")

Investment Thesis

M/I Homes (MHO) is a cheaply valued company with a solid financial foundation and a proven track record of growth. Its customer-centric business offers sustainable housing that is growing in demand. Therefore, it is an excellent candidate to buy and hold for the long term.

The House Of The Future, Sustainable And Eco-Friendly

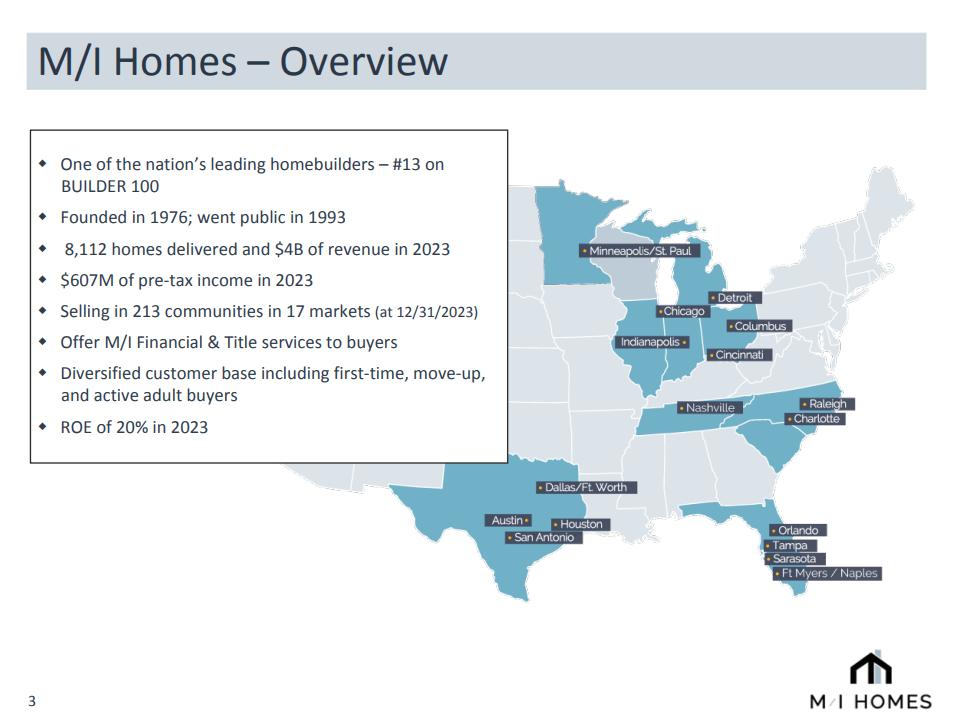

MHO is one of the largest homebuilders in the U.S., ranking #13 in BUILDER 100. The company’s houses are efficient in water and electricity use, aim for sustainability, and claim some of the industry’s best warranty packages.

Their financial services provide mortgages to MHO homebuyers and round up the home-building business side.

They offer a service that guides customers through all the construction process steps, with an app that will alert them of every critical move on the way. MHO appears to be focusing on adding high value through a comprehensive experience, where the customers might not feel as “on their own” as with a more traditional construction company.

M/I Homes Website

MHO has a concentrated business distribution, primarily focusing on the Midwest and South. This adds some risk, as the lack of geographical diversification could put the company in a tight spot if its primary markets dry up.

M/I Homes, Inc. Investor presentation February 2024

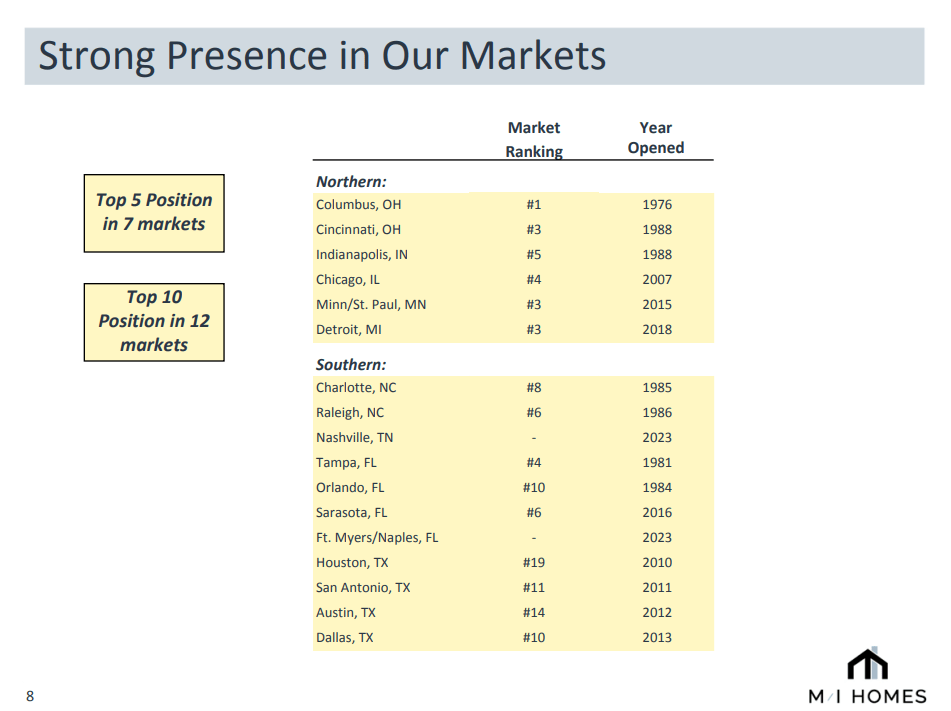

MHO has a strong presence in several markets and ranks high in states like Ohio, Minnesota, and North Carolina. However, it is middle-of-the-road in Florida and lagging in Texas. This is understandable as their entry into Texas was relatively new compared with the other markets.

Expansion into other markets and improved standing in the present markets are two important things to look for, and MHO could really use them, as it seems rather locked in its current areas right now.

Income In 2023 And Before

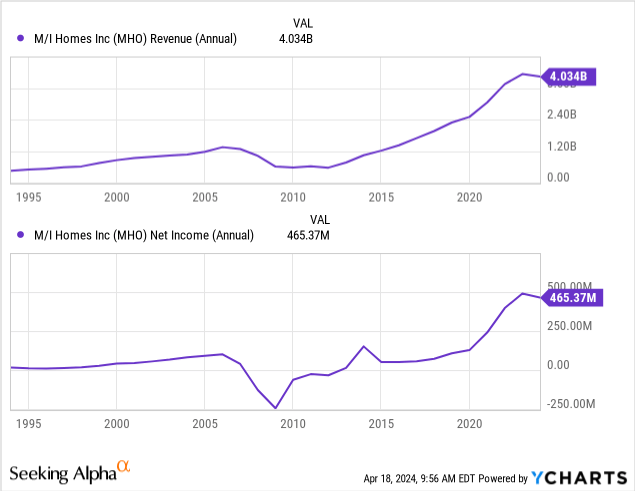

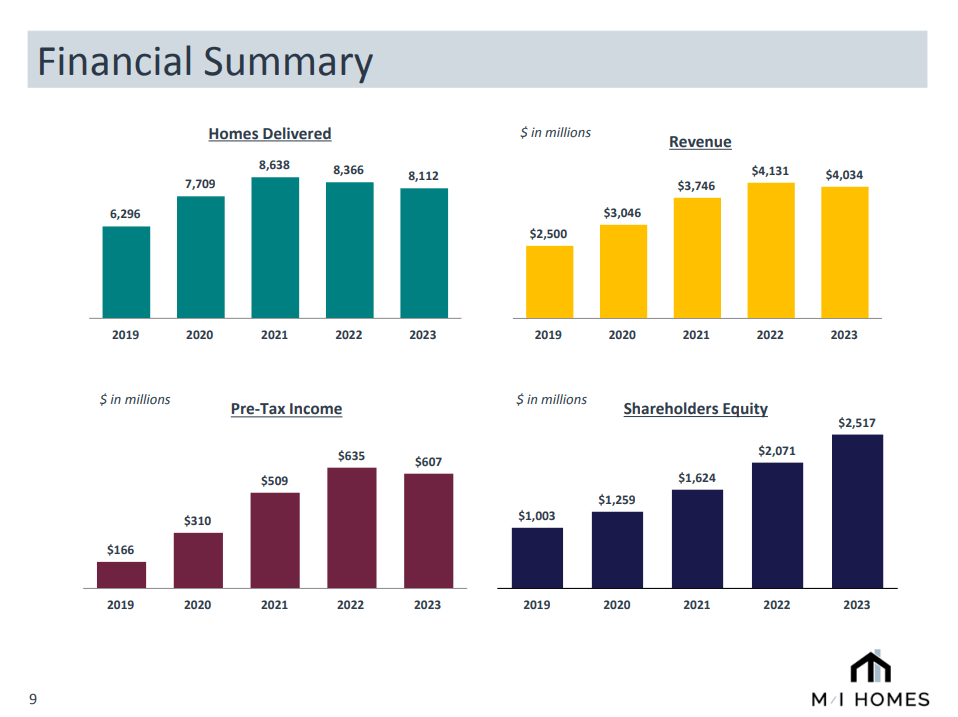

Revenue stagnated in 2023 after four consecutive years of growth, and Earnings per share have followed a similar trajectory. The number of houses delivered is obviously more complex to increase, putting a hard cap on the company’s revenues. This is something to keep in mind for MHO’s future capacity to increase its revenues.

2023 could very well have been a minor slump in a steady growth trend, yet the changes in the housing market brought by COVID-19 are still being felt in the housing market; MHO will need to evolve with the market to leave behind a rough year.

M/I Homes, Inc. Investor presentation February 2024

The number of houses delivered peaked in 2021. As the contracts take a few years to complete, revenue follows with a few years lag. Yet despite the lower number of houses sold, 2023 closed with higher revenues, the product of a hotter housing market and inflation.

This is the trend to be observed, as building companies are very sensitive to materials prices, such as lumber, a product that can even predict future inflation.

M/I Homes, Inc. Investor presentation February 2024

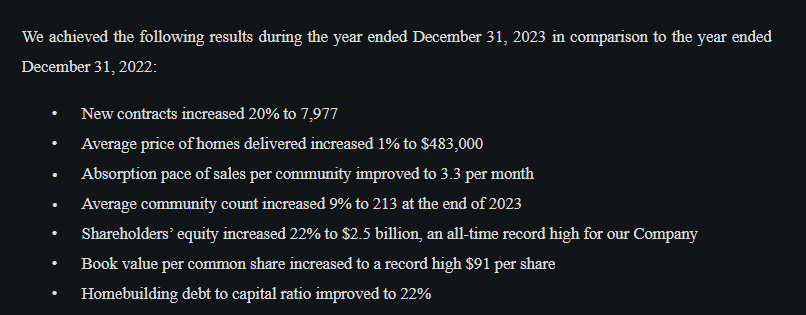

2023 had a 20% increase in contracts, but only a 1% increase in prices for houses delivered. While the rise in contracts is a good sign, the only 1% increase in prices spells a loss of real revenue for the company, as the 2023 inflation was 3.4%

A problem the company could face is having to pay for labor and materials at higher current prices while being locked in contracts that force them to charge prices at lower inflation.

This risk investors should keep in mind and watch out for any large discrepancy between the average prices of houses delivered, real inflation, and costs.

M/I Homes, Inc. Investor presentation February 2024

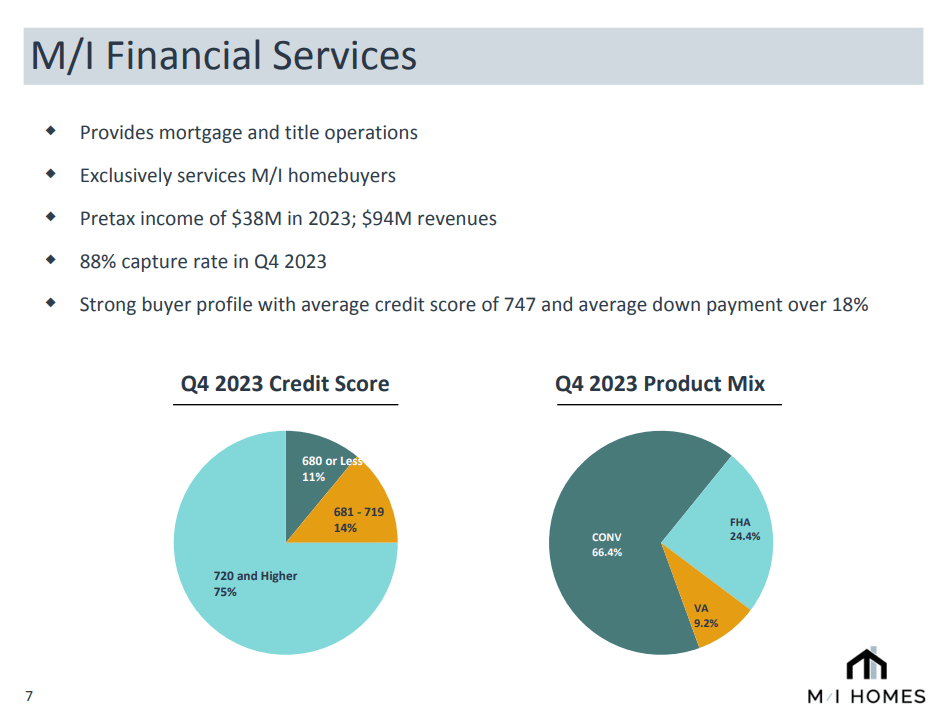

MHO also provides mortgage services that help round up the income streams for the company, yet with $4.03 billion in revenues for 2023 came $3.91 billion from homes delivered, $25.3 million from land sales, and only $93.8 million was from the financial services side of the company, it would add some security from diversification if MHO could bump up the services income.

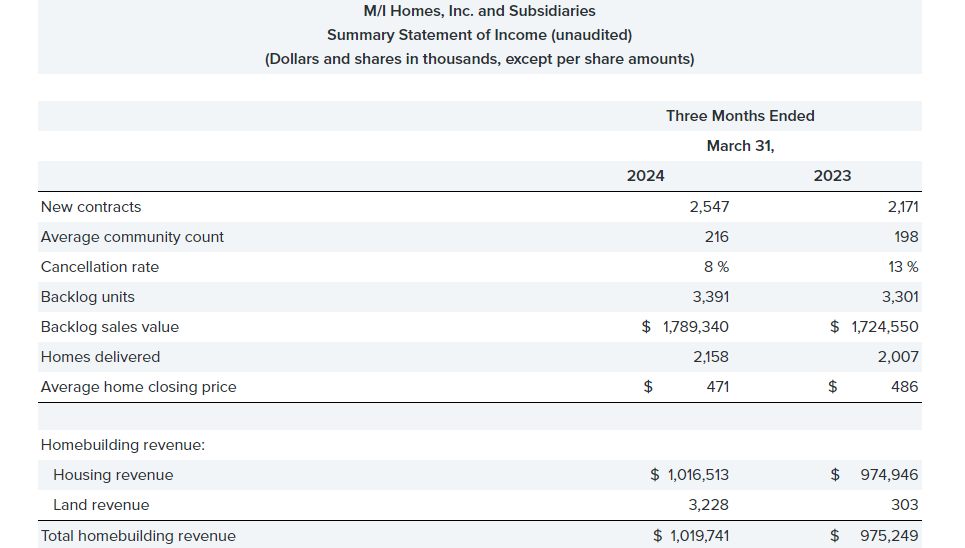

Earnings Q1 2024

The first three months of 2024 were positive for MHO, with a 17% increase in contracts, a new first-quarter record of 2,158 delivered, a 4% bump in backlog, and total sales of $1.8 billion.

MHO beat earnings estimates in its EPS by $0.82, reaching $4.78. Its revenues were $1.05 billion, with a $41.50 million surprise.

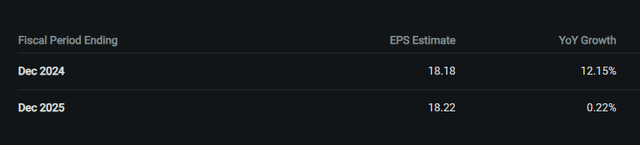

The consensus estimates give MHO a 12.15% growth for 2024. With this record number of contracts and a slight surprise, the company has a good head start on reaching the estimated growth for this year.

Seeking Alpha Quant

Yet, they will have to continue performing and have little margin for lower earnings in the following quarters.

Seeking Alpha Quant

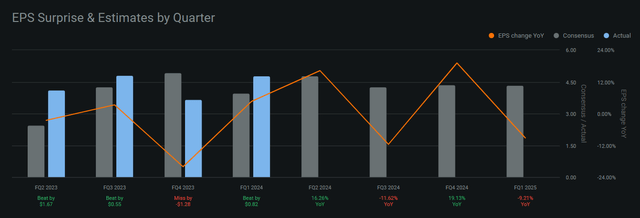

FQ2 is a crucial quarter for the company; as the highest expected EPS quarter, the company must secure a strong Q2 before the relatively lower Q3 and Q4.

With the current higher-than-expected Q1, MHO must replicate this success and build on it to reach the necessary EPS for Q2 and thus increase its margin of error for the last two quarters.

M/I Homes Reports 2024 First Quarter Results

These are some positive points for the company; this great start might promise a good 2024.

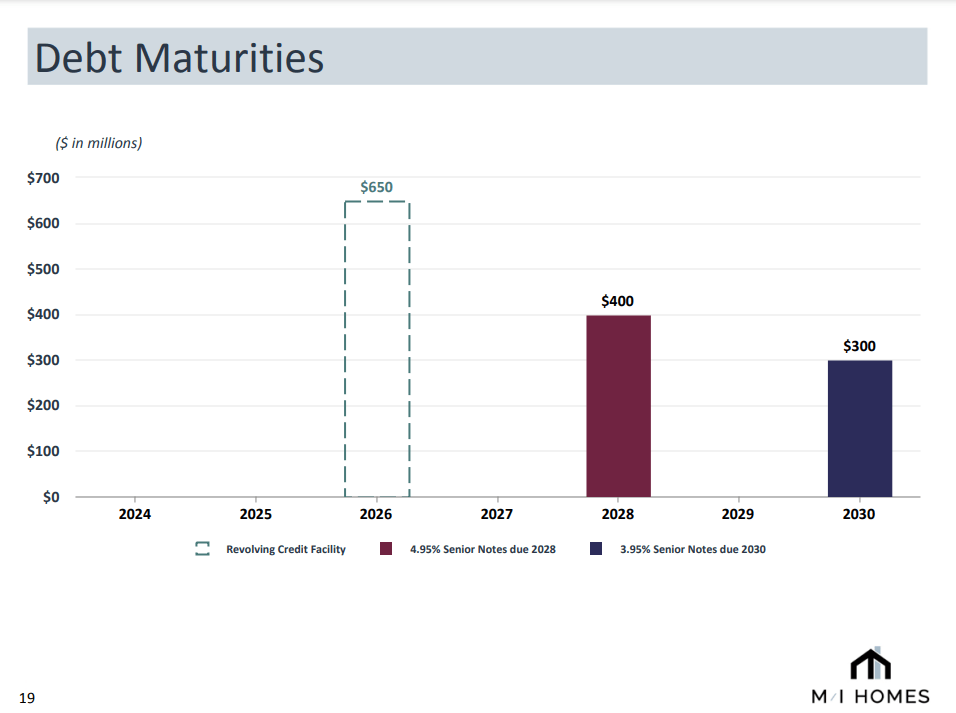

Cash stores reached $870 million, and the lack of use of the $650 million credit facility is also a desirable financial condition for MHO.

I rate this as very positive, especially the unused credit, as it proves the company is currently financially conservative and has access to credit if necessary.

Debt And Debt Ratings

Fitch’s debt rating for the company is BB. While the rating could be higher, Fitch considers MHO’s current building strategy a “Speculative Strategy” and the lack of geographical diversification a risk to the company’s capacity to pay its debt.

On the other hand, MHO’s debt maturities are still in the future, with the revolving credit line maturing in 2026 for $650 million; as of December 2023, the company had $732 million in cash and cash equivalents, giving plenty of room to pay future debt with current funds.

M/I Homes, Inc. Investor presentation February 2024

Resolving credit usage and credit rating are two vital metrics to look for. As homebuilding (and construction in general) are very CAPEX-intensive businesses, having access to credit is vital for the continued survival, let alone prosperity, of any company. I believe the current outlook is positive, but it could be better, such as with an improved rating.

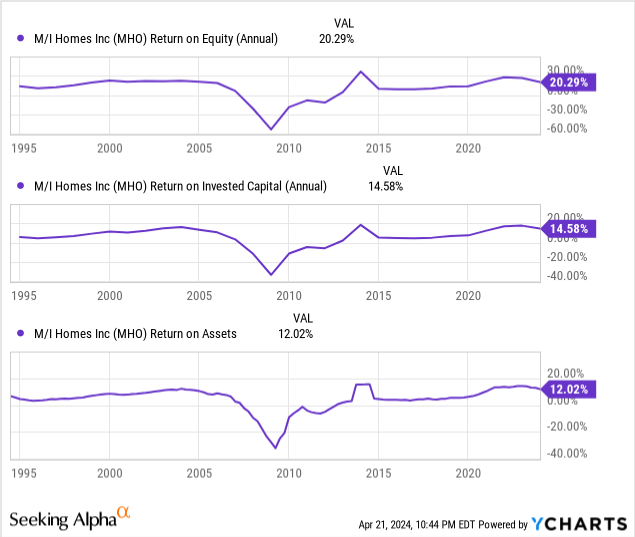

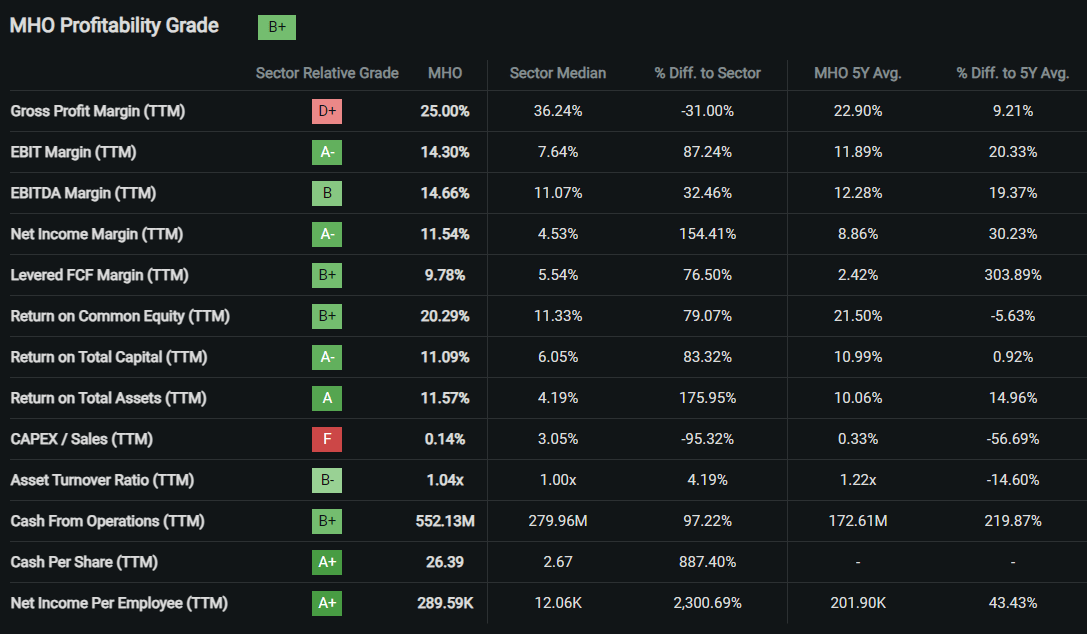

Profitability

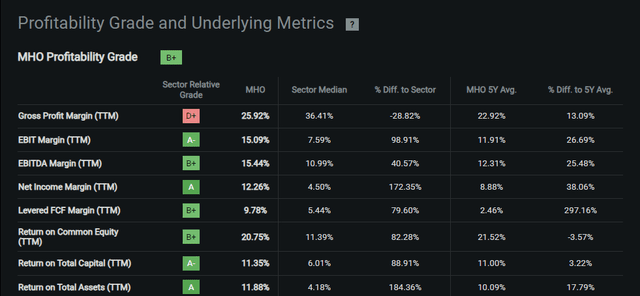

MHO shows promise, having a few key profitability indicators above its peers.

ROE, ROIC, and ROA have been stable since 2015; after a particularly rough 2009 and 2010, they went back on track, attesting to the company’s capacity to recover from losses.

The ROIC of 14.58% stands above the WACC of 10.5%, which shows that the company is creating value.

Seeking Alpha Quant

Other important metrics are the extremely high cash per share of $26.39, nearly ten times the sector’s average, and the Net Income Per Employee, which also stands comfortably above the industry. However, with such a significant difference, I believe some data might be skewed.

Overall, these metrics prove the company is profitable, with high net cash flow from revenues.

Strong Competition In The Builder’s Industry

Among the strong home builders in the USA, D.R. Horton (DHI) stands above them as the largest company; in the first quarter of 2024, they closed 87,801 homes in 33 states.

It’s clear that against the titans of the home building industry, MHO must win customers through higher quality, a better customer experience, and more customization.

I noticed a possible advantage for MHO; they offered a more environmentally friendly option:

M/I Homes Website

This could capture a growing shift in American house buying, as 73% of homebuyers want a more sustainable and environmentally conscious house.

Smaller businesses should strive to make full use of their closer contact with clients, and MHO seems to be focused on providing the best possible customer experience, at least on paper.

Still, homebuilding is a very competitive industry, and only through continuous growth of the customer base can a company prove that they are providing an excellent service in the long term.

The first comparison I have done is MHO against the sector average, to see how it fares against a broader selection of companies, I have used Seeking Alpha’s Quant Peers for the data:

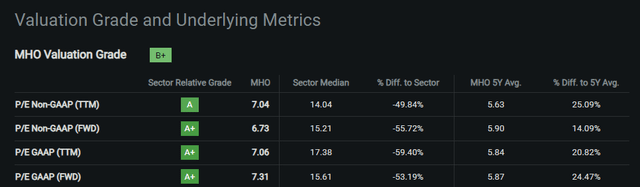

Competing with the previous group of home building companies, MHO has a few key advantages: its higher P/E (FWD) ratios, both GAAP and Non-GAAP, where the company shows a clear advantage, with higher earnings compared to its price.

Seeking Alpha Quant

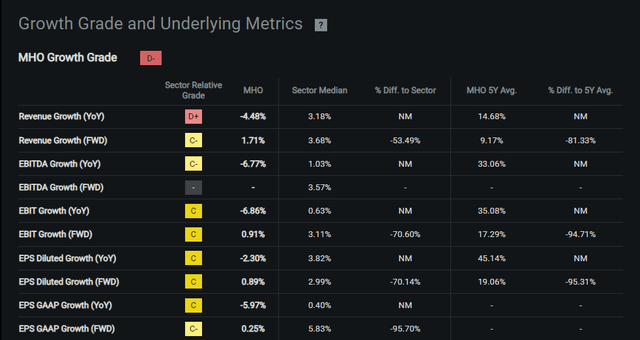

On the growth side, MHO is lagging behind the competition. With 53.49% lower Revenue Growth (FWD), this is one of the key areas the company should look to improve, as its cheap valuation could be deserved if it does not show a capacity for growth.

Especially as a 3 billion-dollar market cap company that is not yet a larger and more mature company that has outgrown its market environment.

Seeking Alpha Quant

On the other side, profitability remains a strong point for the company and is more challenging to increase than revenues.

Profitability requires efficient use of capital, a good business model, a strong customer base, and a working supply chain on both ends. MHO should leverage this to its fullest extent and increase its growth ASAP.

Seeking Alpha Quant

If the company can manage to break free from its stagnation in growth, it will do so with higher margins than the competition, thus increasing its profits at a rate superior to that of its peers.

I rate the competition section as one of the biggest challenges for the company right now. The challenge is not falling behind the rest and stagnating further, yet the company seems to have the tools to avoid this.

Valuation: Just Like A Home Buyer Would do

When buying a new house, most people will try to appraise its value. One of the most popular methods is using comparables, where a potential buyer compares the house with houses of similar size, pricing, neighbors, amenities, etc.

As MHO does not currently pay a dividend, I have decided to use the comparables method, which I find fitting, just as a customer of MHO would do when looking for a new house.

I have used Seeking Alpha’s Quant Peers to compare key metrics with the competition, where we can see similar companies, such as Tri Pointe Homes (TPH), Dream Finders Homes (DFH), Cavco Industries (CVCO), and Century Communities (CCS).

Google Spreadsheets using data from Seeking Alpha’s Quant, made by the Author.

These companies are in the same industry and have similar market caps, thus making them ideal for comparison with MHO.

From this comparison, MHO has the best value in two categories (Marked in green), P/E and EV/S, and is cheaper than the average in Price To Sales and Price To Book while having a worse-than-average value in Revenue Growth and EPS.

The P/E (FWD) once again is the strong point for the company, being 38% cheaper than this group of peers, and the also being EV/S 20.5% cheaper.

I believe this makes for an undervalued company, especially with the very attractive P/E and EV/S.

The slightly stronger-than-expected earnings for Q1 could potentially help improve the company’s growth and thus improve its value in the growth area, which is currently the weakest point for the company.

Despite this, growth is still only 1.33% away from being average.

Still, growth is a metric that should be carefully watched for this company.

Conclusion

MHO has recently proven it has not stagnated and can continue to grow in the current housing market. Its relatively cheap valuation, good profitability, strong financials, and customer-centric high-quality business make it a strong candidate for the long term.

I rate it as a BUY.

")

")