")

Investment summary

My recommendation for Oracle (NYSE:ORCL) is a buy rating, as I am confident that ORCL can hit its FY26 targets given its solid execution and growth momentum. In particular, leading growth indicators are suggesting growth acceleration ahead. On a relative valuation basis, ORCL also screens really well against SAP, which is trading at >30x forward PE while having a similar growth rate as ORCL but lower profit margins. As ORCL shows that it can accelerate growth to meet its FY26 targets, I believe the current valuation is sustainable and could potentially revert upwards.

Business Overview

Oracle is a large player in enterprise software and hardware products and services, with a large presence in database management, storage and networking products, and cloud infrastructure products. Historically, ORCL used to sell product licenses that come with maintenance packages but has since gone through a transition to a cloud/hybrid model where they started offering subscription services to customers. As of 3Q24, cloud revenue is around ~35% of total revenue (based on my own calculation). In terms of cash generation, ORCL has been generating huge amounts of free cash flow over the years, averaging ~24% FCF margin over FY20, or $60 billion in absolute amount. These FCF are typically returned to shareholders via dividends (~1+% yield) and share buybacks (bought back ~39% of shares outstanding since FY14).

Solid growth momentum

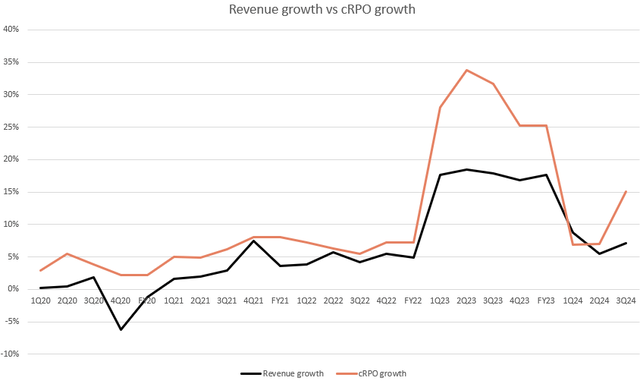

The solid execution by ORCL led me to believe that its growth momentum can continue for the foreseeable future. Talking back to the 3Q24 results, total revenue saw $13.28 billion, 7.1% growth, pro forma EBITDA saw $5.792 billion, a 43.6% margin, and pro forma EPS lands saw $1.41. The remaining performance obligations [RPO] increased to over $80 billion, driven by new, large-scale cloud infrastructure deals signed in the quarter. This is the most important highlight because it shows strong growth momentum. After adjusting for Cerner acquisitions and FX, total RPO growth reached 41%, which is even better than the 29% reported growth. Within the next twelve months, around 43% of RPO is expected to be captured as revenue, which would indicate a growth of around 15% year-on-year in cRPO, or approximately $34-35 billion. In my opinion, the bigger implication is that it reflects the growing trend of customers’ demand for Oracle Cloud Infrastructure [OCI]. In particular, ORCL capturing NVIDIA as a customer stands out, which in my view, further proof of OCI’s competence.

Redfox Capital Ideas

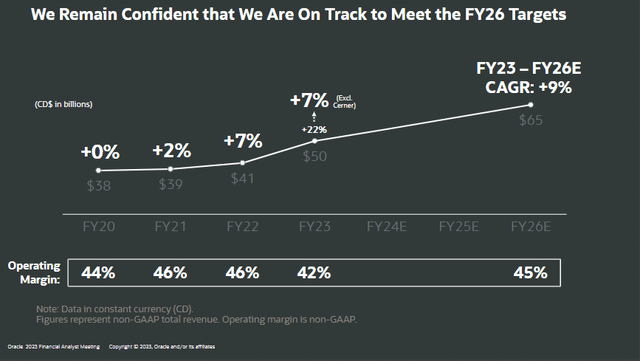

The main drawback that some investors might have with using RPO as a leading indicator for revenue growth is the widening gap between revenue growth and cRPO growth. Considering the potential impact of contract lumpiness and constraints in building data center – which have impacted ORCL ability to implement its products, I don’t think this is cause for alarm. My view is that eventually, this gap will converge just like it did in the past, which means growth is poised to accelerate from here. Hence, I strongly believe that ORCL will be able to meet its FY26 guidance revenue of $65 billion, which implies ~24% growth over the next 2 years, or average of 12%/year (which is below cRPO growth and a lot lower than RPO growth). I should also note that RPO Bookings (RPO + revenue) in 3Q24 saw 106% growth, which is a very strong indicator of demand strength.

Growth concerns not a big issue

I would also like to address two growth concerns that investors might have. Firstly, ORCL Fusion Cloud ERP growth continues to decelerate, but to be fair, the deceleration is so big that it deserves a big red flag (constant currency growth decelerated by 200 bps since 1Q24 to 18% in 3Q24). If we look at NetSuite ERP, constant currency growth was actually pretty stable at 20%, the same as in 2Q24. In the overall scheme of things, where rates are high—pressuring businesses to spend as the cost of capital is relatively higher than a few years ago—I think this actually shows how resilient ORCL is. Also, ORCL is not the only one suffering; this is an industry-wide problem. Secondly, the recently acquired Cerner has relatively underperformed compared to the rest of the business, which is a drag on the consolidated growth rate. I think it’s too early to say that Cerner is a problem child because ORCL has just released the refreshed version of the Cerner application, which should see an uptick in demand. Management guidance for Cerner is also very encouraging, as they expect it to return to growth next year.

Valuation

Redfox Capital Ideas

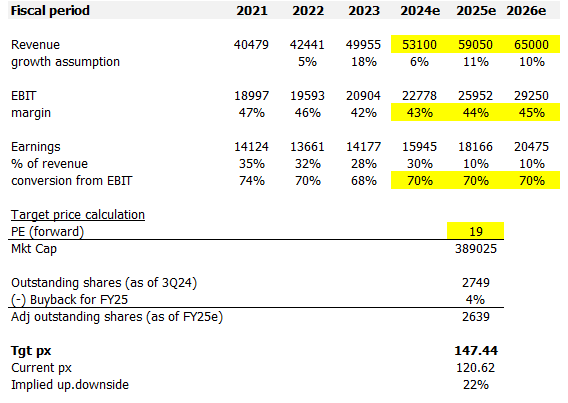

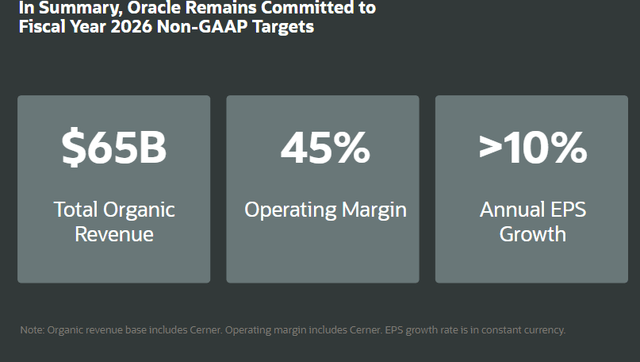

I model ORCL using a forward PE approach, and using my assumptions, I believe ORCL is worth $147. My model revolves around ORCL’s ability to meet its FY26 targets laid out in the previous analyst day, and I am highly confident that it can do so. Assuming modest mid-single-digit growth for 4Q24 (5%), I got to $5.3 billion in FY24, and from there I linearly extrapolated revenue to meet the $65 billion organic revenue target. I did the same for EBIT margins, forecasting linear progression towards the 45% target. Margin should expand as ORCL grows its topline to cover the fixed costs that have been invested in the company over the past two years. Note that ORCL has historically seen margins >45%, so achieving 45% is not an impossible target. While ORCL currently trades above its historical average multiple, I think valuation is going to sustain itself at this level given the growth outlook. Comparing ORCL against its best-known peer, SAP, also suggests that ORCL valuations are not that expensive. SAP is expected to grow low teens, while ORCL has guided for high single-digit growth, but ORCL has a higher profit margin profile than ORCL. On a comparatively small basis, I would assume ORCL to trade at least in line with SAP, which is trading at 32x forward PE today. Hence, at 19x, I don’t think the ORCL valuation is demanding.

ORCL

ORCL

Risk

The slowdown in business spending could worsen as there is a growing chance of the Fed not cutting rates in the coming months, given that inflation is higher than expected and is outside of Fed expectations. This announcement came just weeks after Powell said that they remained confident in cutting rates as per original intention. This basically introduced more uncertainty into the market, and I think businesses could become more conservative in planning their budget, thereby impacting ORCL’s growth.

Conclusion

My view for ORCL is a buy rating as the recent strong execution gave me confidence that ORCL can meet its FY26 targets. Solid growth momentum is evident, with RPO as a leading indicator. While growth concerns exist in Fusion Cloud ERP and Cerner, I believe they are not significant issues. Valuation is also supported by the positive outlook and compares favorably to peers like SAP. The main risk is a potential slowdown in business spending due to the Fed’s recent stance on interest rates.

Q1 2024 Earnings Call Transcript")

")