2026-08-05")

The discipline to stay boring

June 30, 2026

“Investing should be more like watching paint dry or grass grow. If you want excitement, take $800 and go to Las Vegas.” — Paul Samuelson, Nobel Prize winning economist

Before writing these quarterly commentaries, I always reread my most recent editions. Unfortunately, much of what I wrote last quarter still applies ( Why didn’t we do better when value outperformed? ). Through June 30, the Oakmark Fund was flat for the year, trailing double-digit gains for both the S&P 500 and the Russell 1000 Value Index. As in the first quarter, index returns were driven by a sector we didn’t own—a small group of high price-to-earnings (P/E), cyclical technology companies, currently benefiting from increased AI spending. Here is a list of the year-to-date top performers in the Russell 1000 Value Index:

Source: FactSet, as of 6/30/2026. Past performance is no guarantee of future results. Chart is for informational purposes only and does not depict the performance of any Harris | Oakmark strategy or product. Returns shown reflect the period during which each security was a constituent of the Russell 1000 Value Index. Following the index reconstitution effective 6/26/2026, certain securities shown above are no longer members of the index. Price-to-earnings ratios represent the average consensus trailing twelve-month (LTM) P/E ratio for each security as of 12/31/2025.

These 10 companies, out of an index containing 863, accounted for nearly half the index’s gain through the first half of 2026. They began the year with a median trailing P/E ratio of 27x, significantly higher than even the S&P 500. By comparison, the Oakmark Fund portfolio, with an estimated 2026 P/E of only 11.7x, looks much more like a traditional value portfolio. That hasn’t helped our recent performance. If you exclude AI-related stocks and the energy companies powering them, the S&P 500 would be down year to date.

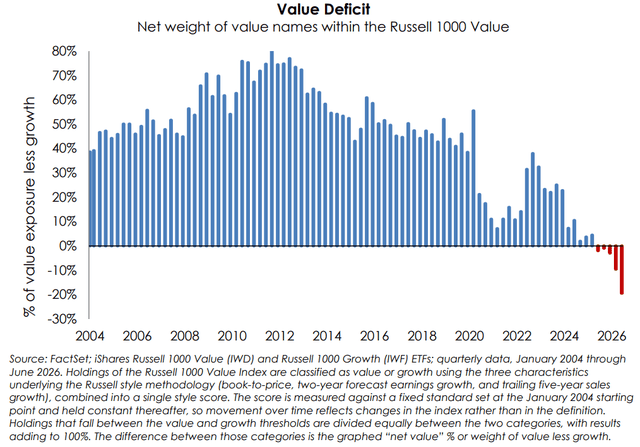

An interesting aside: In last month’s Russell Index rebalance, Apple (AAPL) and Microsoft (MSFT) became new members of the Russell 1000 Value Index. As part of that rebalance, Amazon’s (AMZN) Russell value score rose from 27% to 92%. As a result, a significantly larger share of its market capitalization was included in the index, making Amazon the index’s largest holding. Using Russell’s own classification of whether a stock is value or growth shows just how much the market has changed. For most of the past 25 years, stocks Russell deemed value comprised the overwhelming majority of the Russell 1000 Value Index. Today, the majority is growth. The extraordinary increase in AI infrastructure spending is pushing all but the “growthiest” growth companies into the Russell Value Index.

Given the obvious parallels between today’s AI-driven market and the Internet market 27 years ago, we are increasingly asked whether we expect a repeat of the dot-com bust. Anyone answering that with certainty is suffering from overconfidence. There are clear similarities: a once-in-a-generation technological advance, extraordinary gains concentrated in a narrow part of the market, newly minted fortunes and widespread concern about how the new technology may reshape the economy. Perhaps just as important is the similarity in investor behavior.

In more typical markets, conversations with clients and prospective clients focus on the companies we’ve purchased. Today, it is nearly impossible to interest someone in why we believe Corebridge Financial, trading at less than 6x next year’s expected earnings, could reasonably be worth 9x. Instead, most conversations quickly turn to why we didn’t buy companies such as Dell, Micron (MU) or Intel (INTC) that are now widely viewed as the obvious beneficiaries of AI.

I’ve noticed the same shift outside the investment industry. One tech industry friend discovered that employee stock options that he had long since written off had become worth more than $1 million on paper. When I congratulated him and asked whether he had locked in some of that life-changing gain, he looked at me as though I’d missed the point: why sell something that goes up every day? So far, he’s been right. At a charity dinner, I met someone who told me he was leaving his job to trade ETFs full-time after four years of earning more than 30% annually. Curious, I asked what strategy he followed. “I only own the funds,” he explained, “on the days when it’s obvious they’ll go up.”

This growing belief that exceptional stock market returns are easy to achieve feels familiar. When we’re all within “six degrees of separation” from a SpaceX billionaire, it’s hard to feel satisfied compounding wealth at a “mere” 10% per year (Oakmark Fund’s approximate trailing five-year return).

Although investor behavior may be reminiscent of the dot-com era, we believe there are also important differences. Many of the market’s biggest winners in the late 1990s were newly formed companies, with little or no profitability, whose valuations depended almost entirely on future possibilities. Today’s leaders are mostly established, highly profitable businesses. In fact, if we were to extrapolate their growth for just a few more years, they would trade at valuation multiples below the broader market.

The difficult question is how long today’s environment can persist. Will AI chips remain a near monopoly a decade from now? Will historically cyclical industries such as memory, semiconductors and computers continue to enjoy shortages and unusually high profit margins? Or will we eventually look back on today’s profitability as a cyclical peak? Perhaps these businesses have permanently changed, much as Apple rose above the boom-bust cycles of the consumer electronics industry. Or maybe this resembles oil stocks when crude reached $150 per barrel, and many argued that $200 was the new normal.

We haven’t been able to answer those questions with enough confidence to justify owning the AI hardware stocks. That doesn’t mean we believe they’re wildly overvalued. It simply means we cannot conclude they are selling at prices that provide the margin of safety we require relative to the future cash flows they are likely to generate.

Some have suggested that this makes us “AI bears.” We don’t see it that way. First, we think many of our portfolio companies stand to benefit from AI, and their management teams agree. Capital One (COF) is using AI to reduce the cost of credit authorization and customer service. AIG (AIG) is applying AI to improve and expedite underwriting decisions. Alphabet continues to invest heavily in Gemini and Google Cloud while Amazon Web Services is seeing growth accelerate from AI demand. We expect many of our companies to become more valuable because of AI.

Second, we don’t define portfolio risk by what we don’t own. It has become increasingly popular to think about risk in terms of how much a portfolio differs from an index. If you view risk as performing different than an index, then “I don’t know” means defaulting to the index weight. We see risk differently. We look at risk company by company and ask, “What is the probability our thesis could be so wrong that this company’s business value falls to less than its stock price?” The outcome we are trying to avoid is generating investment returns that end up meaningfully on the wrong side of zero. Of course, we believe that over long periods, this approach will lead to higher returns than an index fund, but we don’t believe that lagging behind a high-performing index, even for a few years, is evidence our strategy no longer works.

So, what should you expect from us as AI usage continues to advance? You will never see us buy an AI company—or any other company—simply because it is popular or heavily represented in an index. Likewise, we won’t avoid an AI company simply because it has become fashionable.

To us, there is no difference in how we evaluate an insurer, an industrial manufacturer or an AI-related company. We will estimate the stock’s fair value based on estimated future cashflow and will only buy if the market price is at a large discount. We will also evaluate management teams and will only invest if they are focused on maximizing long-term, per-share business value. Whether that ultimately leads us to more or less AI exposure than other investors is unimportant to us because we don’t believe it materially changes the likelihood of achieving long-term financial goals.

We believe the “boring” companies we own represent the genuine “value” portion of the Russell Value Index today, exposure that is minimal for most index funds. Staying focused isn’t easy when others appear to be making effortless money. When someone doubles their money betting on red in roulette, we instinctively understand that black was just as likely. The risk of loss is less obvious when looking at winning stocks. We stay grounded by following the operating performance of the businesses we own rather than the share prices of the businesses we don’t.

Next quarter’s commentary will be our annual Q&A with Oakmark shareholders. If you have questions you’d like us to answer, please email them to [email protected] . And if anyone asks, I’d be happy to explain why we think Corebridge is attractive!

Thank you for your continued interest and investment with Harris | Oakmark.

William C. Nygren, CFA Portfolio Manager

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.