Q1 2024 Earnings Call Transcript")

")

Thesis

PIMCO is one of the largest asset managers in the world, with a very strong fixed income presence. Most investors reading our research are very familiar with the PIMCO fixed income closed end funds (‘CEFs’) which have managed very robust performances in the past decade via leveraging-up fixed income. We rarely stumble upon new names from PIMCO, but here we are reviewing the PIMCO Senior Loan Active Exchange-Traded Fund ETF (NYSEARCA:LONZ). We were unaware of this exchanged traded fund from PIMCO, a vehicle which focuses on leveraged loans and has an active approach to its portfolio management.

LONZ is a fairly new fund, having come to market only in 2022, on the back of the higher rates environment spurred by the Fed hiking rates. In this article we are going to have a closer look at this fund, its composition, its performance versus a peer group, and form an opinion on why a retail investor is served by going long this name.

An active floating rate fund

LONZ focuses on leveraged loans, with an active mandate. Rather than passively follow an index, the fund tries to outperform the iBoxx USD Liquid Leveraged Loans Index:

iBoxx USD Liquid Leveraged Loans Index comprises approximately 100 of the most liquid, tradable USD leveraged loans. Index constituents are derived using selection criteria such as loan type, minimum size, liquidity, credit ratings, initial spreads and minimum time to maturity. It is not possible to invest directly in an unmanaged index.

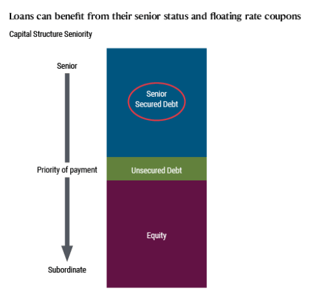

What LONZ brings to the table is the unparalleled depth of the PIMCO research platform, and its ability to pick winning credits. Via its build LONZ takes positions in an asset class which sits at the top of the capital structure:

Capital Structure (PIMCO)

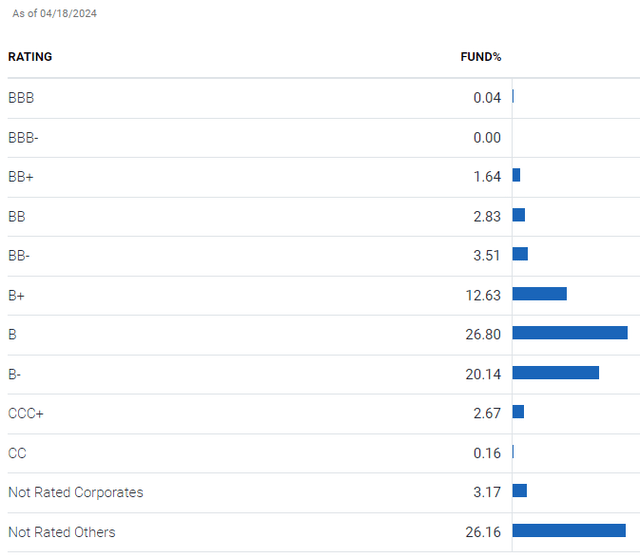

The fund is composed of over 270 names with an average yield to maturity of 9% and a portfolio weighting below 1.7% of the fund. The bulk of the portfolio sits in single-B names for this fund:

Ratings (PIMCO)

We can see the ETF is overweight single-B credits, evenly spread out among B+, B and B- credits. There is also a substantial bucket of not rated credits. As a reminder, in the leveraged loan space issuers sometimes obtain a private rating which the fund knows, but cannot distribute to the public. Private ratings are obtained for cost purposes (it is cheaper to obtain one-off private ratings than have an ongoing public one).

The fund has a very low volatility

What is very particular about this actively managed fund is its very low volatility. Under the ‘Risk’ tab on the Seeking Alpha platform an investor can find the key metrics for the name, and can see a low standard deviation of 2.28, and an annualized volatility of 1.95%. These figures indicate a fund that does not experience deep drawdowns, and means an investor has the peace of mind of being flat or up on most trading days.

Risk in today’s environment is very important in our mind. Obtaining a high 7% yield can come with significant drawdowns, and investors need to pay attention not only to how much a fund yields, but also its risk and volatility.

LONZ has a low volatility profile given the asset class it contains, namely leveraged loans. As highlighted in a section above, leveraged loans sit at the top of the capital structure, and thus are first to get a recovery in a bankruptcy proceeding. This structuring feature gives them a low volatility profile since investors are fairly certain they will get their money back, even if the issuer goes under. In fact the rating agencies assign each leverage loan a recovery rating. The higher the recovery rating, the higher the probability of full recovery.

Leveraged loans have a first lien on underlying company assets, thus asset heavy companies (think industrials as an example) will in most instances show 100% recoveries on leveraged loans, with unsecured bonds and equity holders taking the hits in case of a restructuring.

The active management helps the fund outperform

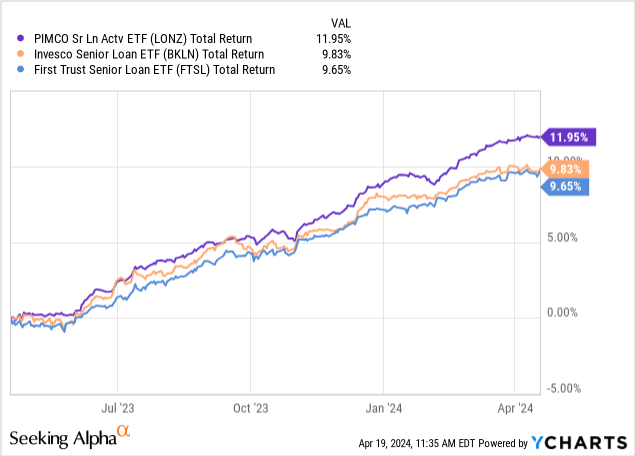

One of the key features for LONZ is its active management by PIMCO. Active management from a large platform like PIMCO results in outperformance:

On a 1-year lookback we can see how LONZ has outperformed both the Invesco Senior Loan ETF (BKLN) and the First Trust Senior Loan ETF (FTSL). The outperformance is even more notable when we look at the total return figure which is north of 11%. Think about that for a second – this fund has delivered an 11% return with an annualized volatility of only 2%.

We feel LONZ will keep outperforming in today’s environment because bankruptcy proceedings will become more numerous, and the environment is a bottoms-up research game. The better the manager at picking undervalued names, the better the outcome given the binary differentiation currently seen in the market.

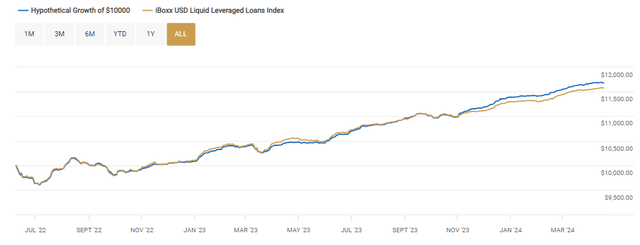

Since inception the fund has also managed to fulfil its other goal, namely beating the index:

Return vs Index (returns)

The blue line in the graph above represents the hypothetical growth of $10,000 invested in the fund, while the brown line represents the total return of the same cash invested in the leveraged loan index. While the outperformance is small here, it nonetheless matters. We have seen many ETFs and CEFs failing the simple task of outperforming their underlying indices.

An investor always needs to look at how an active fund does versus a simple passive index or index ETF. Active management involves higher fees (and the adjusted expense ratio for this name is 60 bps), and those fees need to be justified. If active funds do not outperform passive ones, then retail investors should not pay said fees. A manager charging high fees to perform worse than a passive index is not a manager to invest with.

Conclusion

LONZ is an under the radar fixed income fund from PIMCO. The name invests in floating rate leveraged loans, and was launched in 2022. The ETF has an active approach to its collateral and has managed a 11% total return in the past year with an annualized volatility of only 2%. The results put the fund head and shoulders above its peers, with its active management from a robust platform like PIMCO being the differentiator here. Although the fund is overweight single-B names we expect it to continue to outperform until the Fed starts cutting rates. We like this name and the platform and feel its low volatility and high total returns are appealing for 2024.