A “Buy” Rating for McEwen Mining

This analysis suggests a “Buy” recommendation for shares of McEwen Mining (NYSE:MUX) (TSX:MUX:CA) as, thanks to improved precious metals assets performance in Nevada and good prospects for the mineral projects in Ontario and Argentina, this stock is considered to be well-anchored in the expected uptrend in the gold and silver price cycle amid friendly conditions for the metals with robust demand for hedging strategies and bets on the rate cut by the Federal Reserve (or “Fed”).

President Javier Milei’s legislative package, recently approved by Parliament, has created a much more proactive framework for corporate activities in Argentina. The package aims to reduce bureaucracy in the Argentine economy and give significantly more space to private initiatives, especially the mining industry, one of the pillars of the country’s economy.

Regarding “The Outlook for Gold and Silver,” an entire section is devoted to this topic later in this analysis.

From the Previous Buy Rating: What Happened

This article maintains the same rating of “Buy” as the previous article when McEwen shares were expected to reach significantly higher prices. Although not better positioned than its direct competitors in terms of production and costs, the strong bullish sentiment towards gold and silver was seen as an effective upward driver for share prices of McEwen.

Since the last buy recommendation on March 11, 2024, the market price of McEwen shares has increased by 11.01%, while the US stock market benchmarked by the S&P 500 stock index has increased by 7.10%.

While prior to the subsequent rally the stock did not offer a temporary “healthy” pullback for a bigger return given how tied to the metal’s upside its share price was, investors were still very pleased with the stock flying to record highs between late April and late May 2024 despite starting from an overbought level the recent analysis showed with prices above MA Ribbon and RSI at 70.

Shares in McEwen were helped sharply to the top by the “metal’s third straight monthly gain” in late April, overshadowed after a few weeks by a “new record high” among investors looking for gold (and silver) as a portfolio hedge and rising interest rate cut hopes following encouraging US inflation numbers.

In the wake of the sharp tailwind from precious metals prices, Q1 2024 operating and financial results may have added some extra positivity to McEwen Mining stock’s momentum due to the following:

- 100% interest in the gold/silver open pit “Gold Bar Mine” in Nevada (46 km northwest of Eureka) and 49% interest in the gold/silver underground San Jose mine (48 km east of Perito Moreo, Argentina) performed well.

McEwen Mining Inc. indirectly owns San José through Minera Santa Cruz S.A., a joint venture that directly owns 100% of San José, and the mine’s operator is the majority shareholder of the joint venture, Hochschild Mining plc (OTCQX:HCHDF), which owns the remaining 51% of the joint venture.

- In addition, President Milei’s liberal political leadership in Argentina makes it easier to be optimistic about the prospects for San Jose and the success of the 47.7% indirect interest in the Los Azules project for future copper/gold/silver production 164 km northwest of San Juan, Argentina.

McEwen Copper Inc. owns a 100% direct interest in the Los Azules copper project and currently has approximately 30.94 million shares outstanding. Excluding the impact of the raising of US$70 million through a private placement of up to ~2.33 million shares for subsidiary McEwen Copper to advance the Los Azules Copper Project, with respect to beneficial ownership of Los Azules, McEwen Mining owns 47.7% of McEwen Copper, Stellantis N.V. (STLA) 19.4%, Nuton 14.5%, Rob McEwen (Chairman and majority owner of McEwen Mining) 12.9%, Victor Smogon Group 3.2% and other shareholders 2.3%.

Downward Long-Term Trend Disrupted by Bullish Precious Metal

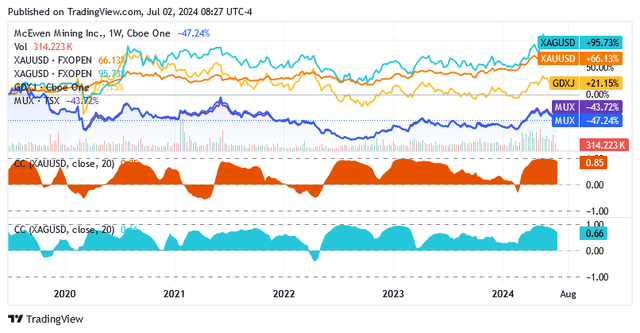

By outperforming its direct rivals on the stock market, McEwen stock has now reversed a trend that had underperformed the VanEck Junior Gold Miners ETF (GDXJ) or its industry’s benchmark index over the long term, reinforcing the thesis of previous analysis that this stock is suitable for capitalize on strong short-term movements in the gold price.

Despite the positive correlation with the Gold Spot Price or XAUUSD:CUR and Silver Spot Price or XAGUSD:CUR, McEwen Mining shares on the NYSE under the symbol MUX and on the Toronto Stock Exchange under the symbol MUX:CA over the past 5 years have shown a significant decrease in value while GDXJ increased 21.15%. The positive correlation, which means that McEwen stocks and gold or silver tend to move in the same direction on average, is graphically represented by dark yellow and light blue area curves that have consistently traded above zero for the past 5 years. The positive correlation means that when stocks are bullish, gold or silver is most likely also bullish, and when stocks are bearish, the metal is most likely also bearish, regardless of returns, which can even be vastly different between the assets.

Source: Seeking Alpha

But now the last 5-year trend has been shocked:

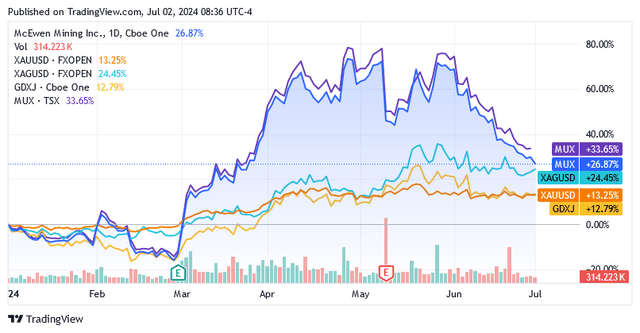

While driven by the sustained rise in the gold price (up 13.25% YTD) or silver price (up 24.45% YTD) coupled with the good results and rosy growth prospects outlined in the Q1-2024 report, McEwen stocks continued to perform significantly better than GDXJ industry as anticipated in the last analysis on March 11, 2024. Although the Ontario mine underperformed, higher consolidated production combined with rising metal prices resulted in a 36.4% year-over-year increase in gross profit to $6 million and a 117% increase in adjusted EBITDA to $6.3 million. Also, a lower consolidated net loss of $20.4 million in the first quarter, primarily due to the investment in McEwen Copper, compared to a net loss of $43.1 million in the first quarter of 2023. The market was pleased with the Q1-2024 profit results from McEwen Mining, and the earnings are acting as a driving force behind share prices in the markets.

Source: Seeking Alpha

McEwen Mining in Q1-2024 and the Boost to its Growth Plans

As for the assets already producing the metals: in addition to 100% in the “Gold Bar Mine” in Nevada and 49% in the underground “San Jose mine” in Argentina, with geolocation better detailed earlier, McEwen Mining has 100% ownership of the gold and silver underground Fox Complex located 65 km east of Timmins, Ontario, Canada.

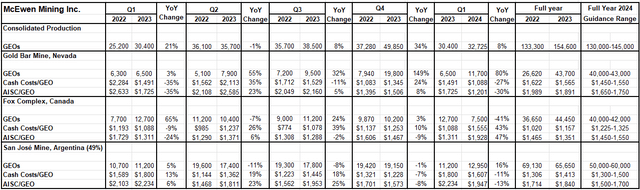

For the first three months of 2024, these mines produced 32,725 gold equivalent ounces (or “GEOs”) on a consolidated basis, representing 8% year-over-year growth, but on a quarterly basis, it was below the full-year 2024 midpoint guidance range of 130,000 to 145,000 GEOs.

Source: McEwen Mining Operating and Financial Reports

Continuing the Q1-2024 trend, Gold Bar Mine is on track to surpass last year when it produced 43,700 GEOs at an AISC of $1,891/oz and also its own guidance of 40,000 to 43,000 GEOs at $1,650 -1,750 AISC/GEO for the whole year of 2024. Gold Bar produced 11,716 GEOs, a more than 80% increase over the previous year quarter. However, production was affected by severe flooding the year before and AISC/oz of $1,201 in Q1-2024 could rise in the second half of 2024 as the company announced operations to move to mining areas with higher strip conditions.

The Fox Complex was impacted by lower-than-expected mining and stockpile grades, resulting in production of 7,486 GEOs in Q1-2024, below plan and more than 40% lower than the prior year quarter. AISC per GEO of $1,928 was also impacted, increasing 47% year-on-year.

The start of 2024 has not been particularly promising for McEwen Mining’s operations in Ontario, but the issues that led to a deterioration in performance in the first quarter of 2024 are turning positive again. The break of a positive trend makes the company very optimistic about Fox Complex’s prospects despite a very weak first quarter of 2024. The full year 2024 production and cost guidance of 40,000 to 42,000 GEOs at $1,450-1,550 AISC/oz is confirmed as the company is confident it can meet the target, which at this point implies growth from the first quarter of 2024 by calculating the quarterly figures on an annual basis. Thus, the company has priced a 2-tranche public financing as it intends to collect the estimated net proceedings of $20.9 million and set aside for drilling and underground infrastructure development will unlock the production growth that should be standard equipment at the Fox Complex.

In San José, production of 12,950 GEOs increased 15% year-over-year in the first quarter of 2024 due to an improvement in the average grade of the mining material processed, causing AISC/GEO to decline 13% year-over-year to $1,947. In line with higher, continued improvement in metal grades as production approaches the midpoint of the full-year 2024 guidance range of 50,000 to 60,000 GEOs, AISC/GEO will probably be lower and in the $1,500 to $1,700 range.

The new environmental outlook for Argentine mining and exploration under President Milei’s administration and his plans to ease exchange controls and enact regulatory reforms, should benefit the Los Azules and San José joint venture mine going forward.

The Los Azules project is a porphyry copper deposit that remains largely undeveloped. Over the past three years, McEwen Copper has reported investing over $230 million in exploration. Preliminary results from 227,000 feet (69,200 meters) of drilling completed so far during the 2023-2024 drilling campaign provide results consistent with the June 2023 Preliminary Economic Assessment (or June 2023 PEA), while metallurgical testing supports an average recovery of 76% using conventional technology, opening up the possibility of a project that could be even more valuable. Based on copper indicated resources of 10.9 billion pounds grading 0.40% Cu and additional copper inferred resources of 26.7 billion pounds grading 0.31% Cu as of PEA June 2023, the Los Azules project has a $2.7 billion after tax NPV8% but the metallurgical tests could raise it further by approx. US$262 million.

The resources are indicated and require further studies to upgrade to a higher mineral reserve category. Only this resource category allows a reliable assessment of the economic viability of the project. The above-mentioned $70 million non-brokered private placement financing from McEwen Mining will be used to accelerate the completion of a feasibility study for the Los Azules Copper Project. This should be available in early 2025 and since interest rates will have fallen by then, it should be much easier for the Los Azules copper project to raise the necessary funds, giving the entire project a boost.

San Jose aims to continue producing metals beyond 2028: Underground exploration near the San Jose mine now offers great potential to expand a mineralized area from the current 80 meters to a target of over 700 meters. Exploration activities indicate that there is potential for further exploitation of this deposit, not only downslope, but also in shallower areas where high mineral concentrations are expected.

The Outlook for Gold and Silver Prices

In times of heightened risk perception for economic growth and increasing global uncertainty, gold and, to a lesser extent, silver investments are used to hedge portfolios against potential negative value impacts. The fact that the Federal Reserve is keeping interest rates high between 5.25 and 5.50 percent on federal funds signals distrust in lending to the economy, as consumers and producers are not seen to provide sufficient solvency guarantees if they are now given hope of recovery. But investors have started to focus more on precious metals than US Treasuries as the latter’s fixed-income asset class, with the prospect of lower returns, tends to cool in attractiveness, leaving more room for zero-income paying gold and silver. Because after 11 rate hikes from March 2022 to July 2023 to combat galloping inflation and no rate cut since then, market participants expect the Fed to reverse rates as inflation fell sharply from 9.1% in June 2022 to the current 3.3%. So, when hopes for the start of Fed rate cuts grow stronger, a rise in per-ounce prices usually follows.

The uncertainty scenario is also currently driving the demand for gold and silver in portfolio hedges as investors fear the impact on their assets of possible disruptions in the economy due to the geopolitical tensions with conflicts in Ukraine and issues in the Middle East at the center of global attention. While the jumps caused by expectations of an eventual rate cut heating up have short-term favorable effects on gold and silver prices, robust demand as a hedge against risk and uncertainty is more geared to strengthen the uptrend in the long term, creating a solid support structure below the prices. A little later they were identified with China’s and other overseas bankers, but central bank buying is an activity that has been going on since early 2024, providing much support for the uptrend in the long run. Rather than inflation falling dramatically as described earlier, the potential recession from the Fed’s hawkish rate policy led China to finance gold purchases through the sale of US dollar reserves to the extent that US investors also picked up the signal to hedge through the yellow metal against threats to the value of their economy. The previously negative sentiment in the West towards the yellow metal began to improve when Robert Crayfourd and Keith Watson, co-managers of the CQS Natural Resources Growth & Income Fund, signaled at the end of May that the significant increase in the use of the ETF as an indicator of investments in physical metals would give prices another boost.

At the end of May 2024, the analysts’ team at UBS Group AG (UBS) Wealth Management welcomed the central bankers’ purchases as “strategies that generate returns in gold” – as a countermeasure against the risk of an economic slowdown burdened by inflation and expensive consumer and investment loans, as well as “healthy” hedging demand against the geopolitical risk factor. Driven by a vision of good momentum for such gold demand, the UBS team of analysts led by Solita Marcelli had raised their year-end gold price forecast to $2,600/oz, according to Marketwatch.

Recently, other major US banks have been busy predicting the gold price in the upcoming period, with Citigroup Inc. (C), targeting $3,000/oz in the next 6 to 18 months, while a more limited but still generous rise to $2,700/oz by the end of the year The Goldman Sachs Group, Inc. (GS) has issued at the end of last month.

Currently, the Gold Spot Price (XAUUSD:CUR) is trading at $2,330.32/oz.

As for the Silver Spot Price (XAGUSD:CUR), gold’s less shiny cousin, which is trading at $29.36/oz as of this writing, Michale DiRienzo, president and CEO of The Silver Institute, which regularly publishes statistics on the demand, supply and prices of the gray metal, last month pointed out that silver prices are poised to follow gold in its ample room to move forward.

In addition to hedging strategies, silver also has “some very practical properties” that are far less present in gold. These will help ensure that the grey metal does not lose touch if the gold price continues to rise. Silver is also used in industrial processes, such as in the manufacture of solar cells. Plus, an ounce of silver is relatively cheaper than gold, which acts as a buying incentive. Based on current market prices, it takes about 79 ounces of silver to buy one ounce of gold, compared to the “20-year average of about 68.”

“The second-biggest market deficit in more than 20 years,” expected this year by The Silver Institute, as a bright future for silver in the “green energy transition” envisioned by President Michale DiRienzo will exacerbate the problem of lower ore grades globally yielding insufficient supply of ounces will provide a robust upward pressure on the price of the gray metal.

Analyst Michael Widmer of fellow US banking major Bank of America Corporation (BAC) said last month that his view now remains bullish for the second half of 2024 and into 2025, expecting silver to average $35/oz in 2026.

The Share Price: The Stock Is a Buy, but a Lower Price Is Possible Under Current Conditions

The growth prospects for the metals are positive, the Nevada deposit is performing well, the Ontario deposit is benefiting from improving grades and the Argentina deposit is also on track to deliver more ounces at lower costs, this analysis suggests buying McEwen shares.

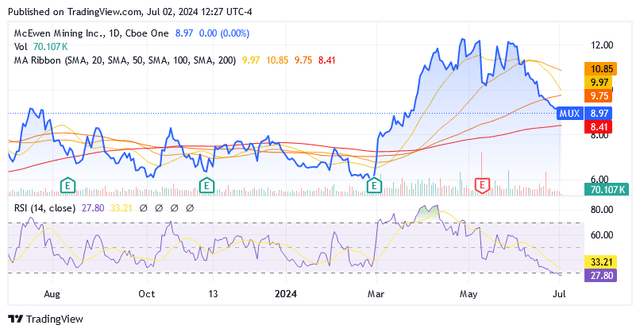

Shares were trading at $8.97 apiece for a market cap of $ 457.23 million under the MUX symbol on the NYSE market. Shares were trading around the middle point of the 52 Week Range of $5.92 to $12.50, and almost completely underneath any line of the MA Ribbon. So, these indicators suggest that the share price is currently low compared to recent trends, while the outlook remains very promising also due to the very favorable mining policies that can now reasonably be expected given the new economic climate under President Milei in Argentina.

Source: Seeking Alpha

The 14-day Relative Strength Indicator of 27.80 suggests that the shares are now back at oversold levels as the last month has not been particularly exciting for the price of the precious metal as we have been spoiled by very significant gains in the previous months. This is most likely due to comments from Federal Reserve policymakers who recently showed reluctance to cut interest rates in September and are now predicting not even two but only one rate cut before the end of the year – and perhaps not even this year. If we add that there are even voices that do not rule out a further interest rate hike, then these views have put pressure on the price of precious metals. Not only do these – unlike US Treasuries – offer no income, but they also suffer from the fact that the strengthening of the US dollar due to Fed chiefs repeated “higher for longer” prophecies has made buying gold significantly less favorable for investors in non-US dollar currencies economies. A slowdown in investment demand for gold (but also silver, which is said to be “poor man’s gold”) has had depressing effects on McEwen shares through moderating precious metal prices.

Essentially, it’s down to the robust labor market, and last week there was another sign of that: the U.S. jobless claims of 233,000 in the period ending June 22 fell for the second week in a row. This forces the Fed to hold back from convincing itself that it is time to cut interest rates. The still very tight conditions in the labor market are blamed for the basis of sticky inflation, which is very reluctant to return to the medium-term target of interest rate of 2%. And then it could be that after this summer vacation, when people tend to spend more, households could complicate the plan of the Fed, which is trying to look as clearly as possible at the inflation issue before it rewinds the monetary policy coil. And so precious metals may still face headwinds, and the impact will still have ramifications for McEwen stock on the NYSE market.

The rating is Buy, but perhaps investors will wait and see how the sentiment around the Fed’s first rate cut, now still expected in September, will be when we get there.

The same reasoning applies to shares of McEwen Mining on the Toronto Stock Exchange under the symbol MUX:CA: At the time of writing, these shares were trading at CA$12.41 a share, with a market capitalization of CA$628.20 million.

Source: Seeking Alpha

Shares are trading nearly below almost each line of the MA Ribbon and near the midpoint of the 52-week range of CA$8.05 to CA$17.08 per share. The 14-day RSI of 28.35 suggests oversold levels but does not rule out lower valuations as further headwinds could lie ahead.

Low Liquid Stock in Toronto Stock Exchange

Investors are certainly aware of the disadvantages usually associated with the low daily trading volumes, as McEwen Mining shares on the Toronto Stock Exchange seem to be characterized: over the past 3 months, an average of 42,207 shares have been traded on the TSX (scroll down to the Trading Data section on this Seeking Alpha page).

Of the total 50.97 million shares outstanding, 41.32 million shares are in the free float, freely tradable on the open market of the Canadian exchange, and institutions own 31.08% of the free float.

Investors must therefore remember that it can be very difficult to bring an oversized position up to the desired volume if circumstances suddenly demand it.

Conclusion

This analysis suggests a “Buy” recommendation for McEwen shares as their price should be driven by positive forces, which essentially consist of continued optimistic precious metal prices and improved business prospects.

Silver and gold will benefit as investors turn to hedge properties amid risky economic scenarios and an uncertain global outlook. The company’s production and costs have performed well in Nevada, and now they should also be accompanied by improvements in Ontario and Argentina, where McEwen Mining’s growth projects welcome President Javier Milei’s new political economy to deregulate and give more space to private initiatives also to foreign investors.

Since inflation, until it convinces in its downward adjustment, may still influence Fed policymakers holding back from implementing the first rate cut, a sustained “higher-for-longer” stance on interest rates could result in US Treasuries paying income in the form of a predetermined interest rate being preferred to zero-income yielding gold and silver. Catching shares of McEwen on this short-term dip in bullish sentiment in the gold and silver spot markets could make buying this stock a bigger opportunity than today given the bright outlook.

")