")

: Earnings And Proposed Debt Exchange Are Not Assuring")

Last week, Office Properties Income Trust (NASDAQ:OPI) reported first quarter earnings. The commercial office REIT surprised analysts to the positive on the revenue side, but disappointed on FFO. Along with the earnings announcement, Office Properties announced a proposed debt exchange. Due to the debt exchange proposal, shares rallied, and short-term bonds tanked. The latest earnings report, combined with the need for a debt exchange is keeping me out of investing in Office Properties’ stock and bonds.

FINRA

Office Properties Financial Performance

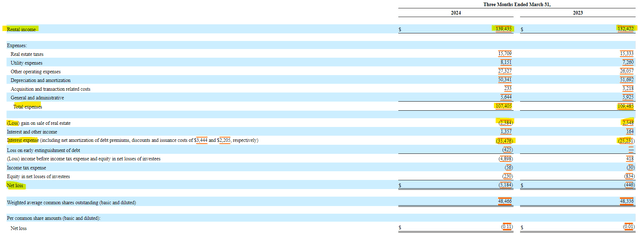

Office Properties saw first quarter revenue grow by $7 million to $139 million. The company was also able to control expenses with a decline of $2 million to $107 million. Unfortunately, those gains were entirely absorbed by the $10 million increase in interest expenses as the company has become more debt dependent on operating over the past few years.

SEC 10-Q

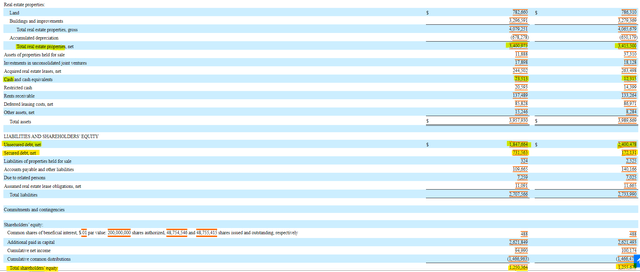

On the balance sheet side, Office Properties saw nominal changes in all areas except for its debt structure. While debt levels stayed relatively the same at just under $2.6 billion, unsecured debt declined by $550 million and secured debt rose by the same amount. This was because the company issued secured notes and used revolving credit to pay off unsecured debt coming due this year. Unsecured debtholders and equity investors need to take note that the growth in secured debt creates a new class of investor senior to them and can influence the impairment of their returns in the event of distress.

SEC 10-Q

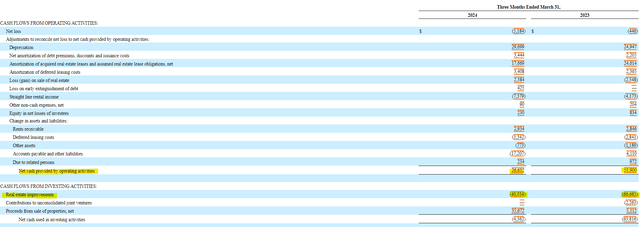

Perhaps the biggest concern for investors comes in the form of the cash flow statement. Office Properties’ cash flow from operations declined to under $27 million in the first quarter, compared to $52 million in the same quarter a year ago. With the level of capital expenditure required to maintain the properties above operating cash flow, Office Properties is not generating enough cash to support a dividend or debt service.

SEC 10-Q SEC 10-Q

The Next Challenges Ahead for OPI

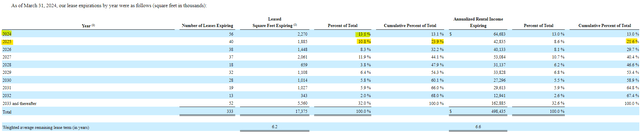

Despite the growth in revenue, Office Properties is facing a leasing problem. The company saw a five basis point drop year over year in leasing across all properties and across comparable properties. Additionally, the company is facing nearly a quarter of its leases expiring between now and the end of next year, which accounts for more than 20% of its total leasing revenue.

SEC 10-Q SEC 10-Q

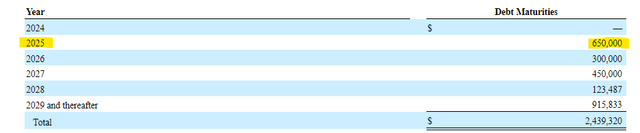

The company’s upcoming debt maturities aren’t making the situation any easier for management. Office Properties is facing debt maturities in each of the next three years of $650 million, $300 million, and $450 million, respectively. The cost of refinancing all this debt combined with the leasing headwinds has the potential to create a doom loop in operating cash flow, which is why the company is turning to a debt exchange.

SEC 10-Q

Details of the Office Properties Debt Exchange Offer

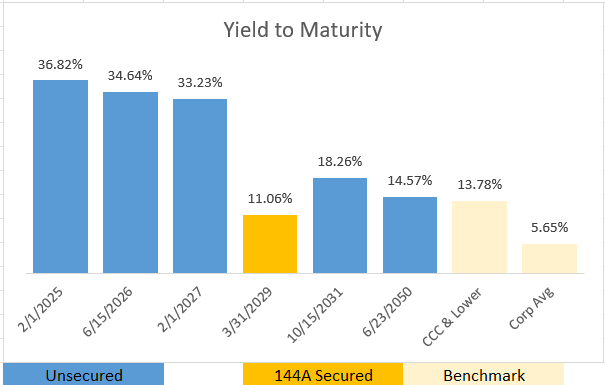

Office Properties is offering to exchange unsecured notes of various maturities with up to $610 million of senior secured notes maturing in 2029. The company has yet to price a coupon on the senior secured notes, but it will likely be comparable to the recent 9% notes. Preference will be given to noteholders of 2025 maturing notes at 93.8 cents on the dollar for early exchange consideration. After that, the exchange rate plummets to between 51.5 and 72 cents. Should the entire 2025 noteholders group participate, there will not be enough capital for the subsequent 2031, 2027, or 2026 noteholders to tender their notes. The debt exchange has led to a credit downgrade from S&P to CC.

SEC 8-K Press Release SEC 8-K Press Release

The exchange offer has eroded the value of the 2025 through 2027 notes and while some investors may see an arbitrage opportunity in the 2025 notes, I’m cautious. Should the 2025 notes not be tendered at an adequate level, Office Properties is going to have to find a way to refinance them in a way that makes their large senior secured class comfortable. The company cannot afford and will not be allowed to have capital exit the business in exchange for the repayment of principal on unsecured debt.

A Silver Lining for OPI?

Office Properties has been able to sell properties through the disruption in its space, albeit for amounts immaterial to the challenges. The possibility of selling other unencumbered assets could be helpful in raising the cash needed to support the day-to-day operations. The company also has sufficient liquidity to support itself between now and the 2025 debt maturity, giving it some time to figure its capital structure out.

Earnings Release

Conclusion

If I were a holder of short-term Office Properties debt, I would take the exchange offer and sell my position shortly after completion. A successful exchange offer in the 2025 note class will lead to higher interest expenses and the need for another exchange to deal with the 2026/2027 notes. Other than by increasing lease activity with higher rents, I’m not seeing another path for Office Properties Income Trust to emerge from its current trajectory.

")

")

")