")

Investment Thesis

Precision Drilling Corporation (NYSE:PDS) is experiencing a significant increase in the number of service rigs, and more could come, thanks to the Trans Mountain pipeline expansion and regulatory spending requirements for well abandonment increase. The recent plans for reduction of the debt levels and distribution of 25%-35% of FCF generated to shareholders could accelerate demand for the stock.

Price Target: Based on my own discounted cash flow analysis, the fair value is $104-$105 per share.

Business Review: Drilling Is The Most Relevant Activity

Precision Drilling is an energy company based in the United States and Canada that has also developed international activity in some areas of its business.

During 2023, close to 87% of its revenue came from drilling activity, under specific contracts. The remaining net sales came from the other segment, which offers completion, workover, and ancillary services to oil & gas exploration and production companies. International activity consists of drilling services, which include technology for the development of platforms and consulting to comply with environmental regulations in each case.

CWC Energy Services: Accretive On A 2024 Cash Flow Per-Share Basis

During the year 2023, Precision Drilling accomplished the acquisition of CWC Energy Services, which meant an expansion in its activities in Canada, adding 62 drilling service platforms in this country, in addition to equipment, inventory, and operating facilities that were added to the 111 platforms that were already active. The acquisition was valued at $127 million on November 7, 2023. In my opinion, the most relevant is that the company expects the transaction to be accretive on a 2024 cash flow per-share basis. Hence, we could see an increase in cash flow per share in 2024 as compared to that in 2023.

With the projected synergies, we expect the transaction to be accretive on a 2024 cash flow per share basis and to support our ongoing deleveraging plan. Source: Press Release

Precision has achieved headcount and operational annual run-rate synergies of approximately $13 million. Source: Annual Report

Automation And Data Processing Software To Enhance Drilling Activities

One of the differentials that Precision has found within the competitive markets of the energy sector is the development of its Alpha digital platform, which uses automation and data processing software oriented towards each of its clients.

In addition, the company maintains Evergreen technology, developed to optimize environmental pollution rates, through the automation of the operation of drilling equipment and data processing.

During 2023, the company had the most modern drilling equipment in Canada, which not only has Alpha and Evergreen technology, but also maintains some robotic functions, adding to the automation capabilities as well as increasing general safety levels in the development of activities.

In my view, these technologies could enhance future drilling activities, and offer an enhancement in the environmental pollution rates. In addition, clients may demand more drilling services as robotic functions offered increase.

According to Market Research Survey, the use of robotic drilling equipment in the petroleum industry is projected to rise at 8.5% CAGR through 2033. I incorporated these assumptions in my forecasts.

New International Rigs And The Trans Mountain Pipeline Expansion Represent A Net Sales Driver

In the last management report, I could read about eight rigs running throughout 2024, which is expected to represent a 40% increase in activity compared to 2023. We are talking about a 50% increase in the company’s international EPS, which I think may benefit future earnings expectations and the demand for the stock.

I could also observe a significant optimistic outlook for the business coming from rig activations and new bids. Besides, if clients continue to show up thanks to the Trans Mountain pipeline expansion and regulatory spending requirements for well abandonment increase, revenue growth could also accelerate.

We continue to bid our remaining idle rigs within the region and remain optimistic about our ability to secure additional rig activations. As the premier well service provider in Canada, with size and scale, the outlook for this business is positive. Source: Management Discussion, And Analysis

Growing Number Of Service Rigs, Compliance With Covenants Signed, And Debt Reduction Plans

There is a significant momentum growth in the number of well servicing rigs. In the quarter ended March 31, 2024, the number of service rigs was 183. In the same quarter in 2023, the number of rigs was 118. The change in the number of service rigs was 55. In my view, further increase in momentum growth could bring new revenue growth.

Source: Management Discussion, And Analysis

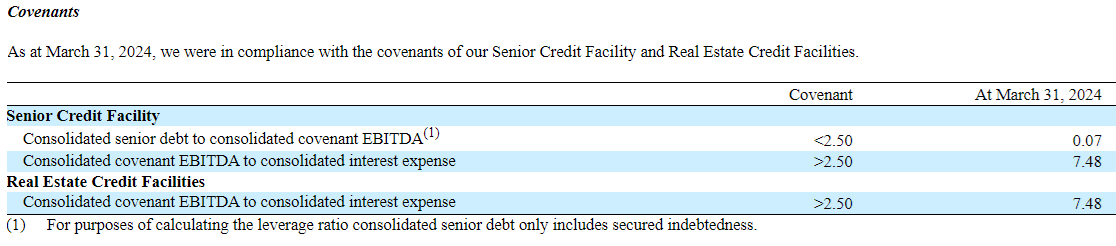

Besides, the company is in compliance with covenants signed. As of March 31, 2024, Precision Drilling reported consolidated covenant EBITDA to consolidated interest expense of 7.4x. The covenant signed was 2.5x.

Source: Management Discussion, And Analysis

According to the last annual report, one of the central objectives of the company’s present strategy is to reduce the total amount of debt. In the long term, the reduction objectives are $500 million by 2025. The company plans to reduce debt by $150 million to $200 million in 2024.

During the year, we reduced our debt by $152 million and allocated 15% of our free cash flow to share repurchases. Our focus on our debt reduction strategy remains firmly in place and in 2024, we plan to reduce debt by another $150 million to $200 million. Source: Annual Report

Besides, in the last quarterly report, Precision promised once again to return 25%-35% of FCF generated to shareholders. In my view, further reduction in the debt levels could lead to increases in the EV/FWD EBITDA ratio.

Precision remains on track to reduce debt between $150 million and $200 million in 2024 and return between 25% and 35% of free cash flow to shareholders in 2024. Source: Management Discussion, And Analysis

The CFO Brings Investment Banking Expertise

I reviewed the Board of Directors and the business profile of different members of management. I think that Wall Street analysts may like the profile of Carey T. Ford, CFO of Precision. He brings expertise accumulated in investment banking. In my view, if the company needs to assess potential mergers or acquisitions with other competitors or even the sale of Precision Drilling, he will offer beneficial judgment to bring a beneficial opinion to the Board of Directors. Besides, he may know well what the company needs to offer to market participants and shareholders to enhance the valuation of the company.

Carey T. Ford currently serves as Senior Vice President & Chief Financial Officer for Precision. He joined the company in May 2011. Mr. Ford previously held the positions of Vice President, Finance & Investor Relations and Senior Vice President, Finance Operations before being named Interim Chief Financial Officer in March of 2016. Prior to joining Precision, Mr. Ford spent seven years as an investment banker at Simmons & Company International serving clients in the oilfield service sector. Source: Precisiondrilling

The Balance Sheet Shows A Significant Decrease In Total Debt

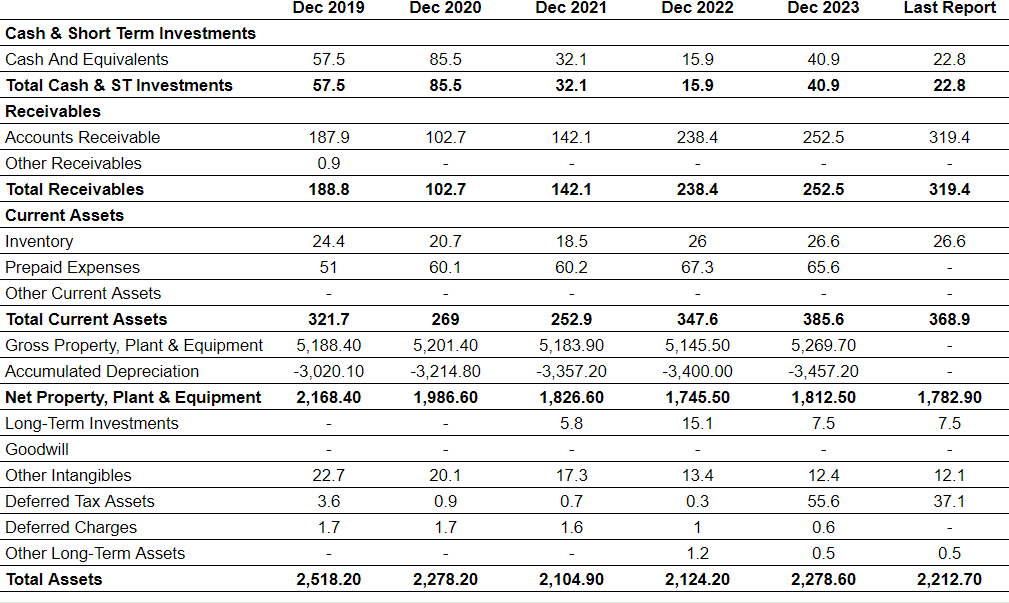

Precision’s balance sheet shows an asset/liability ratio of more than 2.2x. This ratio increased from close to 1.9x in 2019. Precision Drilling reports an increase in the total amount of property and equipment/total liabilities from 2019 to 2024, which I think is quite beneficial. The company appears to be reducing its total amount of liabilities at a faster rate than the property and equipment.

Source: Author’s compilations based on data from the 10-Q

In the last report, the company reported $2.2 billion in total assets and $1 billion in total liabilities. So, the book value per share is lower than the current stock price. According to Seeking Alpha, the sector median price/book value is close to 1.5x. Given these figures, Precision Drilling appears quite undervalued.

Source: Author’s compilations based on data from Seeking Alpha

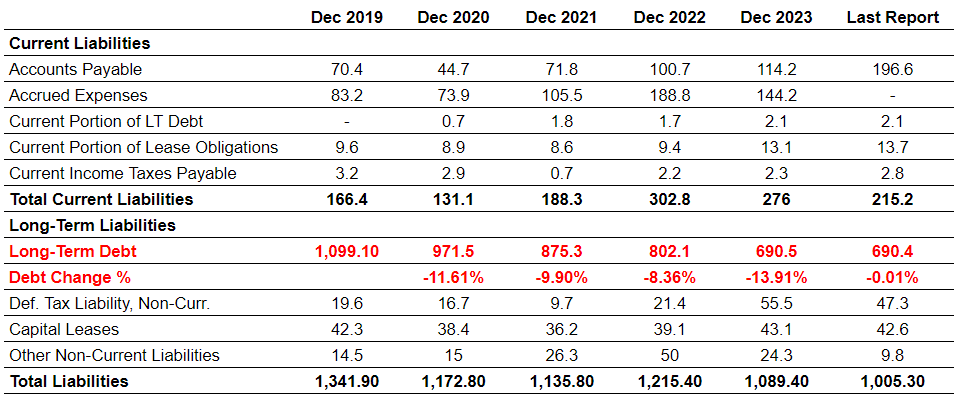

As shown in the image below, the total amount of long-term debt decreased by around 13% in 2023, 8% in 2022, and 9% in 2021. In my view, a further decrease in the total amount of debt will most likely lead to an increase in the company’s EV/FWD EBITDA.

Source: Author’s compilations based on data from Seeking Alpha

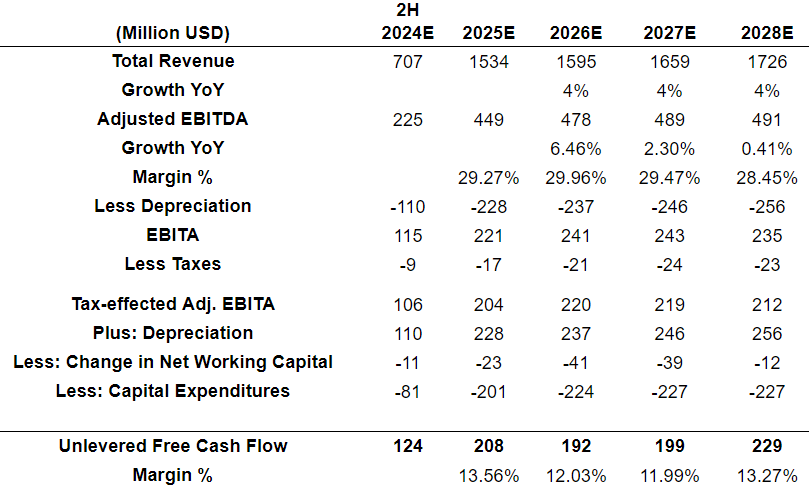

Discounted Cash Flow Analysis

In connection with rendering the opinion given and performing my related financial analyses, I reviewed the company’s annual report and the most recent report from management. Besides, for the assessment of future Adjusted EBITDA growth, the calculation of EBITDA, changes in net working capital, taxes, and capex, I reviewed SA’s tool.

Source: Seeking Alpha

I also assumed a growing number of service rigs, FCF growth thanks to the Trans Mountain pipeline expansion and regulatory spending requirements for well abandonment increase. Besides, I also expect growth as a result of the use of automation and data processing software.

With the previous assumptions, I included net sales growth of 4% from 2026 to 2028, with growing D&A, growing capex, and growing unlevered free cash flow. Under my own assumptions, unlevered FCF/Total revenue would be close to 13% and 11% from 2025 to 2028. These numbers were based on my own judgment, previous assumptions, and previous cash flow statements.

Source: Author’s Work

For the selection of the terminal EV/TTM EBITDA, I had a look at the multiples currently reported by peers. Competitors trade at close to 4x TTM EBITDA and 10x EBITDA. I used an exit multiple of 4.5x. Besides, after reviewing previous quarterly reports and 10-Ks, I incorporated a cost of capital of 9%.

Source: Seeking Alpha

Finally, I performed a DCF to calculate the implied equity value. By summing the discounted unlevered free cash flow from 2024 to 2028 and the discounted terminal value, and subtracting the net debt, I obtained a target equity value of $1532 million. Dividing by the total number of shares outstanding, my target value is close to $104-$105 per share.

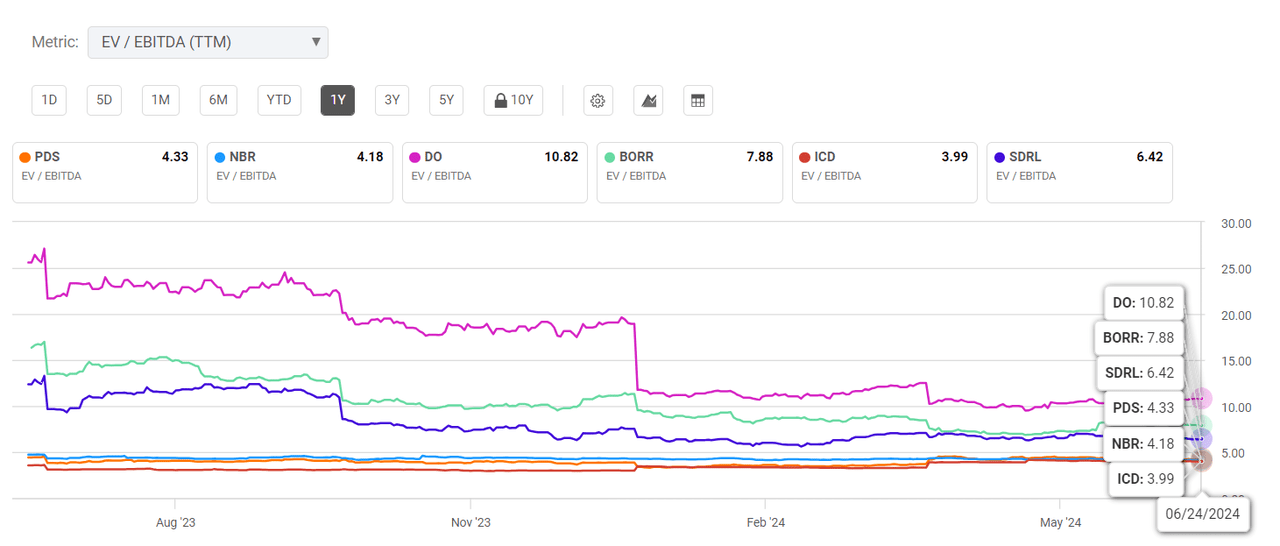

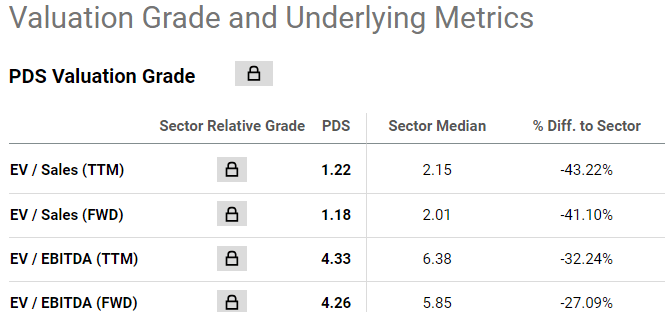

Precision’s EV/ FWD Sales And EV/ FWD EBITDA Show Significant Undervaluation

A quick look at the EV/FWD Sales and EV/FWD EBITDA ratio reported by Precision Drilling and that from the industry indicates significant undervaluation. The company’s EV/EBITDA appears to offer a 27% discount as compared to peers.

Source: Seeking Alpha

Other companies focused on drilling, such as Helmerich & Payne (HP) as well as Nabors (NBR), show an EV FWD EBITDA between 4x-4.5x, which is not far from that of Precision Drilling. Hence, I think that by means of a merger of Precision Drilling with another company offering more services from drilling, the total EV/FWD EBITDA of the new entity may increase.

Equity Research Share Price Targets

I reviewed publicly available consensus estimate stock price targets for the company. I could find Wall Street analysts covering the stock, who published research with an average price target of $100. These numbers are in line with my expectations and price target of $104-$105. It appears clear that most people in the market think that Precision Drilling is undervalued.

We Saw Mergers In The Sector In 2023

Patterson-UTI Energy, Inc. (PTEN) and NexTier Oilfield Solutions Inc. signed a merger in 2023, which included $200 million of annual cost savings and operational synergies within 18 months following close. Precision Drilling could also team with another large player in the United States or Canada to generate synergies. I could not blame shareholders for expecting such a similar transaction with other players like Helmerich & Payne, Nabors, Liberty Energy, ProFrac Holding, RPC, Calfrac Well, STEP Energy, or Trican Well. Potential cost synergies observed in the merger between PTEN and NexTier could appear.

Risks From Changes In The Oil Price

Precision’s revenue will most likely fluctuate in relation to the oil price. Lower oil price and gas price may lead to lower drilling activity in the United States and Canada. If clients decide to reduce their activities, Precision Drilling would see decreases in the unlevered FCF. Under this case scenario, analysts could lower their expectations about the future, and the demand for the stock could lower.

Generally, we experience high demand for our services when commodity prices are relatively high, and the opposite is true when commodity prices are relatively low. The volatility of crude oil and natural gas prices accounts for much of the cyclical nature of the oilfield services business in recent years. Increased volatility and other factors beyond our control have led to greater uncertainty in the demand for our services. Source: Annual Report

Risks From Trans Mountain Pipeline And Regulatory Uncertainty In Western Canada

Precision Drilling could suffer from delays in the construction of the Trans Mountain pipeline in western Canada. Besides, management noted that other proposed LNG facilities in Canada could also suffer from delays. If the company fails to complete their expected timelines, expected net sales growth may decrease. In the worst case scenario, future unlevered FCF may also decline, and the implied fair price would be lower than expected.

Construction is progressing on the Trans Mountain pipeline in western Canada and may be in service in the first half of 2024. Canada generally has also lagged behind other natural gas producing countries in taking advantage of rising global demand and prices for natural gas primarily as a result of Canada’s lack of liquified natural gas facilities and, by extension, export capacity owing to regulatory delay and uncertainty. Source: Annual Report

Other proposed LNG facilities in Canada are at earlier stages of development, including Woodfibre LNG and Ksi Lisims LNG (completions currently anticipated between 2027 and 2028). There is no assurance that LNG projects in Canada will be completed on their expected timelines, or at all. Source: Annual Report

Risks From Violence In The Middle East Region

As noted, Precision Drilling maintains activities internationally, specifically in the Middle East region, where the capitalizable market is large, and oil activity is highly concentrated. Based on the signing of new contracts and the insurance of its activity within the Middle East for the short and medium term, the company increased its lines of credit for insurance on this activity from $30 million to $40 million. In any case, with regard to this region specifically, the outlook is uncertain due to the growing violence between the Israeli state and neighboring countries. At some point, I think that the activities of Precision Drilling could be affected by the war in the region.

Conclusion

Precision Drilling is currently experiencing a growing number of service rigs, and offered a beneficial outlook thanks to the Trans Mountain pipeline expansion and regulatory spending requirements for well abandonment increase. I would expect net sales growth as a result of new robotic functions and the use of automation and data processing software. In addition, management recently promised to lower its debt levels as well as to return 25%-35% of FCF generated to shareholders. I think that these initiatives could represent successful future price catalysts for the stock. Based on my own DCF model, peer review, and research of other opinions from analysts, my price target is $104-$105 per share.

")

")

")