")

")

Written by Nick Ackerman, co-produced by Stanford Chemist.

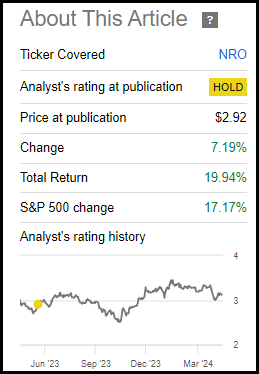

We last covered the Neuberger Berman Real Estate Securities Income Fund (NYSE:NRO) around a year ago. At that time, I had rated the fund as a ‘Hold’ despite the deep double-digit discount to its net asset value per share that the fund was trading at. In hindsight, it should have been rated a ‘Buy’ as the performance of the fund was quite strong. However, a large driver of this was simply the fund’s discount narrowing over this time. Today, I would still rate it the same, and I believe there are a couple of peers that look like more interesting bets.

NRO Basics

- 1-Year Z-score: 1.89

- Discount: -3.99%

- Distribution Yield: 11.96%

- Expense Ratio: 1.4%

- Leverage: 22.54%

- Managed Assets: $221.869 million

- Structure: Perpetual

NRO’s investment objective is “high current income. Capital appreciation is a secondary investment objective.” To achieve this, the fund will “develop a portfolio with a broad mix of real estate securities through superior stock selection and property sector allocation.”

They continue that they can invest primarily in “securities issued by Real Estate Companies, including REITs.” They don’t exactly specify, but that does include both the common and preferred securities issued by REITs.

Alternatives To NRO

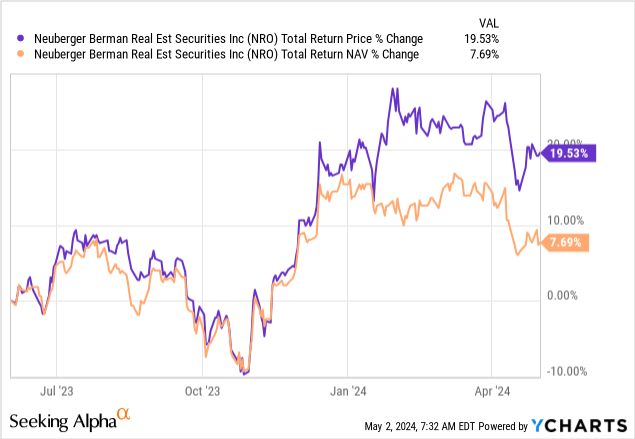

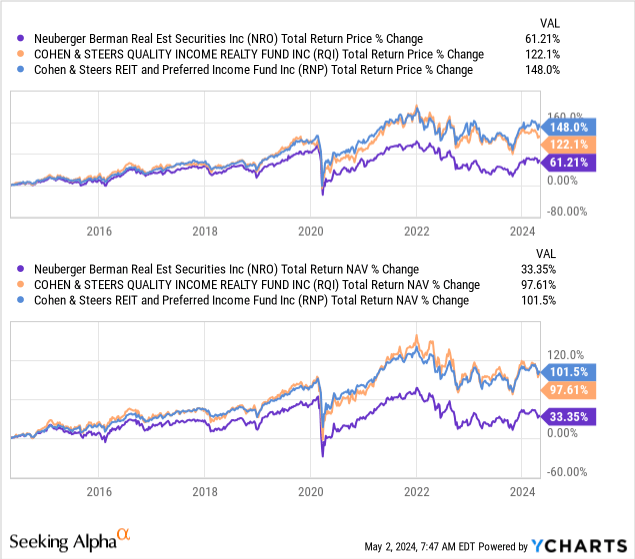

Since our last update, the fund’s total returns have outpaced those of the S&P 500 Index-though it did dive lower in the broader market correction of October. Still, overall, the results here were impressive.

NRO Performance Since Prior Update (Seeking Alpha)

In hindsight, I should have been more bullish on this name with a ‘Buy’ rating, as my conclusion even leaned toward that direction.

While I don’t necessarily see NRO as a long-term hold type of position, an argument could be made as it could be seen as a diversifier. Most of my REIT exposure is tied up to C&S, and they could start underperforming, as history is no guarantee of future success. All that being said, I believe that NRO is attractive due to the current discount on the fund. At this level, historically, the fund has tended to bounce. If you are a long-term holder, taking advantage of dollar-cost averaging down could be worth considering too.

That said, I would still remain at a ‘Hold’ rating today. A strong and primary driver of these results was merely the fund’s discount narrowing over this time as the fund’s underlying performance – as measured by the NAV – was relatively weaker. When covering this previously, the fund had a 1-year z-score of -2.30 and a discount of -13.54%.

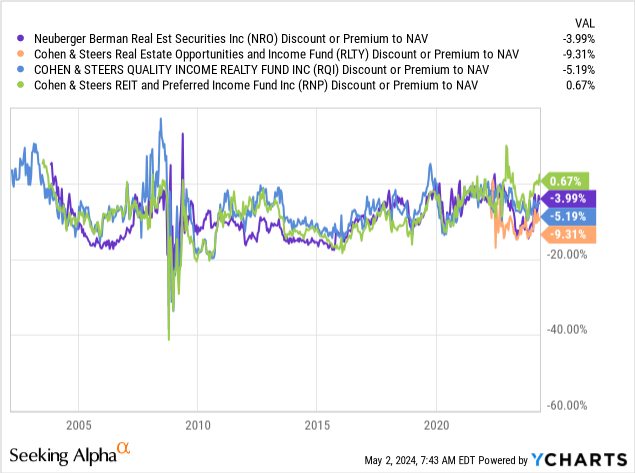

The wide double-digit discount has moved to a lower single-digit discount now. The divergence primarily played out as we entered 2024 when the fund’s discount really started to narrow as the share price became elevated.

Ycharts

While my rating wasn’t as bullish as it should have been in that last article, given the performance we see now, it is a good reminder of how discounts/premiums can be played when it comes to closed-end funds to help identify attractively valued investments.

With where NRO is trading today, I believe there are a couple of alternatives that investors could consider. As I noted in our prior update, NRO invests somewhat similarly to the Cohen & Steers REIT and Preferred and Income Fund (RNP), which is split between preferred and equity positions. RNP is about 50/50 allocations. NRO is closer to 35% in preferred and 65% in equities.

This happens to be close to the allocations of Cohen & Steer’s (CNS) other CEF, the Cohen & Steers Real Estate Opportunities and Income Fund (RLTY). RNP is looking relatively expensive these days as well, trading at a slight premium. However, RLTY is attractively valued, the most attractive currently of the leveraged trio of CNS REIT-focused funds. The other is Cohen & Steers Quality Income Realty Fund (RQI), which I believe is also worth paying attention to as it carries a relatively attractive discount as well.

Ycharts

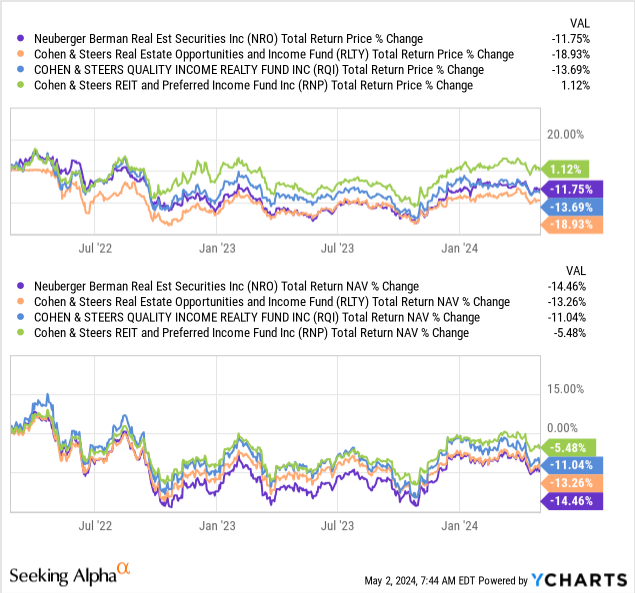

RLTY is a relatively newer fund that launched in early 2022. That was right before the Fed began raising rates aggressively and when REITs went tumbling. That’s why the performance of all of these funds since then has been quite ugly, but on a relative basis, in an admittedly short time frame, RLTY has slightly outperformed NRO. RNP was the best in terms of total NAV returns, and that’s likely a factor in its heavier emphasis on preferreds. While preferreds are also interest rate sensitive, REIT equity positions have proven to be even more rate sensitive.

Ycharts

When removing RLTY and putting the performance up against only the three that have longer histories, we can go back over the last decade to see a performance comparison. When doing that, it really is no competition. Of course, the caveat here is that past performance is not a guarantee of future returns.

Ycharts

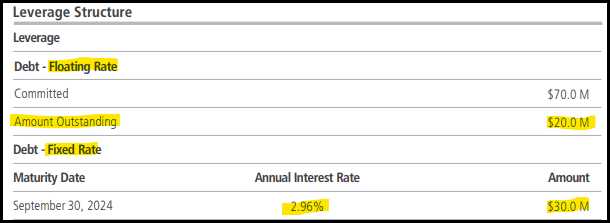

Additionally worth noting here is also that NRO is exposed to less leverage and, therefore, could be considered a bit less risky. Though the fund does carry some leverage, that always means moves are going to be amplified for both up and down moves. The fund also has over half of its latest outstanding leverage on a low fixed annual interest rate, which is beneficial in this higher-rate environment.

NRO Leverage Stats (Neuberger Berman (highlights from author))

The lower leverage also means that if we get a black swan event, this fund is in a better position to utilize the capacity of leverage under its facility. The CNS funds employing higher amounts of leverage are pretty much maxed out. That’s one way that NRO could be in a better position to outperform going forward – of course, assuming we get a sharp drop and NRO takes advantage of such a drop by timing it right.

NRO’s Double-Digit Distribution Yield

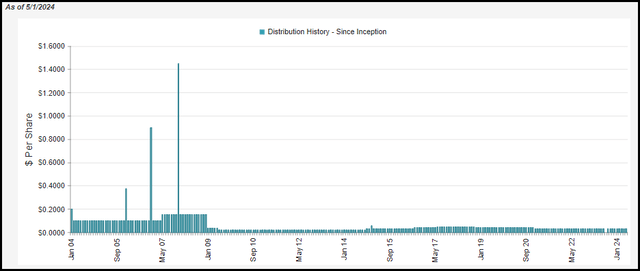

Another area that investors could argue in favor of NRO would be the fund’s distribution. At a nearly 12% distribution yield, that’s probably a draw to the fund for income-focused investors.

NRO Distribution History (CEFConnect)

Unfortunately, that doesn’t always mean a fund is earning that level of payout. In CEFs, there are a number of funds that overpay and end up slowly cutting their distribution over time. NRO is one of those funds that has had to cut its distribution for that reason. RQI and RNP cut their distributions in the Global Financial Crisis as well but have raised them a few times since and held them otherwise steady for a number of years now.

Given NRO’s NAV rate of ~11.5%, plus the fund’s 1.4% operating expense ratio, the fund has to earn around 13% to cover its payout. I had noted previously that it seemed too high, and today, it still remains too high, in my opinion. That doesn’t mean that they will cut, but again, a fund can really pay whatever it would like, but it doesn’t mean that’s what your total returns will be in the end. At this pace, I would continue to expect NAV erosion over a period of time.

Being more optimistic, this fund could benefit from lower rates in the next year or two. In that scenario, as long as the economy is faltering too sharply, the underlying REIT/preferreds could see some significant appreciation. That would definitely help out this fund in a way that supports its currently elevated distribution.

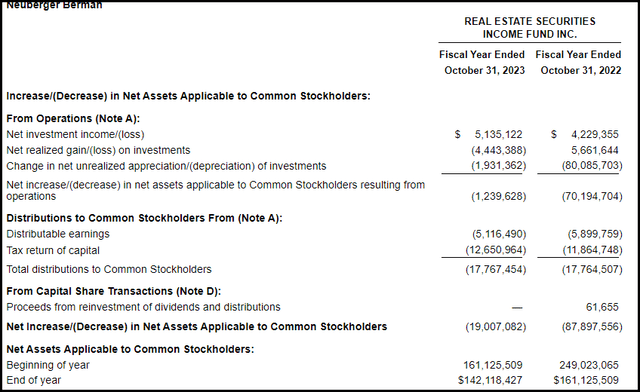

It would also mean that the fund’s borrowings would get a bit cheaper, which would free up more net investment income. The last report showed that NII moved a bit higher as well, to around 29% coverage, up from the ~24% coverage.

NRO Annual Report (Neuberger Berman)

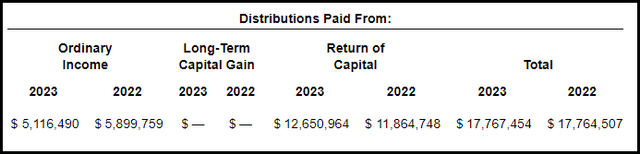

For tax purposes, the fund has seen return of capital as a significant classification in the last two years. However, for 2023, it wouldn’t have been considered destructive ROC as the NAV actually grew that year thanks to some solid performance rebounding from 2022. Still, I suspect we will see destructive ROC going forward in most years unless they cut the distribution or start to perform much better.

NRO Distribution Tax Classification (Neuberger Berman)

NRO’s Portfolio

NRO’s turnover in the last year came in at 7%, so for the most part they had a quiet year in terms of actively managing the portfolio. That could have changed with more recent data, but they only list it as of the 12 months ended October 31, 2023.

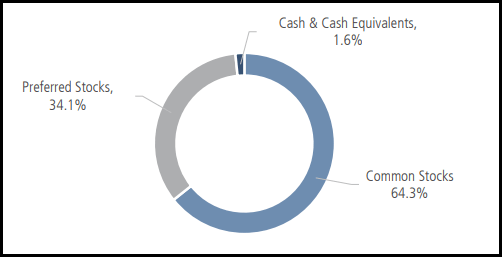

As we noted above, the fund invests primarily in common stocks or equity REITs with a still sizeable sleeve of preferreds. These weightings are consistent with what we saw in our prior update.

NRO Asset Allocation (Neuberger Berman)

Preferreds are one of the areas where the fund can earn some yield, which ultimately helps deliver higher NII for investors. However, they also list that the average yield of the underlying equity REITs is actually quite competitive.

NRO Portfolio Yields (Neuberger Berman)

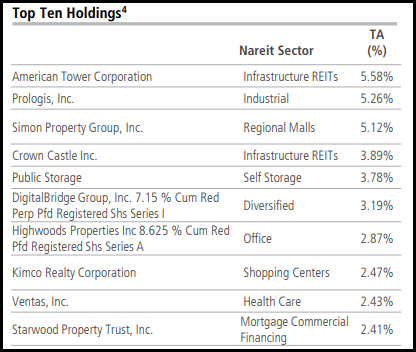

In looking at the top ten holdings, we have a few familiar names that we see regularly in the CNS portfolio. That includes American Tower Corp (AMT) and Prologis (PLD), which tend to be staples of those funds. Simon Property Group (SPG) and Crown Castle (CCI) are also regulars in those peer REIT funds. From there, it gets a bit more mixed, where some of the largest holdings for NRO are preferred positions.

NRO Top Ten Holdings (Neuberger Berman)

NRO listed 81 holdings in total. CNS, on the other hand, tends to be much more diversified when it comes to preferred holdings. None of them generally show up as top holdings, and RLTY, for example, lists 181 total holdings. RQI lists 189 total holdings for some further perspective.

Further, it is worth noting that NRO invests almost purely in real estate/REITs. The preferred sleeve is invested in mostly real estate-related investments. For the CNS funds, that is not primarily the case. Instead, the preferred sleeves for those are overwhelmingly allocated to financial industries such as banking and insurance. That’s one of the reasons why I’ve noted that NRO could be considered more of a “diversifier” fund that could be held in complement with a CNS fund. At the end of the day, though, I’m more valuation-driven when making a decision about where to allocate capital today. That’s why I would still favor a fund like RLTY.

Conclusion

NRO has seen its discount narrow materially since our last update. That has helped the fund’s total returns in the last year but now makes it less likely to outperform going forward. Taking advantage of the narrowed valuation, an attractive alternative to consider for a rotation swap could be RLTY or RQI at this time.

")

")

Q2 2024 Earnings Call Transcript")