Q1 2024 Earnings Call Transcript")

I On The Prize")

Summary

Meta (NASDAQ:META) is the premier social advertising platform, with 3.24Bn Daily Active People using its family of apps. Its Q1 2024 results showed strong financial performance but presented challenges to 3 critical narratives driving the stock. Despite this noise and the near-term headwinds posed by AI investment, we view the long-term growth prospects as intact and compelling, including advertising on Reels, AI services (including introducing new ad formats and products), and business messaging. We maintain our Buy rating.

Earnings Update

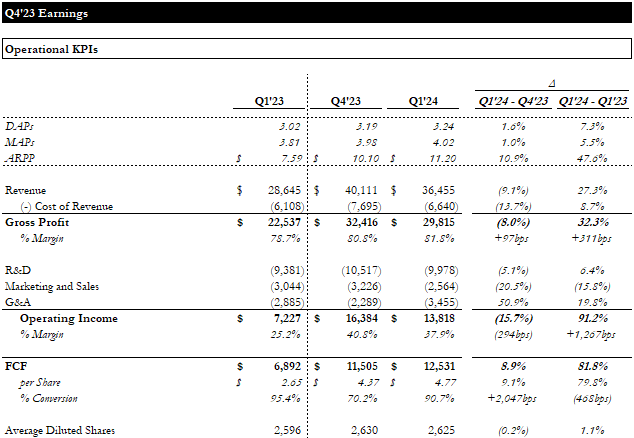

By the numbers, Meta posted a strong quarter. Daily Active People (“DAP”) and Monthly Active People (“MAP”) grew 1.6% and 1.0% QoQ, respectively, with MAPs cracking 4Bn for the first time. Sequential comparisons of the income statement are not very meaningful, given the business’ seasonality. Compared to the comparable period in 2023, revenue grew ~27%, and gross margins expanded ~300bps. R&D and G&A spending were up ~6% and ~20%, respectively, as the Company continues to invest heavily in new projects, including AI (discussed later), though marketing spend declined ~16%. This drove a ~90% increase in operating income (“OI”) with a ~1,300bps margin expansion. FCF per share was up ~80% YoY and ~9% QoQ. Despite repurchasing ~$15Bn of shares, the average diluted share count only declined ~0.2% due to Meta’s extremely generous stock-based compensation.

Earnings Update (EMpyrean; META)

Despite these positive results, the shares opened down ~14% and are currently down ~10% from the pre-release price. The market’s negative reaction to the report centers around data points and management commentary that challenged 3 key narratives for the stock.

Firstly, the market was looking for AI to help solve the negative impact of Apple’s App Tracking Transparency (“ATT”) related changes, leaving Meta well positioned to benefit from elevated revenue growth by taking share in the digital advertising market. Meta is certainly better positioned in the post-ATT world; however, with>50% of the non-Search digital ad market, AI-related share gains will likely only have a modest impact from here. Furthermore, the benefit of AI to ad growth may have been overestimated relative to just ramping ad volumes, at least in the short term. The lack of material revenue upside provided in the Company’s Q1 & Q2 guidance supported this view, and it is likely that revenue growth will decelerate into the mid-teens in the second half of the year.

Secondly, the narrative was that AI would unlock additional revenue streams by offering users new experiences. While Meta has made impressive progress with its AI models, and there will certainly be incremental monetization opportunities over time, Zuckerberg emphasized that significant monetization of its AI was still a few years away. Against the backdrop of the Company’s need to enter a new heavy investment cycle, the market took this poorly. In fairness, Zuckerberg did note some of the early success of its AI initiatives, which we view as highly promising:

Right now, about 30% of the posts on Facebook feed are delivered by our AI recommendation system. That’s up 2x over the last couple of years and for the first time ever, more than 50% of the content that people see on Instagram is now AI recommended.

AI has also been a huge part of how we create value for advertisers by showing people more relevant ads. And if you look at our two end-to-end AI powered tools, Advantage+ shopping and Advantage+ app campaigns, revenue flowing through those has more than doubled since last year. (Meta Q1 Conference Call)

Lastly, was the narrative around the company’s renewed cost discipline. The quarter showed that opex continues to be much more tightly managed than historically. However, Meta raised the low end of its 2024 opex guide to $96-99Bn from $94-99Bn and raised its capex guidance for the second quarter in a row to $35-40Bn from $30-37Bn to support the AI build-out. While this risks losing the Company’s hard-earned investor trust, it highlights just how much potential Meta sees in its AI initiatives.

Valuation

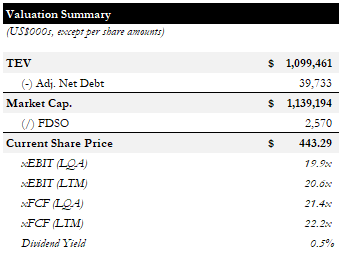

Following the post-earnings sell-off, Meta is trading for ~21x LTM EBIT and ~22x LTM FCF.

Valuation Summary (Empyrean)

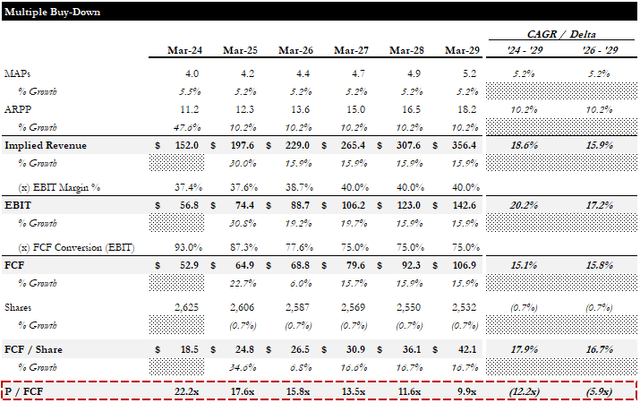

Despite the near-term pressures posed by the impending AI investment cycle, we are still relatively bullish on Meta’s long-term prospects. Below, we outline an illustrative multiple buy-down under what we believe is a reasonable set of assumptions.

Multiple Buy-Down (Empyrean)

We believe the main risks and catalysts are largely unchanged from our previous report:

China-Based Advertisers

China-based advertisers accounted for ~10% of advertising revenue in ’23, accounting for ~5% of overall growth. It was well known that China-based advertisers accounted for a large portion of Meta’s revenue, but the extent to which Meta relied on them was surprising. The largest verticals these advertisers were active in were Online Commerce & Gaming. This could increase political pressure on Meta and threaten topline growth if geopolitical tensions rise further.

Higher CapEx Requirements

Meta raised its ’24 capex guide due to its increasing focus on AI. With a goal of building the most popular and advanced AI products and services, it raised the high-end of its ’24 capex guidance by ~$2Bn and now expects to spend between ~$30-37Bn, with which it expects to acquire ~350k of Nvidia’s H100s and ultimately have ~600K equivalent H100s of compute by the end of the year ’24.

Regulatory Headwinds

Regulatory headwinds remain a significant concern, with the FTC seeking to modify an existing consent order that could have an adverse impact on future operations.

“In 2019, the FTC accused Meta of misleading parents about privacy controls regarding the Messenger Kids app and other issues. Furthermore, it also imposed a $5 billion fine on the company while banning the monetization of data of minors.

In May 2023, The FTC proposed changes to the privacy order, alleging that Meta had violated the 2019 order. The FTC has now proposed a blanket prohibition order on monetizing youth data.

As per the changes, Meta will not be able to profit from the data of minors it collects, and this would even include interactions with its VR devices. The amended privacy order will also limit how Meta can use biometric recognition and make additional protections mandatory for users under 18.” (Spice Works.)

(Empyrean)

With the cat out of the bag as far as the risk of higher capex, we see the reliance on Chinese advertisers presenting a risk that may not be priced in, especially with US elections on the horizon.

Clearly, AI could (and we believe it will likely be) a major catalyst over time as the Company begins to monetize it. We would also add the potential TikTok ban as another potential windfall for Meta.

Conclusion

Despite investors’ disappointment in Meta’s Q1 2024 results, we believe that the Company’s current valuation offers a reasonably attractive entry point considering its long-term growth prospects. Heavy investment in AI and Reality Labs will likely weigh on the shares in the short term, so we would consider writing covered calls to improve our basis.

")