")

")

Intro

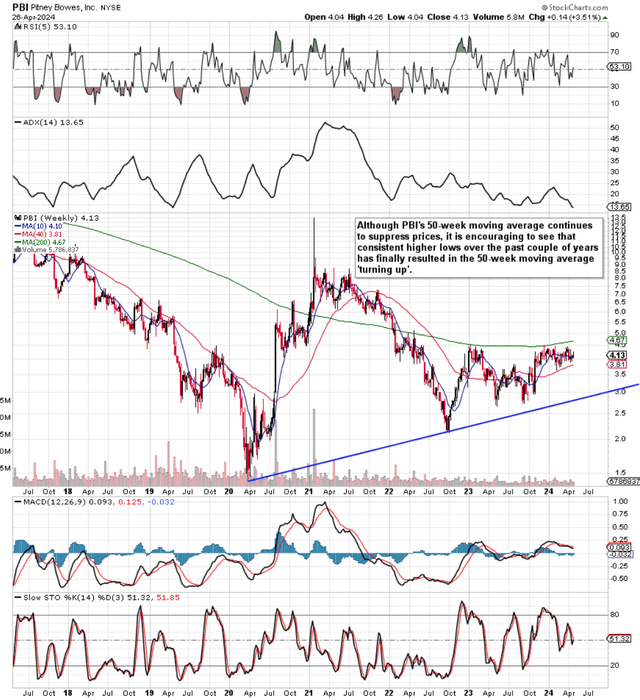

We last wrote about Pitney Bowes Inc. (NYSE:PBI) in February of 2023 when we rated the freight & logistics company a ‘Hold’. In hindsight (as confirmed by PBI’s technicals below), the ‘Hold’ rating was the right call as shares are basically ‘flat’ since our commentary over fourteen months ago. Overhead resistance (50-week moving average) continues to rule the day in Pitney Bowes & until this key resistance area gets breached to the upside, we have no interest in getting long this underlying.

In saying this, it is noteworthy that the stock’s 50-week moving average has finally begun to turn up, particularly in calendar 2024. Given that share-price action on the technical charts always gives the ‘full picture’ regarding the fundamentals of the company at a given time, change may very well be afoot in PBI.

PBI Intermediate Technical Chart (Stockcharts.com)

Suffice it to say, here is where value investors many times can get blindsided. What we mean by this is that much value-orientated teaching literature aimed at investors focuses on positive profitability and a clean balance sheet. Although as we see below, Pitney Bowes’ valuation from an assets & sales standpoint may still look compelling, the company continues to hold significant debt on the balance sheet (to the tune of $2.09 billion at the end of fiscal 2023) where negative GAAP earnings were reported in the same year (-$385 million). These trends continue to pressurize PBI’s 4.8%+ dividend yield where growth in the payout has been non-existent for some time now. Therefore, you feel a catalyst may be needed (which may make the market view the stock differently) to finally hurl shares above long-term resistance. Here are our thoughts on ways PBI can unlock capital going forward.

| Financial Metric | PBI (Trailing) |

| GAAP Earnings | -$385.6 Million |

| Price To Sales Ratio | 0.22 |

| Dividend Yield | 4.84% |

| Price To Cash-Flow | 9.23 |

| Shareholder Equity | -$368.6 Million |

| Long-Term Debt | $2.09 Billion |

PBI Debt Profile Post Q4-2023 (Seeking Alpha)

Global E-commerce (GEC) Business

Investors may believe that the sale of this business would do little to revitalize the share price (Due to the sustained hemorrhaging of cash) but they would be wrong. If we go higher up PBI’s income statement, for example, for fiscal 2023, we see that the company remained profitable from an EBIT ($91.6 million) standpoint. Interest expense for the same period came in above $100 million. Obviously, this expense could be impacted favorably depending on the price tag fetched for GEC, but the benefit of a potential sale reaches far beyond an incoming credit. What we mean by this is that GEC contributed over $130 of negative operating profit to the company last year. This means, that if the business did not exist, PBI would have reported well over $200 million in EBIT last year.

The hunt for a CEO still goes on where you feel the impact (despite recent upheaval concerning the board of directors) from Hestia Capital over the past 9 months has been limited, to say the least. What may be foreshadowing an upcoming GEC sale was management’s recent decision to shift the profitable digital shipping business of Global E-Commerce into SendTech. Despite GEC’s high costs and the adverse ramifications from the alteration to cross-border client relationships, this segment still managed to report a 13% increase in domestic parcel volume in the recent fourth quarter.

EBIT also sequentially improved due to ongoing profitability & the above-mentioned stronger domestic volume. Going forward within GEC, astute investors know that volume numbers need to remain elevated for profitability to improve, and here is where PBI may be found wanting. Why? When one takes into account Pitney Bowes’ current market cap ($737 million) and struggling profitability, one must ask whether a superior economy of scale exists within the overall operation at present to be able to record marked improvements in efficiencies. We are not so sure.

Suspend The Dividend & Cancel A Percentage Of Treasury Stock

Remember, ongoing cost-cutting initiatives will only take PBI so far concerning improving underlying profitability. Near-term forward-looking EPS revisions have been poor, citing another reason for more radical change. Therefore, to aggressively back the likes of client support in Presort & invest in shipping capabilities in SendTech, other options open to PBI would be to suspend the dividend or cancel a percentage of the company’s Treasury Stock. First, concerning the dividend, the payout cost the company over $35 million last year. In fiscal 2023, PBI’s dividend was not covered by either net earnings or free cash flow, meaning resources of the company continue to be depleted.

Nevertheless, given the $2.86 billion of treasury stock on the balance sheet, canceling some of these shares would immediately provide cash flow for the company. These shares denote stock that has been previously repurchased but has yet to be retired. Suffice it to say, that the above-mentioned negative shareholder equity number ($-369 million) is not an accurate picture of PBI’s solvency, given the amount of Treasury Stock the company holds. Value investors also need to take this into account when doing their due diligence.

How Treasury stock changes the dynamic from a valuation perspective is the following. If we were to add treasury stock back to the present shareholder equity number ($-369 million), we would get an adjusted debt-to-equity ratio of 0.84 which demonstrates that PBI may certainly be undervalued once capital can be unlocked.

Conclusion

Pitney Bowes is expected to announce its first-quarter earnings numbers for this present fiscal year later this week. (May 2nd). Consensus is looking for revenues of approximately $797 million & earnings of -$0.04 per share. Irrespective of the pending results, investors will be more interested in information surrounding how value can be unlocked, specifically regarding a potential Global Ecommerce sale or major restructure. We look forward to continued coverage.