")

Investment thesis

As interest rates start their way down, it is safe to assume that over the next six to 12 months, investors’ commitment to cash will decrease, and they will begin looking for alternative investment opportunities that provide low-risk yield. This transition will move them towards higher-risk assets that pay meaningful dividends.

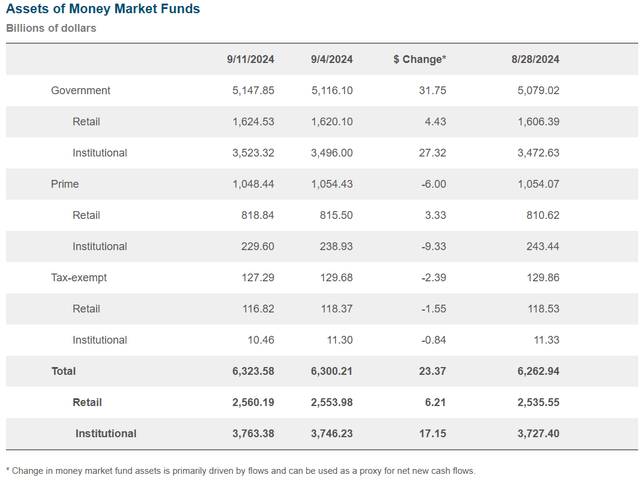

This will be a massive move, as according to the Investment Company Institute, money market funds recently reached US $6.3 trillion. Currently, these funds pay an average seven-day yield of slightly more than 5%.

At the early stages of interest rate cuts, it is difficult to imagine a stampede out of cash; however, over the next six to 12 months, with interest rates going down consistently, the need to diversify will increase dramatically.

Investment Company Institute

Historically, when looking for ways out of cash, investors considered both low-risk equities that pay reliable dividends and debt, however, giving preference to fixed income. Investing in preferred shares of established utilities and infrastructure companies seems like a good combination of both. Preferred shares not only pay low-risk, high-yield dividends fixed for the long term but also may provide capital gains due to further interest rate cuts.

Enbridge remains a low-risk and high-return opportunity

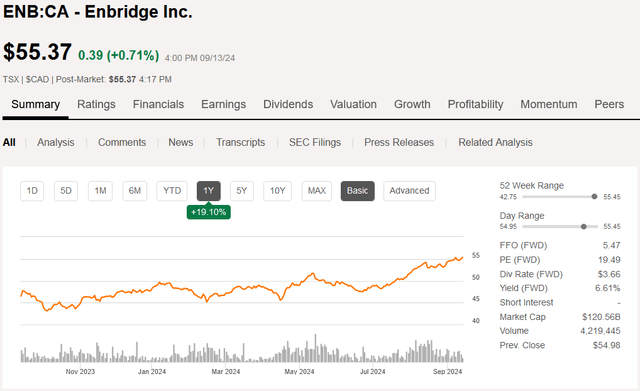

Enbridge will likely benefit from the transition as one of the most popular dividend aristocrats. It ticks all the boxes to be considered a viable alternative for cash investments down the road. However, as I wrote in my previous article, Enbridge: Common Shares Downgraded As Preferreds Offer Better Value, I believe that in the long term, the company’s preferred shares are likely to provide better returns than the commons. In this article, I compare investment opportunities provided by all 21 preferred shares issued by Enbridge.

Seeking Alpha

However, this cannot be done without assessing the overall business and risks related to the company. The risk of investing in Enbridge is low as its business has a geographically diversified asset base. The company’s revenues rely on a high-quality customer base, with 95% of the off-takers having an investment-grade credit rating. A significant part of the sales is built on long-term contracts that are escalated with inflation, providing good visibility for the company’s EBITDA.

In addition to a solid financial outlook, the company has a strong balance sheet that supports Enbridge’s BBB+ rating by S&P and Fitch. Recently, DBRS has upgraded the company’s rating to A, based on the following:

“Planned acquisitions of the US gas utilities provides more stable cash flow generation with lower risk compared to ENB’s existing business risk profile.”

The company’s approach to funding its growth remains relatively conservative. The funding mostly relies on long-term and fixed-rate debt (90% of the debt is fixed). Moreover, according to the company’s management, capital expenditures, as well as mergers and acquisitions, are accretive to shareholders.

Enbridge is one of the most popular infrastructure companies among investors seeking reliable, low-risk dividends. The company has an outstanding track record of paying increasing dividends on its common shares. Over the last 29 years, the dividends’ CAGR reached 9.7%. The company targets a payout ratio for the common shares dividends in the range of 60-70% of the Distributable cash. Preferred shares have significantly better coverage, as their dividends are paid before those of common shares.

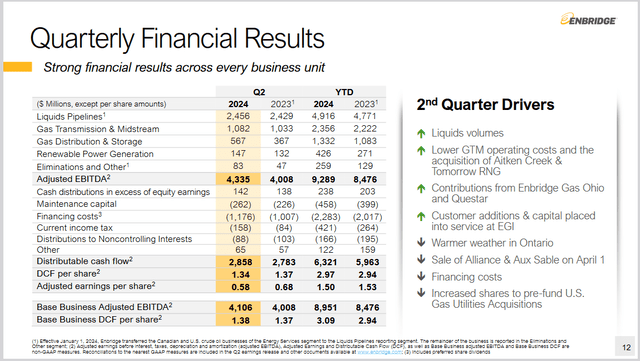

Quarterly results support a long-term positive outlook

Company Q2 presentation

The Q2 2024 operating and financial results align with the expectations, with the Adjusted EBITDA for the quarter reaching $4,335 million (all figures are in CAD unless otherwise stated), approximately an 8.2% increase year-over-year. Even though Distributable cash flow (DCF) increased from $2,783 million in Q2 2023 to $2,858 million this year, the DCF per share went down from $1.37 to $1.34 over the same period. Similarly, adjusted earnings per share decreased from $0.68 in Q2 2023 to $0.58 in Q2 2024. The drop results from the issue of new shares to finance Gas Utilities Acquisition in the US. The deal is expected to strengthen the company’s business and improve dividend coverage for preferred shares, as their number and total dividends remain the same.

Enbridge preferreds: alternatives for cash investors

Enbridge has 21 preferred shares currently listed in Canada and the US. The preferreds offer a significantly higher yield than the commons. Moreover, some of the preferred shares will have their dividend yields reset over the next year, resulting in a major increase. Three out of 21 preferreds are paying dividends in the US dollars. These shares are trading on the Toronto Stock Exchange and are also available in the US on the OTC market. All dividends paid by Enbridge preferreds are eligible dividends:

“Unless otherwise indicated, common and preferred share dividends paid by Enbridge Inc. (NYSE:ENB), either in Cdn or US dollars, will be designated as “eligible dividends” for Canadian income tax purposes except as described below*. An eligible dividend paid to a Canadian resident is entitled to the enhanced dividend credit.”

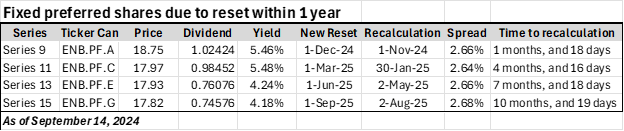

Preferred shares are due to reset within one year

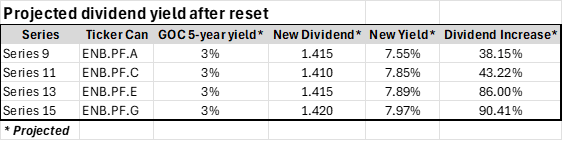

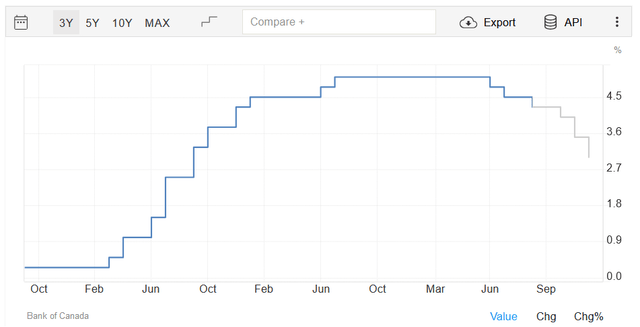

The following Enbridge preferred shares are due to reset within one year. For all of these preferreds, the new yield will be calculated based on the sum of the respective spreads and the yield of five-year Bank of Canada (BOC) bonds at the time of recalculation. The dividends will be fixed for five years from the reset.

Author analysis

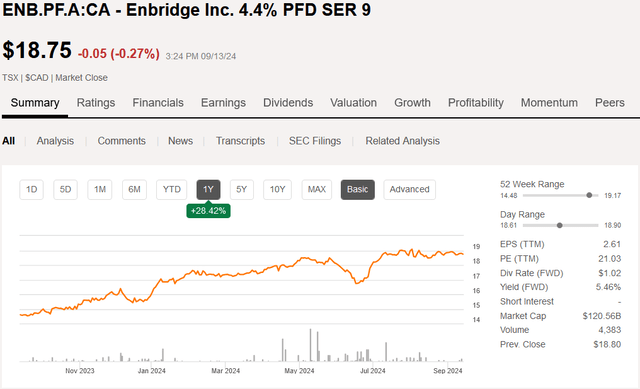

Series 9 (ENB.PF.A:CA) will be reset first, on December 1, 2024, with dividends recalculated 30 days before that — on November 1. Series 15 (ENB.PF.G:CA) will have its dividends recalculated later than others on August 2, 2025.

Seeking Alpha

In the current economic environment, it seems reasonable to assume that the yield for the five-year BOC bonds will remain at 3% in the long run. This assumption results in the following projected dividend increases. Series 13 (ENB.PF.E:CA) and Series 15 (ENB.PF.G:CA) would get the highest dividend hike of 86% and 90.41%, respectively, due to the significant time lag before their resets. The projected post-reset yields for these preferreds are between 7.55% and 7.97%.

Author analysis

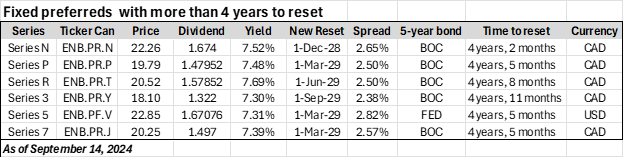

Preferred shares that have their dividends fixed for more than four years

Investors who are interested in long-term fixed dividends may consider the six preferred shares listed in the following table, as their dividends were recently reset. They offer yields exceeding 7% fixed for more than four years. Five out of six preferreds pay dividends in Canadian dollars, and Series 5 (ENB.PF.V:CA) pays dividends in US dollar.

Author analysis

US dollars denominated preferred shares

Author analysis

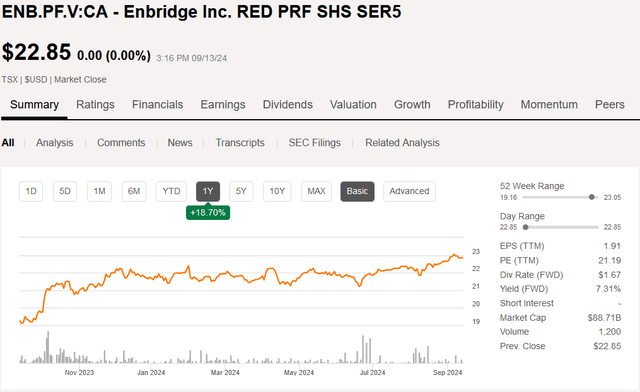

Series L (ENB.PF.U:CA) (OTCPK:EBBNF), Series 1 (ENB.PR.V:CA) (OTC:EBBGF) and Series 5 (ENB.PF.V:CA) (OTCPK:EBGEF) are US dollar denominated and pay dividends in US dollars. As of September 13, closing, the highest yield of 7.31% is offered by Series 5 (ENB.PF.V:CA). These preferred shares were reset on March 1, 2024, and offered the longest time before the next reset (four years and five months). The dividends are reset based on the sum of their spreads and the United States Treasury bond, with a term to maturity of five years. Since October 2023, the price of the preferred shares has increased significantly due to the expectation of interest rate cuts by the FED. The capital appreciation is likely to continue with the US economy slowing.

Seeking Alpha

Floating-rate preferred shares provide an even higher yield

Three out of 21 Enbridge preferreds pay floating dividends that are recalculated every three months, with the dividends based on the sum of their spreads and yield of three-month GOC bonds at the time of recalculation. Even though they offer higher yields than the fixed dividend preferreds (between 7.99% and 9.14%), many investors are cautious about them as the upcoming interest rate cuts will result in lower dividends. However, at least for the next year, those dividends will likely exceed the fixed dividends paid by other preferreds.

At the same time, as I wrote in my previous article, “Northland Power Series 2 Preferred Shares Pays Dividends North Of 10%, And Share Price Is Likely To Go Up” history indicates that the decrease in interest rates is likely to be compensated by capital appreciation. This argument seems to be getting more acceptance as Enbridge announced that investors voted to convert more than 1 million Series 3 fixed dividend preferred shares to Series 4 floating dividend preferreds.

Author analysis

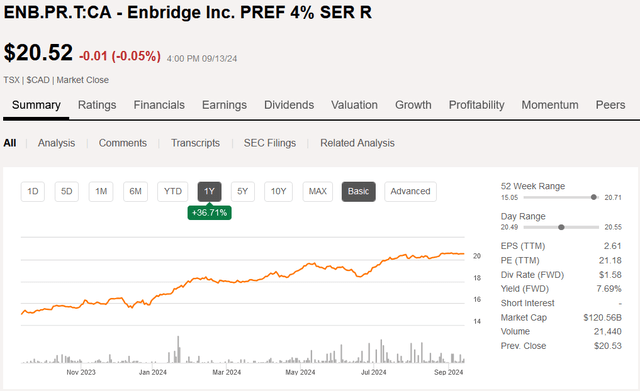

Three fixed dividend preferred shares with the highest yield

The following three preferreds: Series H (ENB.PR.H:CA), Series N (ENB.PR.N:CA) (OTCPK:ENNPF) and Series R (ENB.PR.T:CA) offer a combination of the yield above 7.5% and significant time to reset.

Author analysis Seeking Alpha

The remaining five preferred shares seem less interesting

Five fixed dividend preferred shares in the table below seem less interesting due to lower yields and relatively short (under four years) time to reset.

Author analysis

Risks associated with investment in Enbridge common and preferred shares

The risks related to investments in common and preferred shares of Enbridge include both downside and upside. The typical downside risks are the ones associated with operations and development. They include problems with regulators, economic issues impacting supply demand dynamics, force majeure events as well as overpaying for M&As, unjustified capital expenditures and development of projects with low returns.

Macroeconomic risks include sticky inflation, which could result in a potential increase in interest rates, and an economic recession, which could result in technical selloffs of both preferred and common shares. On the other hand, steady interest rate cuts by the BOC and Fed could result in capital appreciation for both common and preferred shares, as well as capital inflows from investors in the money market.

What to expect from the BOC and Fed

The three interest rate cuts by the Bank of Canada this year and the widely expected first cut in the US by the Federal Reserve this September indicates the beginning of the new monetary policy cycle. The markets expect the banks to continue with the rate cuts into the next year. Currently, the key interest rate in Canada is 4.25%. Trading Economics forecasts three more rate cuts before the middle of next year, with the benchmark interest rate in Canada going down to 3% on June 30, 2025.

Trading Economics

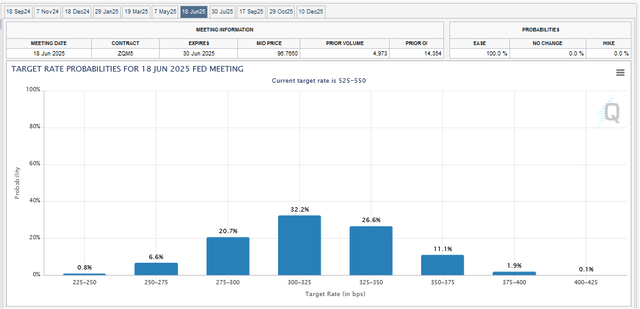

Similarly, in the US, according to the CME Group, the markets expect that by the end of June next year, interest rates will decrease from the current range of 5.25%-5.5% to 3%-3.25%. If the soft landing of the US economy becomes more turbulent, the interest rate cuts may be faster and deeper.

CME Group

Conclusion

The current economic environment is characterized by the interest rate cuts in both Canada and the US and the high concentration of investors in money markets. It seems likely that the future steady decrease in interest rates will result in investors diversifying from cash to other high-yield and relatively low-risk investments over the next six to twelve months. Enbridge’s low-risk and high-dividend preferred and common shares will likely benefit from this transition.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")