")

Matador Resources (NYSE:MTDR) is a mostly Delaware Basin focused company that has been growing production rapidly through a combination of development and acquisitions. It reported strong Q1 2024 results and now expects its full-year production to end up at the high-end of its guidance.

Matador’s balance sheet remains healthy, as indicated by its ability to issue 2032 notes at a 6.5% interest rate recently. I also project Matador to generate $705 million in 2024 free cash flow at current strip prices before dividends or spending on acquisitions.

My estimate for Matador’s value is $76 per share based on my long-term commodity prices of $75 WTI oil and $3.75 NYMEX gas.

Notes On Matador

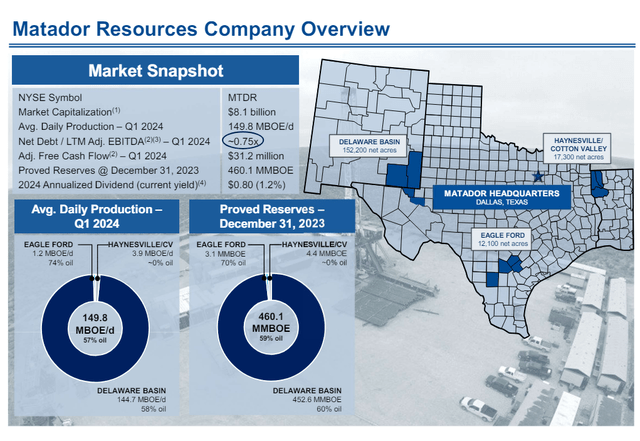

Around 97% of Matador’s production and 98% of its proved reserves are in the Delaware Basin. It also has minor positions in the Eagle Ford and Haynesville Shale.

Matador’s Overview (Matador Q1 2024 Presentation)

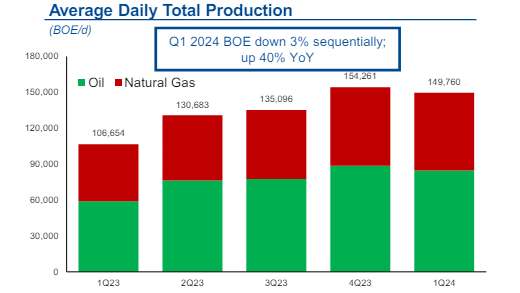

Matador’s Q1 2024 production was up 40% year-over-year compared to Q1 2023. I estimate that a bit over 60% of that growth was from acquisitions (primarily its Advance acquisition) while the remainder of that growth was from the development of its assets.

Matador’s Production (Matador Q1 2024 Presentation)

Matador’s total production in Q1 2024 exceeded its expectations by 3%, while its oil production exceeded expectations by 2%. This (combined with an acquisition) allowed Matador to announce that it expected to reach the high-end of its production guidance for 2024. It also noted that Q1 2024 capex was lower than expected.

2024 Outlook

At the high-end of its production guidance, Matador would average around 159,000 BOEPD during the year, including 95,000 barrels per day in oil production (a 60% oil cut). This would be a 3% increase in total production and a 7% increase in oil production from Q4 2023 levels, although Matador’s recent acquisitions (since December 2023) appear to add a couple percent to its production.

At current 2024 strip prices (including $78 WTI oil and $2.35 NYMEX gas), Matador is projected to generate $3.142 billion in oil and gas revenues. Matador reports production on a two-stream basis, so it is likely to realize above NYMEX for its natural gas. Matador realized $0.86 above NYMEX for its natural gas in Q1 2024, but expects negative $0.50 to positive $0.50 versus NYMEX in Q2 2024 due to weaker Waha pricing.

Matador may add another $130 million in third-party midstream revenues along with $25 million in purchased gas revenues (net of cost).

Matador’s only hedges for 2024 involves Waha basis swaps covering around 8% of its natural gas production at negative $0.59 to Henry Hub. These hedges currently have around $3 million in positive value for 2024.

|

Type |

Barrels/Mcf |

$ Per Barrel/Mcf |

$ Million |

|

Oil |

34,675,000 |

$78.50 |

$2,722 |

|

Natural Gas |

140,160,000 |

$3.00 |

$420 |

|

Third-Party Midstream Revenues |

$130 |

||

|

Net Purchased Gas |

$25 |

||

|

Hedge Value |

$3 |

||

|

Total |

$3,300 |

Matador expects to have around $1.425 billion in 2024 capital expenditures. This includes roughly $225 million in midstream capex.

|

Expenses |

$ Million |

|

Production Taxes, Transportation, And Processing |

$334 |

|

Lease Operating Expense |

$319 |

|

Plant And Other Midstream Services Operating |

$157 |

|

Cash G&A |

$120 |

|

Interest |

$140 |

|

Capital Expenditures |

$1,425 |

|

Cash Taxes |

$100 |

|

Total Expenditures |

$2,595 |

Thus on a consolidated basis, Matador is projected to generate $705 million in free cash flow in 2024 at current strip prices. This doesn’t include the impact of acquisitions and Matador has already made a $155 million acquisition in Q1 2024.

Matador is also paying out around $100 million per year in dividends with its current $0.20 per share quarterly dividend.

Notes On Debt

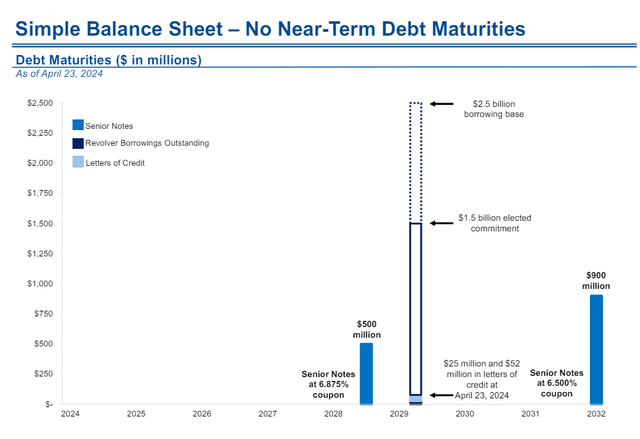

Matador currently (as of April 2024) has $1.4 billion in outstanding notes and $25 million in credit facility debt. Matador’s next debt maturity is its $500 million in 6.875% unsecured notes due 2028.

Matador’s Debt Maturities (Matador Q1 2024 Presentation)

Matador recently issued $900 million in 6.5% unsecured notes due 2032. It used part of the proceeds to redeem its $699.2 million in 5.875% unsecured notes due 2026, while paying down most of its credit facility debt with the remainder of the proceeds.

These transactions took care of Matador’s nearest-term debt maturity. The new notes have a slightly higher interest rate, but a 6.5% interest rate for 8-year notes is still good in the current environment.

At last report, San Mateo Midstream also had $495 million in credit facility debt outstanding. San Mateo is included in Matador’s consolidated results since Matador owns 51% of it.

Notes On Valuation

As noted before, Matador recently issued unsecured notes due 2032 at an interest rate of 6.5%. Thus, I believe that a free cash flow yield of around 10% (before the impact of cash income taxes) would be appropriate for Matador’s valuation. This would translate into a free cash flow yield of near 8% if Matador was a full payer of cash income taxes, which is around 1% to 2% more than its bond interest rate.

I estimate that Matador could generate around $950 million in free cash flow (before cash income taxes) while holding production flat to 2024 exit rate levels. This is based on my long-term commodity prices of $75 WTI oil and $3.75 NYMEX gas and results in an estimated value of approximately $76 per share for Matador.

Conclusion

Matador has been rapidly growing production through a combination of acquisitions and development on its existing assets. It is now expected to end 2024 with near 100,000 barrels per day in oil production.

Matador’s balance sheet looks healthy despite the spending on growth and acquisitions. It has no debt maturities until 2028 now after redeeming its 2026 notes and was also recently able to issue notes at a 6.5% interest rate.

I estimate that Matador is worth $76 per share based on my long-term commodity prices of $75 WTI oil and $3.75 NYMEX gas.

")