Will Reach $200,000 During the 2024-25 Bull Run, Highlights Solana Competitor Priced Under $0.05 as the Most Promising Altcoin This Cycle")

Q1 2024 Earnings Call Transcript")

On Friday, March 29, 2024 at 8:30 AM US EST, the Bureau of Economic Analysis (BEA) will publish its monthly report on Personal Income & Outlays (PI&O), in which they will release their estimates for U.S. Personal Consumption Expenditures (PCE) corresponding to the month of February 2024. Revisions to PCE data for prior months will also be released.

PCE, also referred to as “Personal Spending,” directly accounts for over 60% of total U.S. Gross Domestic Product (GDP), marking it one of the most important coincident indicators of U.S. economic activity. Consequently, forecasts for near-term GDP growth, inflation, and monetary policy will tend to be impacted substantially after the release of PCE data. It will also greatly impact assessments of the prospects for a “soft landing” of the U.S. economy.

In this article, we will provide critical background information and analysis that will help readers to assess the PCE data when released and to size up (pre and post) market reactions.

Summary of Forecasts and Expectations

In this section, we provide a summary of forecasts for PCE, the PCE Price Index (PCEPI) and Real PCE.

Figure 1: Summary Data and Analysis

Forecasted PCE Summary Data & Analysis (BEA, Investor Acumen & Investing.com)

The median estimate of professional forecasters expects Personal Consumption Expenditures for February 2024 to be reported at $19,149.47 billion in current dollars, a record high. This would imply Month-on-Month (MoM) growth of +0.50%, a rate of change which would rank in the 51st percentile historically. The median forecast expects Real PCE – adjusted for inflation by the PCEPI – to be reported at $15,650.49 billion, also an all-time record. This would imply a MoM rate of change of +0.10%, which would rank in the 34th percentile historically.

Critical Background

In this section, we provide our readers with contextual data, which is critical for evaluating the PCE data in the PI&O report. First, we review the recent history of growth and momentum of PCE. Second, we review the recent history of deviations from forecasted values in order to gain an appreciation for the extent of forecast errors and any tendency toward bias. Finally, we review the recent history of BEA data revisions, in order to be able to understand the frequency and magnitude of recent errors and any tendency toward bias in the BEA’s estimates.

Recent History of Growth and Momentum

In Figure 2 we can see the 1-month, 3-month, 6-month, and 12-month annualized rate of change of current-dollar PCE, PCEPI, and Real PCE, assuming the consensus forecasts are accurate.

Figure 2: Annualized Growth Rates of Nominal and Real PCE

Annualized Growth of Forecasted PCE (BEA, Investor Acumen & Investing.com)

The 3-month annualized rate of change of Real PCE is expected to be +2.17%, which is well below average (34th percentile), indicating deceleration compared to the 6-month annualized rate of change (41st percentile).

History of Forecast Deviations

Reported data often deviate from the estimates of professional forecasters. It is important to understand the frequency and extent to which this is true. Furthermore, it is important to observe whether there is any tendency toward forecast bias.

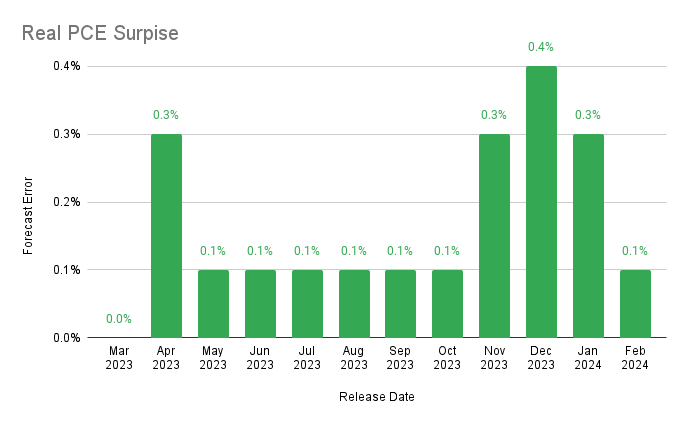

Figure 3: 12 Months of Real PCE Forecast Deviations

Real PCE Forecast Surprise (BEA, Investor Acumen & Investing.com)

In Figure 3 we can observe the frequency of significant errors and forecast bias. First, forecast error has been significant in 4 out of the last 12 months. All significant errors were underestimations. Second median forecast error has tended to be very biased, underestimating PCE in 11 out of the last 12 reports, and for the last 11 consecutive months. The average forecast underestimated PCE growth by +0.2% in the last 12 months.

History of BEA Revisions

Forecasters try to forecast what the BEA’s estimates will be, but the BEA’s own estimates contain a significant margin of error. The BEA subjects the data to up to 5 regular monthly revisions, plus annual and 5-year revisions. These revisions can be significant, and even the final estimate contains a significant margin of error.

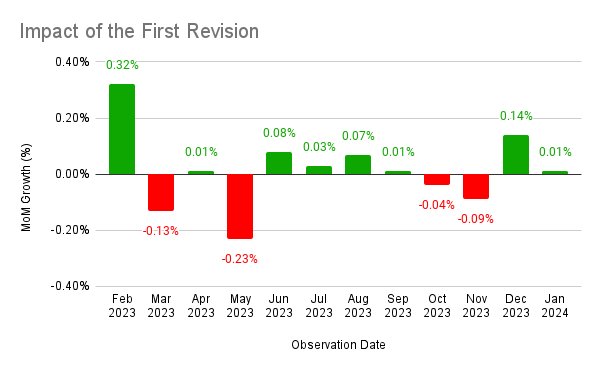

The BEA’s estimation errors (between the first and second revision) have tended to be relatively small this year. However, the errors have been somewhat biased, underestimating Real PCE in 8 out of the last 12 reports.

Figure 4: Difference Between the First Revision and the First Estimate

Impact of Revisions on Real PCE (ALFRED & Investor Acumen)

It is important to understand that net revisions have the same impact on monthly and quarterly nowcasts and forecasts of GDP as the forecast surprises pertaining to a single month. Therefore, it is important for readers to factor in both the forecast surprises and revisions in assessing the potential economic impacts and market impacts of the PI&O data releases in a given month.

U.S. Economy Outlook: Scenario Analysis

In this section, we review three scenarios. The first scenario is one in which the median forecast of professional economists proves to be accurate. The second scenario is one in which the reported data surprise to the upside. The third scenario is one in which the reported data surprise to the downside. The objective in this section is to anticipate the implications of each of these scenarios for the economic outlook in the U.S. and for financial markets.

Scenario 1: Forecasts are Accurate

The median forecast of professional economists expects the BEA to report that personal spending grew at a rate of +0.50% percent during the most recent month (51st percentile). Assuming that this forecast is correct and that there were no revisions to prior data, the 3-month annualized change of Personal Spending would have been a +2.17% growth rate, ranking in the 34th percentile historically.

The implications for forecasts and outlooks of various key macroeconomic conditions are as follows:

1. Business cycle risk. A below-average growth rate of Personal Spending (34th percentile) during the past three months would indicate that the risk of a business cycle recession has increased slightly relative to the previous 3-month period in which growth was above average. However, the absolute level of recession risk in the next 6 months remains very low. It should be noted that because the US economy is in the Late Expansion stage it is more vulnerable to an exogenous shock than during other stages.

2. Economic Activity. If the reported numbers are roughly in line with forecasts, the rate of change of Personal Spending, on a 3-month annualized basis will have grown at a +2.17% rate, which ranks in the 34th percentile historically. Such a scenario should not bring about any major changes in forecasts of U.S. economic activity.

3. Inflation. The U.S. economy is currently operating at, or near, full capacity; labor and capital resource utilization rates are very high. Under these conditions, it is generally believed that the aggregate rate at which the supply of goods and services can grow in the U.S. economy – without causing acceleration of price inflation – is below average. Since the current median forecast expects personal spending to grow at a below-average pace, all things being equal, the rate of inflation should be expected to remain roughly stable at the current high level.

Scenario 2: Upside Surprise

Let us assume that the reported data exceed the median forecast by a significant margin as has been the case in 8 of the past 12 months. What would be the implications?

1. Business cycle risk. Even lower. An upside surprise would reduce estimates of near-term business cycle risk even further, from levels that are already very low. However, perceptions of intermediate-term risk could increase if overly “hot” personal spending growth raised the risk of tighter-than-expected monetary policy.

2. Economic activity. Forecasts upgraded. A significant net upside surprise in the PCE data would cause forecasters to upgrade their estimates regarding the rate of economic activity in the U.S. Forecasts of GDP growth, which are currently within a historically average range could be upgraded to expectations of an above-average rate.

3. Inflation forecasts. Greater acceleration. Under current conditions, with resource utilization (labor and capital) at very high rates, a significant net upside surprise in the PCE data would increase expectations of accelerating inflation above and beyond current forecasts.

Scenario 3: Downside Surprise

Let us assume that the reported data falls short of the median forecast by a significant margin. What would be the implications?

1. Business cycle risk. Moderately higher. A downside surprise would moderately increase estimates of near-term business cycle risk, from very low levels. However, perceptions of business cycle risk in the intermediate-term risk could become more complicated due to the increased risk of a potential monetary policy error (i.e., cutting interest rates too soon while inflation is still too high).

2. Economic activity. Forecasts downgraded. A significant net downside surprise in the PCE data would cause forecasters to downgrade their estimates of the rate of economic activity. Forecasts of GDP growth, which are currently within a historically average range, could be downgraded to expectations of a below-average rate.

3. Inflation. Forecasts moderately lowered: A significant net downside surprise in the PCE data could cause forecasters to lower their inflation forecasts. Despite the fact that resource (labor and capital) utilization rates are high, growth of consumer demand that is lower than the potential growth of supply will, all things being equal, tend to cause inflation to decelerate.

Market Outlook

In this section, we will discuss potential market reactions under different scenarios.

First, we would point out that the PCE Price Index data could become a show-stopper if it comes in significantly above expectations. Fed Governor Waller alluded to this possibility in a speech on Wednesday evening, and some speculate that he may have gotten a peak at the data. Although I doubt that this is the case, I agree with Waller that a strong PCEPI number should cause expectations of Fed rate cuts in 2024 to be pulled down and pushed out significantly.

Second, particularly strong or weak Personal Spending figures could make a big difference regarding expectations of Fed rate cuts. We would note that Chairman Powell is scheduled to speak on Friday at 11:30 AM.

Concluding Thoughts

Our team at our Investing Group is generally of the view that the overall macroeconomic environment in the U.S. and globally presents good reward-to-risks prospects for a very select group of equities. However, for several months, we have been positioning our portfolios in a manner that accounts for likely disappointments of market expectations regarding Fed policy. We are also growing increasingly concerned about inflation risks in the second half of 2024. Indeed, we think that very unusual opportunities are going to emerge in the second half of 2024, starting sometime between June and August.