")

")

Introduction

In my previous report on Palo Alto Networks, Inc. (NASDAQ:PANW), I expressed appreciation for the “Accelerated Platformization” strategy whilst downgrading PANW stock to a “Hold” rating due to its premium valuation:

In my mind, the push for an acceleration in platformization is more of a poker move than panic discounting from Palo Alto Networks’ seasoned leadership team. And not many cybersecurity firms can do such bundling!

Heading into the report, we held a 4.2% position in PANW within our GARP portfolio. Given the 26% post-ER slump, I understand the temptation for long-term investors to jump in to buy the dip. While I see no reason to worry about Palo Alto Networks’ as a business, the stock is still trading above its fair value and its expected 5-year CAGR of 13.28% doesn’t exceed our investment hurdle rate of 15%. Therefore, I am assigning a “Hold” rating for PANW.

If Palo Alto Networks were to keep sliding lower, I will restart accumulation of PANW as soon as its projected CAGR return exceeds our hurdle rate. FYI, this buying level is ~$250 per share.

Source: Palo Alto Networks Q2 FY2024: Arora Fumbles, Stock Tumbles

Since then, Palo Alto Networks’ stock has moved up from ~$270 to ~$310, and with its Q3 FY2024 report, we have now received data-based evidence that the platformization push at PANW is working. In today’s note, we will briefly review Palo Alto Networks’ Q3 FY2024 results and re-evaluate PANW’s long-term risk/reward to formulate an informed investment decision.

Analyzing Palo Alto Networks Q3’FY24 Report

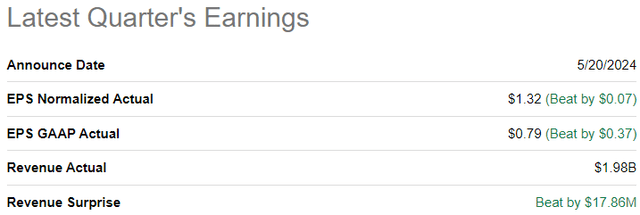

Heading into its Q3 FY-2024 report, Palo Alto Networks was projected to deliver revenues and normalized EPS of $1.96B and $1.25, respectively. Despite beating consensus street estimates on both top and bottom lines [revenue: $1.98B (up +15% y/y), normalized EPS: $1.32], Palo Alto Networks stock plummeted by ~9% to $293 per share in the immediate aftermath of the report, only to recover back to the low $300s in yesterday’s session.

Seeking Alpha

While PANW stock is moving all over the place as Mr. Market goes through a price discovery exercise in light of new information, investors clearly stepped in to buy the post-ER dip. Let’s dig in further to understand why!

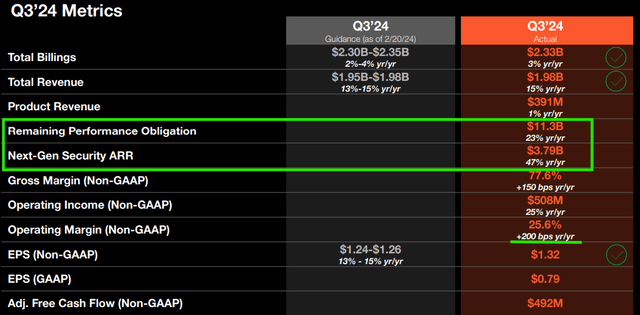

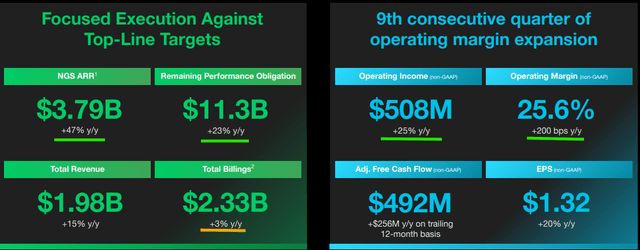

In Q3 FY2024, Palo Alto Networks’ revenue of $1.98B (+15% y/y) came in at the high end of management’s guidance range, driven by robust growth in Next-Gen Security business [ARR: $3.79B, up +47% y/y].

Palo Alto Networks’ Q3 FY2024 Report

With more and more customers opting for annual plans, Palo Alto Networks’ billings growth slowed down to +3% y/y; however, more importantly, PANW’s RPO growth rate ticked up to +23% y/y in Q3 – indicating a strong demand backdrop for the cybersecurity industry and PANW’s Network Security, Cloud Security, and Security Operations platforms.

Palo Alto Networks’ Q3 FY2024 Report

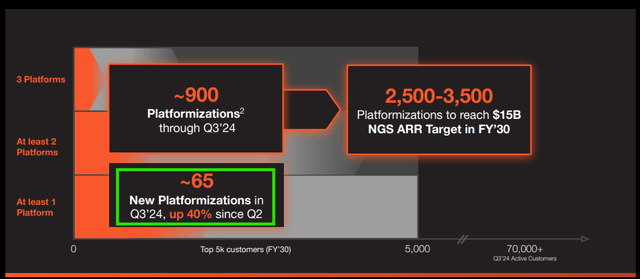

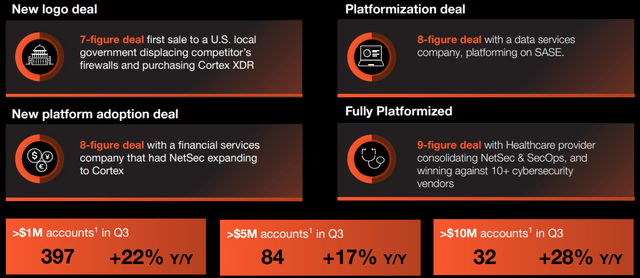

Last quarter, Palo Alto Networks’ seasoned leadership launched an “Accelerated Platformization and Consolidation” strategy, wherein PANW is offering its “platforms for free” for a limited time period in exchange for long-term platform commitments from its customers. With ~65 “New Platformizations” in Q3 FY2024 (40% higher than Q2), customers are clearly biting at Palo Alto Networks’ lucrative offer!

Palo Alto Networks’ Q3 FY2024 Report Palo Alto Networks’ Q3 FY2024 Report

Here’s some management commentary from the Q3 FY2024 earnings press release and conference call:

We are pleased with the enthusiastic response to platformization from our customers in Q3. Platformization is a long-term strategy that addresses the increasing sophistication and volume of threats, and the need for AI-infused security outcomes.

I’m delighted to report, despite the concerns around our platformization approach after our last quarter, the customer feedback has been nothing but encouraging. We have initiated way more conversations in our platformization than we expected. If meetings were a measure of outcome, they have gone up 30%, and a majority of them have been centered on platform opportunities. In short, demand is robust, and my expectation is that we will continue to see it be that way over the next many quarters.

– Nikesh Arora, Palo Alto Networks’ CEO

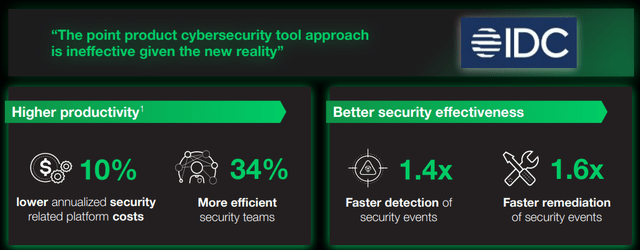

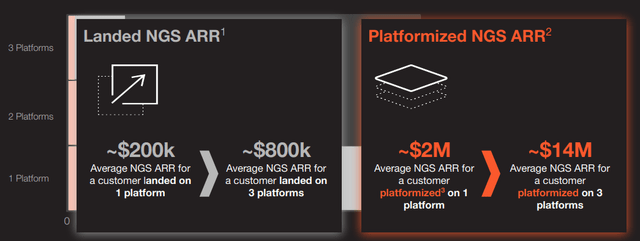

In terms of impact, the accelerated platformization offers are set to hurt near-term billings and revenue growth at Palo Alto Networks. However, by standardizing on Palo Alto Networks’ platforms, customers like IDC get higher productivity and better security outcomes. With “Platformized” NGS customers yielding an ARR of $2M to $14M [1 to 3 platforms] versus “Landed” NGS ARR of $200K to $800K, the rationale for accepting short-term revenue and billings pain is more than sound.

Palo Alto Networks’ Q3 FY2024 Report Palo Alto Networks’ Q3 FY2024 Report

The initial results of Palo Alto Networks’ “Accelerated Platformization and Consolidation” strategy are impressive, and I now feel a lot more comfortable about management’s FY2030 NGS ARR projection of $15B [+25% CAGR growth in NGS ARR for the next six years].

Now, despite offering freebies to entice customers into platformization, Palo Alto Networks’ operating leverage story remains robust, with non-GAAP operating income rising by +25% y/y to $508M (operating margin: +25.6% [+200 bps y/y]) and diluted EPS increasing +20% y/y in Q3 FY2024.

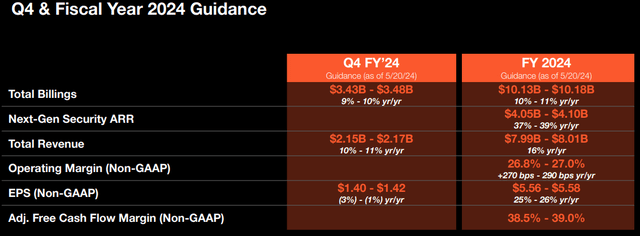

For FY-2024, Palo Alto Networks’ management is now guiding for revenue to be in the range of $7.99-8.01B [+16% y/y growth, up from $7.95-8B in Q2’FY2024], with billings projected to come in at $10.13-10.18B, in line with previous guide of $10.1-10.2B.

Palo Alto Networks’ Q3 FY2024 Report

Overall, Palo Alto Networks’ Q3 FY2024 report was better than expected, and I see a bright future ahead for this cybersecurity giant. That said, we still have further growth moderation ahead of us, with the re-acceleration back up to 15% CAGR at least three quarters away.

Given PANW’s Q4 FY2024 guidance [10-11% y/y revenue growth and negative y/y earnings growth], I think its richly valued stock could come under some selling pressure over the next 6-9 months in the event of a broad market pullback or correction.

PANW Stock Fair Value And Expected Return

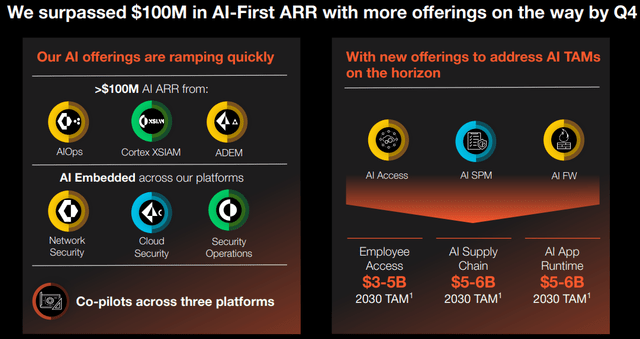

Over the next 5-6 years, Palo Alto Networks’ leadership is looking to double their business once again, with NGS ARR projected to grow from $4B in FY2024 to $15B in FY2030, and additional growth potential from AI, which is expected to boost PANW’s FY2030 TAM by ~$17B.

Palo Alto Networks’ Q2 FY24 Presentation

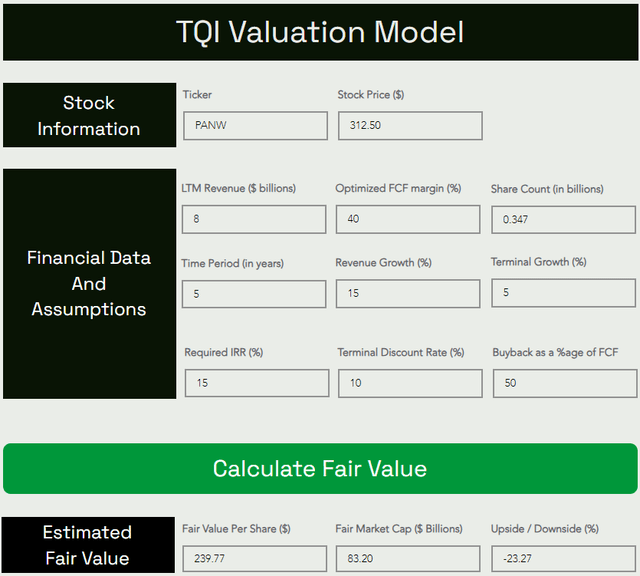

While Palo Alto Networks is set to experience slower top-line growth for the next three quarters, a re-acceleration back up to the mid-teens level within 12-18 months seems inevitable, given the strong initial customer response to PANW’s “Accelerated Platformization” strategy. Considering PANW’s “higher growth for longer” guide and AI potential, I am choosing to look beyond near-term growth rates in maintaining my 5-year CAGR sales growth assumption at 15% (which was somewhat conservative, to begin with). All other assumptions are relatively straightforward, but if you have any questions, please share them in the comments below.

Here’s my updated model for PANW:

TQI Valuation Model (Free to use at TQIG.org) TQI Valuation Model (Free to use at TQIG.org)

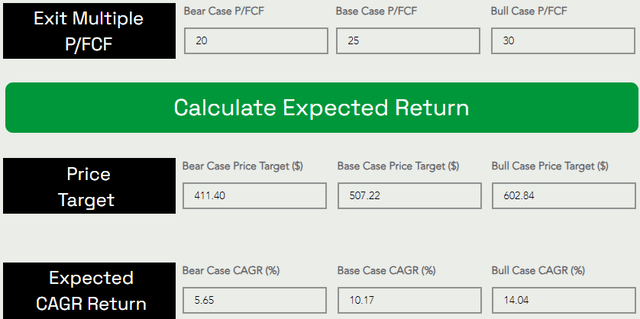

Assuming an exit multiple of 25x P/FCF, Palo Alto Networks stock could rise from $312.5 to $507.2 per share at a CAGR rate of 10.17% by 2029. With PANW’s expected CAGR returns falling well short of my investment hurdle rate of 15%, I am not a buyer here. Now, given that PANW’s expected CAGR is more or less in line with long-term S&P 500 (SP500) returns of 8-10% per year, I am also not a seller at these levels.

Concluding Thoughts: Is Palo Alto Networks Stock A Buy, Sell, or Hold?

Palo Alto Networks is a high-quality cybersecurity company that’s currently going through a transitional period amid a strategic shift to “Accelerated Platformization”. As evidenced by Q3 FY2024 results, PANW’s push for platformization is the right way to go for the long term, despite its near-term impact on top-line growth. At TQI, we continue to own PANW stock within our GARP portfolio, and here’s my plan of action for the next 12-24 months:

- If PANW stock declines to its fair value of $240, I will restart accumulation.

- If PANW stock rises to the high $300s (expected CAGR falls under 5%), I will trim opportunistically [like we did in the past].

Key Takeaway: I rate Palo Alto Networks “Hold/Neutral” at $312.5 per share.

Thanks for reading, and happy investing. Please share your thoughts, concerns, and/or questions in the comments section below.

Q2 2024 Earnings Call Transcript")