")

Recently, I saw the news that Laurentian Bank’s (TSX:LB:CA) peer, Canadian Western Bank (CWB:CA), was being acquired by National Bank of Canada (NA:CA). Since the two banks are similar in size, C$48.4 billion in total assets for Laurentian vs. C$42.0 billion for Canadian Western, my immediate thought was whether Laurentian will be next in line to be acquired in the current consolidation wave.

However, after reviewing the NA/CWB transaction and Laurentian’s latest results, I believe there are reasons Laurentian failed to find a suitor last year. The bank does not have attractive assets that warrant a takeover attempt by its Big-6 competitors.

As a standalone bank, Laurentian continues to struggle financially, reporting a massive impairment and restructuring charge in the latest quarter. Until I see signs of improvement in the bank’s efficiency and profitability, I recommend investors stay on the sidelines despite the bank’s cheap valuations.

(Author’s note, all financial figures in this article are in Canadian dollars)

Brief Company Overview

For those not familiar, Laurentian Bank is Canada’s 8th largest bank (after RBC acquired HSBC Bank of Canada). Laurentian primarily operates in the provinces of Quebec, Ontario, Alberta, British Columbia, and Nova Scotia (Figure 1).

Figure 1 – Top 10 banks in Canada (wallstreetmojo)

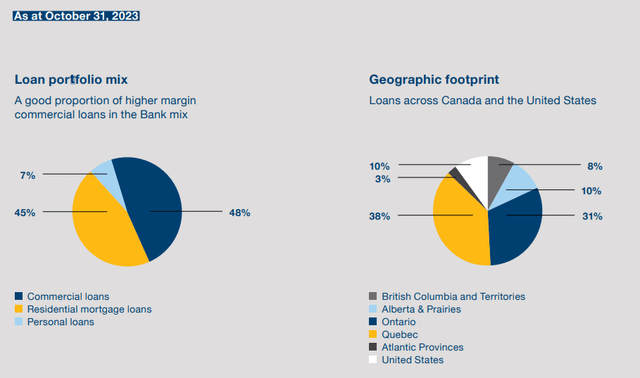

Laurentian is known as a personal and commercial lender, focused on small and medium enterprises, with an ancillary capital markets business focused on niche verticals like green and social bonds (Figure 2).

Figure 2 – LB loan portfolio mix, October 2023 (LB annual report)

Another Wave Of Consolidation In Canadian Banking?

Unlike the United States with more than 4,000 commercial banks, the Canadian banking landscape is highly concentrated with the Big 6 (RBC, TD, Scotia, BMO, CIBC, NA) commercial banks dominating the market for loans and deposits.

Despite the oligopolistic market structure, Canadian banking regulators appear unconcerned about further consolidation, as they recently allowed RBC to acquire the assets of HSBC Bank of Canada.

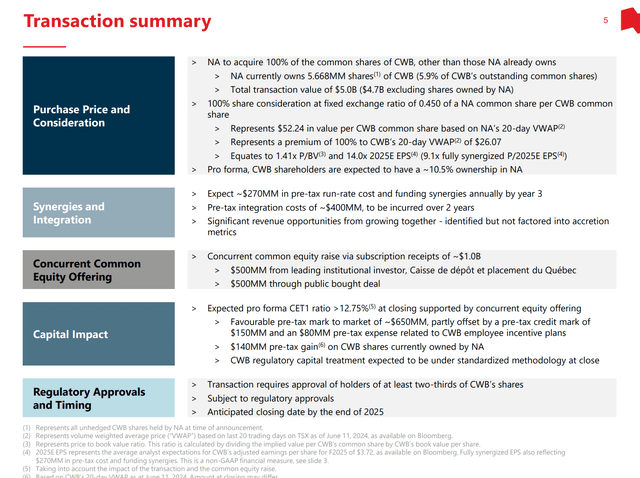

In recent weeks, we have also seen National Bank announce the acquisition of Canadian Western Bank in a $5 billion transaction, as mentioned at the beginning of this article (Figure 3).

Figure 3 – NA to acquire CWB for C$5 billion (NA investor presentation)

Rationale For NA/CWB Transaction

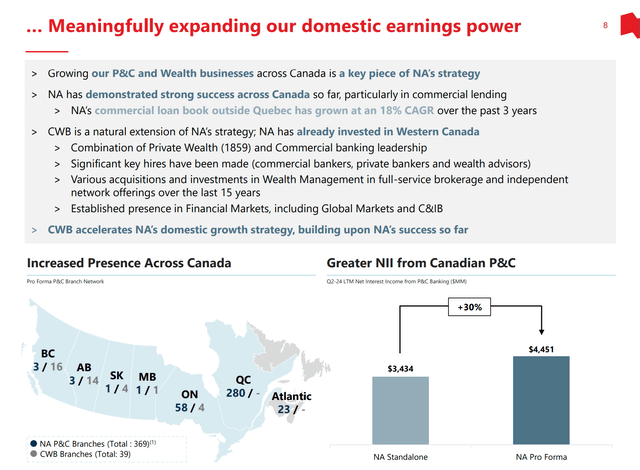

For National Bank, its rationale for acquiring Canadian Western makes a lot of strategic sense. CWB is a commercially focused bank specializing in business and personal banking, equipment financing, trust services, and wealth management. Most importantly, CWB has a strong presence in Western Canada, where National is historically weak. CWB will add 39 branches to National’s network, with virtually no overlap (Figure 4).

Figure 4 – CWB has a complementary branch network (NA investor presentation)

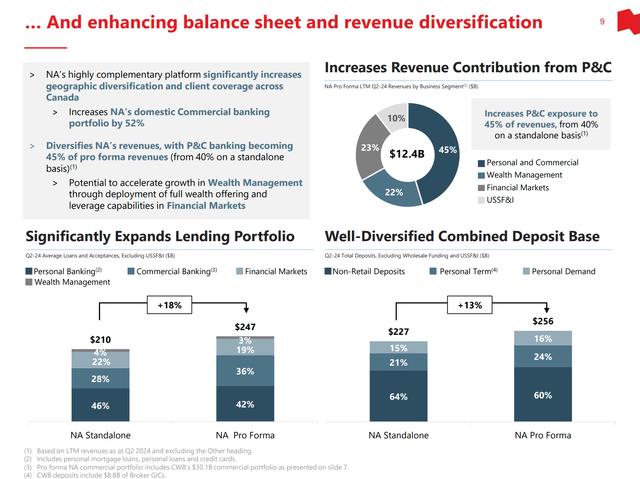

CWB will also enhance National’s revenue diversification by bolstering its commercial loan book by 52% (Figure 5).

Figure 5 – CWB increases NA’s commercial loans (NA investor presentation)

Laurentian Left With No Dance Partner

Unfortunately, upon further reflection, I do not believe Laurentian will be the subject of any takeover attempts in the near future. First, readers should recall my article from last summer, when Laurentian put itself up for sale by announcing a strategic review process.

Unfortunately, after likely inviting every Big 6 bank and other financial institution that may be interested in Laurentian into its data room, the bank’s strategic review was concluded in September without a deal.

In my opinion, the primary issue with any Laurentian takeover is that Laurentian does not have any assets of significant value to its Big-6 competitors. For example, while CWB has a complementary network of bank branches in Western Canada that appealed to National Bank, Laurentian’s branches are predominantly located in Eastern Canada, which overlap with many of the Big 6 banks.

Niche Businesses Not Big Enough To Warrant Takeover

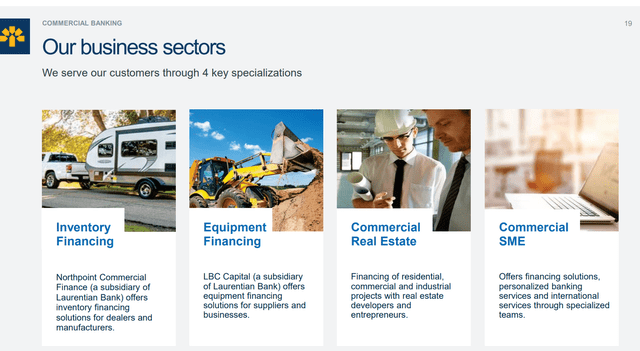

Furthermore, while Laurentian does have a leadership position in certain niche business lines such as inventory and equipment financing, these businesses are likely not large enough to warrant a full-scale takeover of the bank itself (Figure 6).

Figure 6 – LB has leadership in niche areas (LB investor presentation)

That is why Laurentian will likely have to struggle alone in its ‘Path Forward’.

Lagging Fundamentals Warrant Discounted Valuations

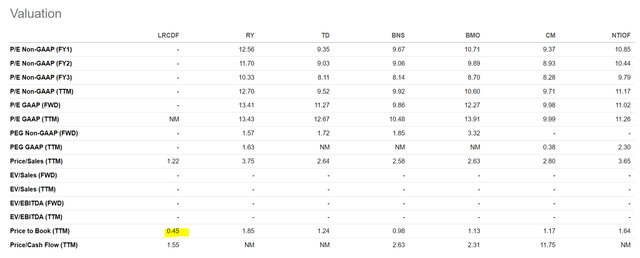

On the positive side, Laurentian Bank does trade at very discounted valuations. At a recent price of $26.55, Laurentian is trading at 0.45x Price-to-Book value (“P/B”), 1/3 to 1/2 of its Big-6 bank peers (Figure 7).

Figure 7 – LB vs. peer valuations (Seeking Alpha)

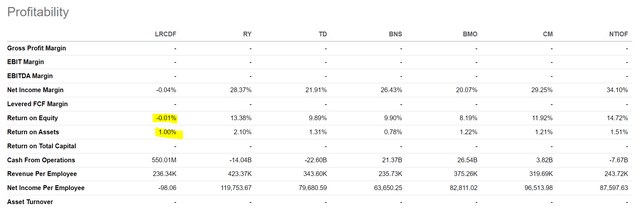

However, I believe Laurentian’s discounted valuation may be warranted as the bank is sub-scale and earns significantly lower return-on-equity (“ROE”) and return-on-assets (“ROA”) compared to its peers (Figure 8).

Figure 8 – LB vs. peer profitability (Seeking Alpha)

Recent Quarter Continues To Show Laurentian Struggling

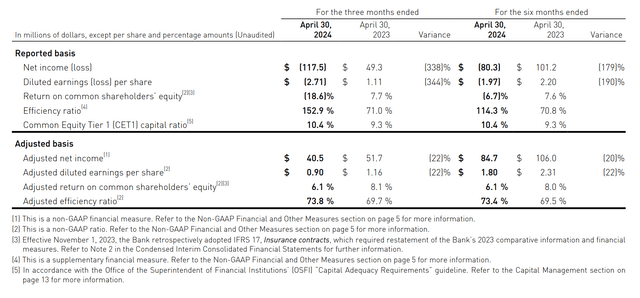

For example, in the most recently reported Q2/F24 earnings, Laurentian reported a large loss of $2.71 / share, as the bank had to take $197 million in impairment and restructuring charges related to its Personal and Commercial (“P&C”) segment (Figure 9).

Figure 9 – LB Q2/F24 financial summary (LB Q2/F24 MD&A)

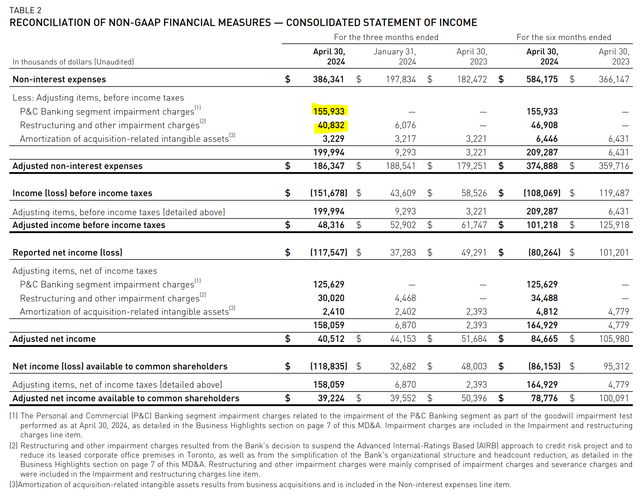

Looking at the details, Laurentian recorded $156 million in goodwill impairment charges to its P&C business, along with $41 million in restructuring charges for the bank as a whole (Figure ). This puts into question the quality of historical management decisions since goodwill impairment arises from past acquisitions.

Figure 10 – LB impairment details (LB Q2/F24 MD&A)

Investors are reminded that the current CEO, Eric Provost, was formerly EVP of Commercial Banking and President of the Quebec market, so he shares some of the blame for these historical acquisitions (Figure 11).

Figure 11 – Current CEO, Eric Provost, was formerly head of Commercial Banking and President of the Quebec market (LB investor presentation)

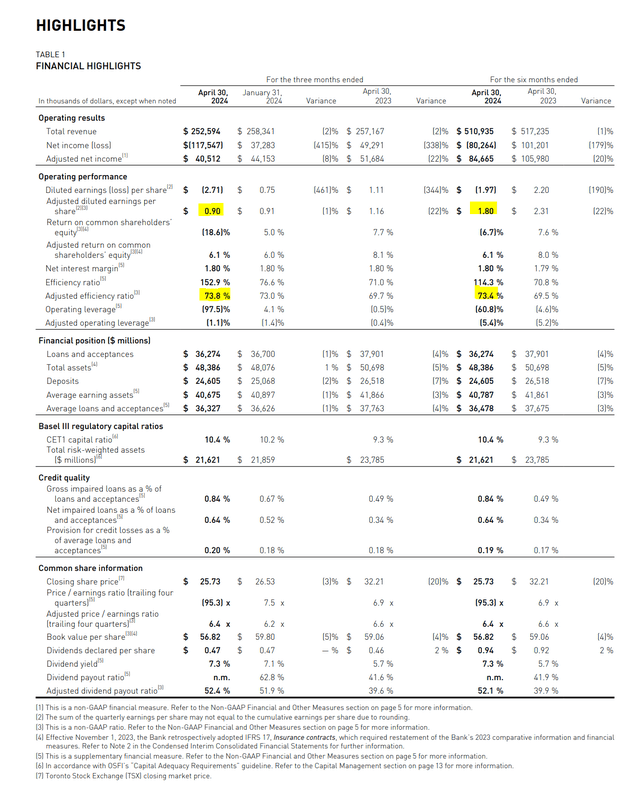

Even adjusting for the charges, Laurentian reported a 22% YoY decline in YTD adjusted earnings to $1.80 / share, and a peer-lagging efficiency ratio of 73.4% (Figure 11).

Figure 11 – LB adjusted Q2/F24 financial performance shows continued deterioration (LB Q2/F24 MD&A)

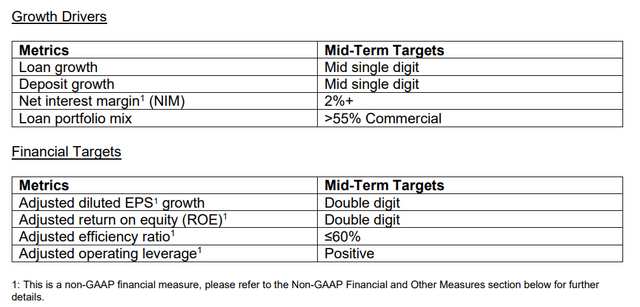

Simply put, despite management’s bravado, Laurentian still has a very long way to go to achieve management’s goal of double-digit EPS growth, double-digit ROE, and sub-60% efficiency (Figure 12).

Figure 12 – Laurentian’s ambitious medium-term targets (company reports)

Conclusion

Recently, National Bank of Canada announced the acquisition of Canadian Western Bank, sparking speculation of further consolidation in Canadian banking. However, after reviewing the NA/CWB transaction and Laurentian’s latest results, I believe there is a reason Laurentian’s strategy review came up empty last year.

Simply put, the bank is a sub-scale lender with assets that overlap with its peers. This makes any Big-6 bank acquisition of Laurentian hard to justify.

As a standalone entity, Laurentian continues to struggle financially, with the bank recording a massive impairment and restructuring charge in the latest quarter. While management has ambitious goals of improving efficiency and profitability in the medium term, so far, I have seen no evidence of the company’s strategy coming to fruition.

Although Laurentian is very cheap, trading at 0.45x P/B, I do not see any near-term catalysts to unlock shareholder value. I maintain my hold rating on Laurentian Bank’s shares.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")

")

")