currently, the company already has preferred convertible stock issued that could significantly dilute shareholders in the case of conversion and given the pay-in-kind dividend we see additional dilution pressure. So, while I do like Redwire’s products and their top line growth, the dilution and debt pressure is significant, and as long as we have no sight on how the company will address the 2026 debt pile, we see shareholder dilution as a significant risk and feel more comfortable with a hold rating rather than the previous strong buy rating.

Conclusion: Redwire Corporation Is A Nice Company, Unattractive Risk

I like the overall product portfolio and the bidding for bigger contracts and exploring new product lines for commercializing on space. However, what is a significant drag for Redwire is its capital structure. There are convertible preferred stock outstanding that already provide a significant dilution to shareholders if the shares are converted, which I believe would happen on a cashless base if it happened. Furthermore, there is a significant debt for which I have seen no clear plan from Redwire management to address this. As long as this significant debt load in 2026 is not addressed, I see additional dilutive pressure on Redwire stock, even more so since the company’s stock has significantly risen. The good thing about the higher stock prices is that higher stock prices allow Redwire to raise capital with a lower dilutive impact.

")

")

")