")

Thesis overview

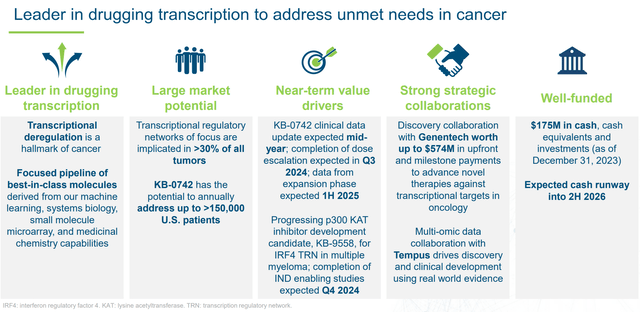

Kronos Bio, Inc. (NASDAQ:KRON) is an early clinical-stage biotech targeting dysregulated transcription pathways in cancer. KRON’s discovery platform aims to identify optimal targets within transcription regulatory networks to suppress oncogenic activity while avoiding (to the extent possible) off-target gene expression dysregulation.

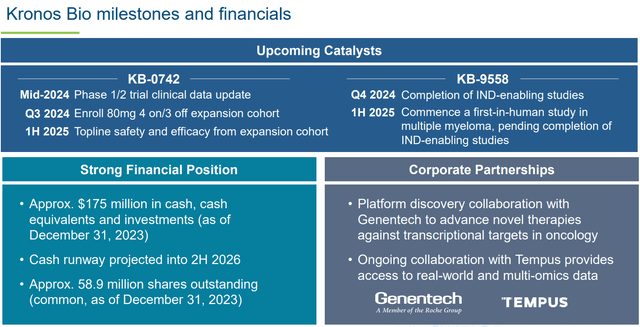

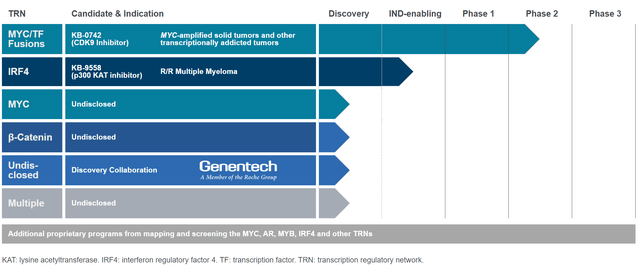

KRON currently has only one clinical-stage candidate (in phase 1/2 stage), KB-0742, an orally bioavailable selective CDK9 inhibitor being developed for MYC-amplified and other transcriptionally addicted tumors. KRON’s second asset, KB-9558, is being developed for multiple myeloma and initiation of the first trial in humans is planned 1H 2025. KRON is also developing additional undisclosed assets, all in the pre-clinical stage, including a preclinical collaboration with Genentech.

To sum up my thesis, I believe KRON is a good buy now for the following reasons:

- KRON is currently trading well below cash and at a negative enterprise value.

- KRON estimates a cash runway into 2H 2026, well beyond important catalysts.

- KRON has a promising discovery platform with big pharma collaboration (which validates the appeal of KRON’s discovery platform).

- KB-0742 has demonstrated promising antitumor activity and good tolerability in the ongoing ph1/2 study. Αn update is expected in ASCO this June, and top-line results are expected in 1H 2025.

- KB-9558 has demonstrated selective and strong antitumor activity in preclinical studies and has potential to be used both as monotherapy (in patients refractory to other treatments) and in combination with other approved treatments (in earlier line patients).

- CEO recently bought $1.5M worth of shares.

Summary of bullish thesis for KRON (KRON’s company presentation)

KRON is well funded through next catalysts (KRON’s company presentation)

Overview of KRON’s prior failures

One explanation about the market’s disbelief in KRON is failure of its 2 prior lead assets (SYK inhibitors entospletinib and lanraplenib) against acute myeloid leukemia. So it is worth briefly discussing those.

In November 2022, KRON announced discontinuation of its ph3 entospletinib trial “for strategic reasons.” The trial was stopped due to slow enrollment and challenges in “enrolling a genetically defined subset of patients in a front-line setting,” rather than due to adverse events or lack of efficacy signals. KRON then chose to focus on its next-generation SYK inhibitor (lanraplenib), which had important advantages (once vs. twice daily dosing, and ability to be taken fed or fasted, as well as with proton pump inhibitors). However, in December 2023 KRON announced discontinuation of its mid-phase lanraplenib AML trial based on review of ph1b data, although KRON is still open to further development with a partner.

Of note, neither of the above 2 assets were developed by KRON. Both entospletinib and lanraplenib were acquired from GSK (note that “Prior to joining Kronos Bio, Norbert was the Executive Vice President, Research and Development and Chief Scientific Officer at Gilead Sciences”). On the contrary, both current assets (KB-0742 and KB-9558) have been internally developed by KRON.

Overview of KRON’s discovery platform

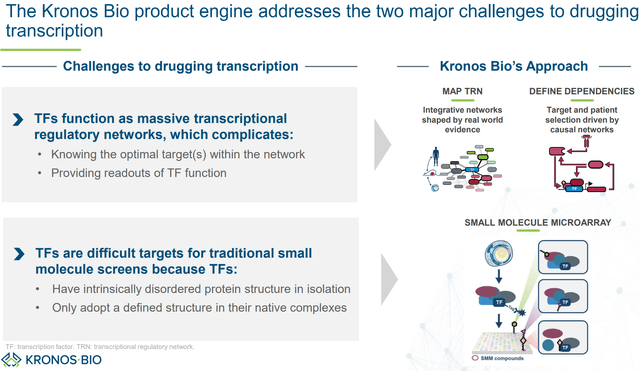

One of the hallmarks of cancer is dysregulated transcription. Sometimes tumors are “addicted” to a single activated oncogenic protein/pathway, and inhibition of these pathways can result in cancer cell death. This makes transcription factors (TFs) a good target for drug development. TFs are proteins that bind to DNA and regulate gene expression. A single TF can regulate several genes, and each gene can be regulated by more than one TFs. Furthermore, TFs don’t act alone, but as part of a TF complexes (i.e., TFs + their cofactors). Finally, this process is regulated by (often >1) upstream signaling pathways. This results in massive regulatory networks, making it challenging to specifically target oncogenic signals without off-target adverse effects.

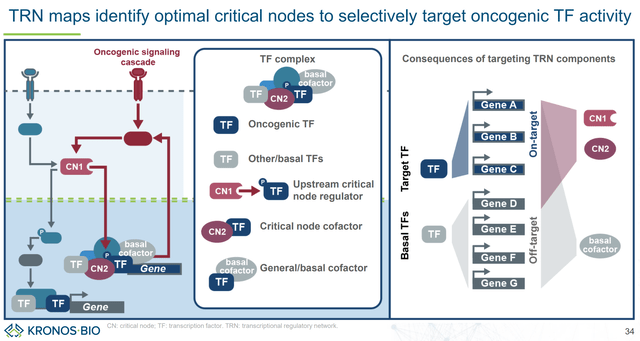

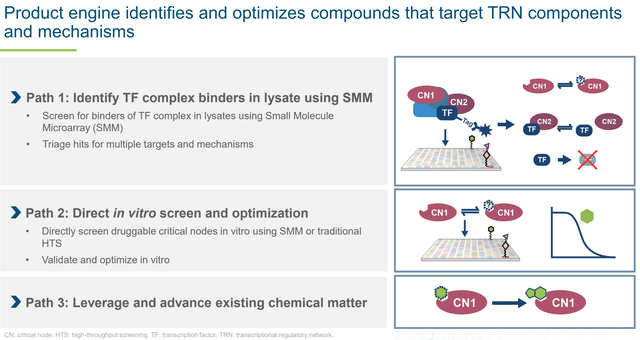

KRON’s goal is to identify optimal targets within these regulatory networks to suppress oncogenic pathways, while at the same time avoiding off-target gene expression dysregulation (which would mean off-target adverse effects). To achieve this, KRON is looking at TFs “in context” rather than isolated proteins. With its Small Molecule Microarray (SMM) platform, KRON can conduct high throughput binding assays in cell lysates, which maintains TF complexes, thus allowing identification of binding pockets “in context” in either the TF itself or its cofactors. Furthermore, by analyzing TFs in various cell types (e.g., blood, lung etc.) and states (e.g., normal vs. tumor cells) KRON can identify “whether different cofactors assemble to make unique transcription regulatory complexes to regulate genes within that specific context.” KRON’s approach is summarized in the figures below.

Overview of KRON’s discovery platform (KRON’s company presentation)

The ideal goal is to target oncogenic TF activity sparing basal TF activity (thus avoiding off-target adverse effects) (KRON’s company presentation)

KRON targets TF complexes rather than TFs as isolated proteins (KRON’s company presentation)

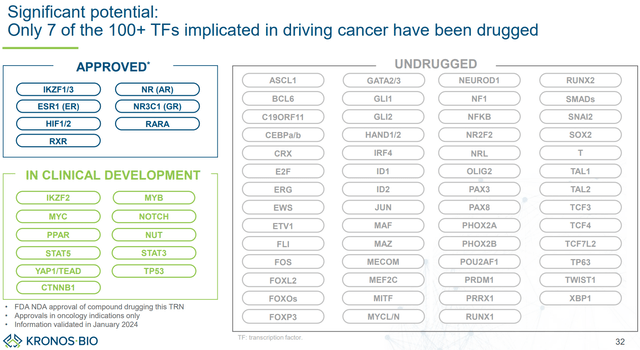

Importantly, last January KRON announced a collaboration with Genentech (which in 2009 was acquired by Roche for about $47B) to identify small-molecule drugs against selected transcription factor targets using KRON’s discovery platform. KRON received a $20M upfront payment and is eligible for up to $554M milestone payments (“including discovery, preclinical, clinical and commercial milestones”). This collaboration is important not only for the potential future revenue for KRON, but also because it validates big pharma interest in KRON’s discovery platform. This is a major reason to be bullish for KRON long-term. Notably, according to KRON there is a lot of room for developing drugs against dysregulated transcriptional pathways in cancer (see figure below).

KRON’s discovery platform has potential to identify drug candidates for numerous TFs that remained “undrugged” (KRON’s company presentation)

Overview of KB-0742

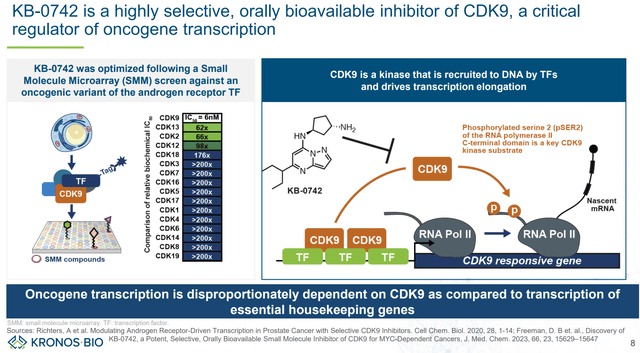

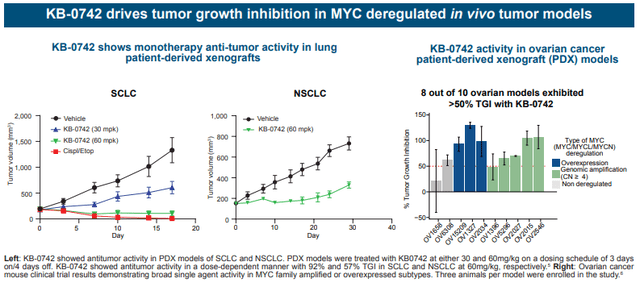

KB-0742 is KRON’s lead asset. KB-0742 is an orally bioavailable, highly selective and potent CDK9 inhibitor. For interested readers, the preclinical development of KB-0742, from discovery to optimization and in vivo validation, is described in publications in Cell Chem Biol and J Med Chem. Of interest is that KB-0742 provides validation of KRON’s SMM screening platform. In vivo antitumor activity has been proven in patient-derived xenograft models and KB-0742 is currently been evaluated in an ongoing phase 1/2 trial.

Overview of KB-0742’s mechanism of action and selectivity (KRON’s company presentation)

Summary of pre-clinical data (AACR-NCI-EORTC 2023)

KB-0742 phase 1/2 design

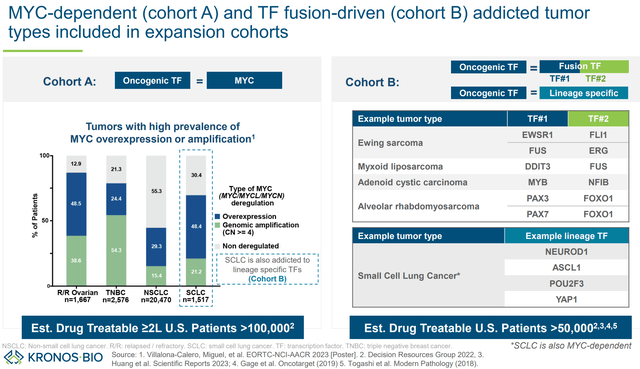

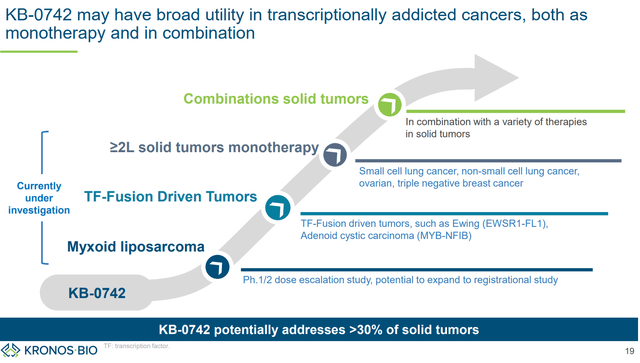

KB-0742 is being evaluated in an ongoing phase 1/2 trial against relapsed/refractory (without other available therapeutic options) solid tumors or non-Hodgkin lymphoma, focusing on specific cancer types to increase probability of responses:

- Tumor types associated with high prevalence of MYC overexpression/amplification (SCLC, epithelial ovarian cancer, TNBC, NSCLC)

- Other epithelial solid tumor with evidence of MYC copy number gain

- Diffuse large B-cell lymphoma with documented MYC translocation or Burkitt’s lymphoma

- Sarcoma of histologic subtypes known to be associated with transcription factor fusion, specifically: i) Myxoid/round cell sarcoma ii) Clear cell sarcoma iii) Desmoplastic small round cell tumor iv) Low-grade fibromyxoid sarcoma, v) Extraskeletal myxoid chondrosarcoma vi) Ewing sarcoma vii) Alveolar rhabdomyosarcoma

- Chordoma, NUT midline carcinoma, or adenoid cystic carcinoma

Note that, with a couple of exceptions, confirmation of MYC overexpression/amplification is not a requirement (maybe due to practical challenges), which means treatment efficacy may be underestimated by including patients with tumors without MYC dysregulation.

Tumor types of interest for the phase 1/2 (KRON’s company presentation)

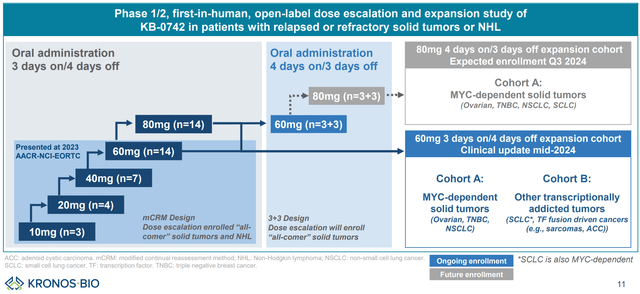

The different dosing cohorts are summarized in images below. KB-0742 is being evaluated in increasing doses to assess tolerability and define maximum tolerable dose (MTD) and appropriate dosing regimen for the next stages of clinical development. Patients were initially dosed with a 3 days on/4 days off regimen (doses: 10mg, 20mg, 40mg, 60mg, 80mg). Next, a different dosing regimen (4 days on/ 3 days off) will be tried.

Phase 1/2 design (KRON’s company presentation)

KB-0742 phase 1/2 preliminary results

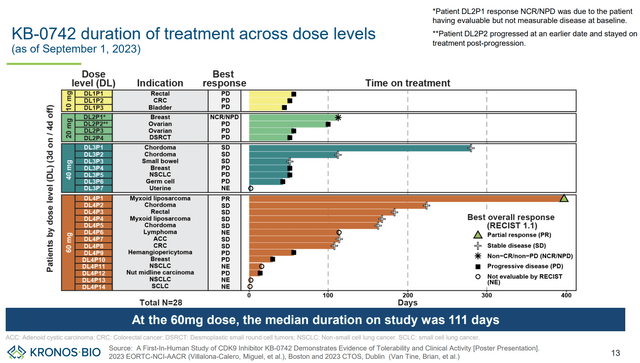

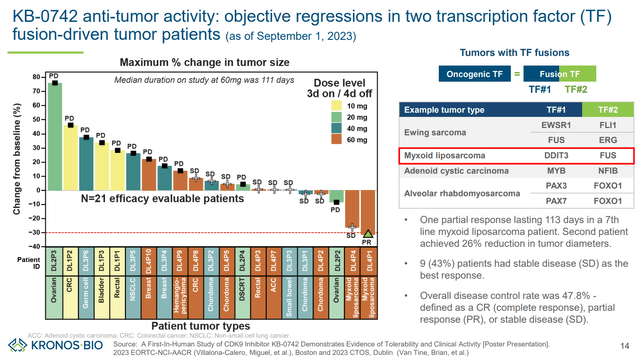

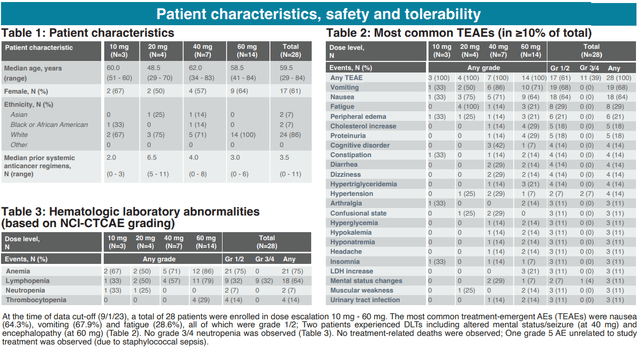

Preliminary results (including safety and efficacy) have been presented for doses up to 60mg (3 days on/ 4 days off) in AACR-NCI-EORTC 2023. No tumor responses were observed in the lowest dosing cohorts (10mg and 20mg), In the 40mg cohort n=3 (50% of evaluable patients) had stable disease, but no partial/complete responses were demonstrated. In the 60mg cohort, n=1 partial response (10% of evaluable patients) and n=6 patients with stable diseases (60% of evaluable patients) were documented, corresponding to a disease control rate of 70% (among evaluable patients).

Swimmer plot (KRON’s company presentation)

Waterfall plot (KRON’s company presentation)

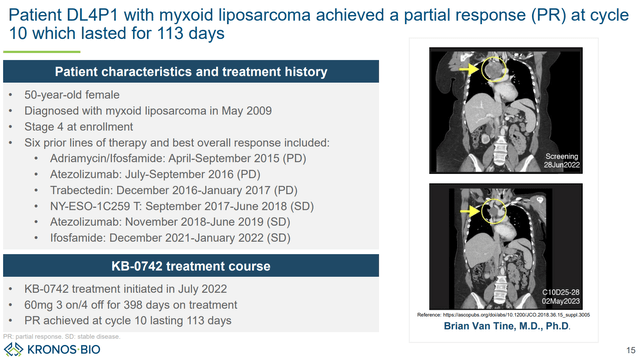

The single response was observed in a patient with myxoid liposarcoma (a tumor type with TF fusion). Furthermore, a 26% tumor reduction (stable disease) was achieved in the other patient with myxoid liposarcoma. This suggests high potential in carefully selected transcriptionally addicted tumors.

Description of the single patient demonstrating a partial response (KRON’s company presentation)

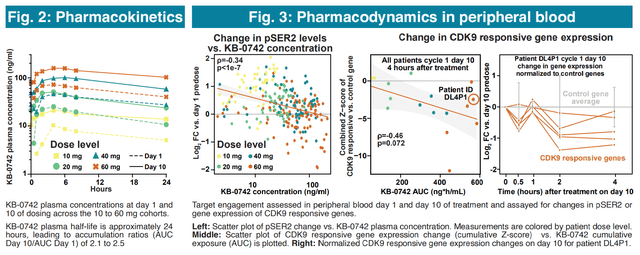

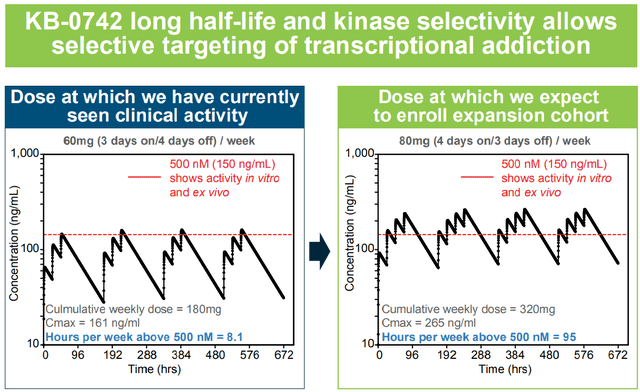

Importantly, according to pharmacokinetic/pharmacodynamic data (figures below) it looks like the lower dosing cohorts (10mg, 20mg, 40mg) were insufficient, while the 60mg cohort achieved target concentrations for only 8.1 hours/week. Therefore, with higher doses (80mg) or the 4 days on/ 3 days off dosing regimen, longer exposure to therapeutic concentrations is to be expected, which could result in better antitumor efficacy (but potentially at the cost of more adverse effects). An update on the ph1/2 trial, “including data from the 80mg three days on/four days off dosing regimen,” is expected in ASCO 2024 (abstracts to be released May 23, poster to be presented June 1). The update will also likely include efficacy data on previously non-evaluable patients (n=4 in the 60mg cohort). Data from the expansion phase (4 days on/ 3 days off) are expected in H1 2025.

Pharmacokinetic/pharmacodynamic data from the ph1/2 showing a dose-dependent on-target activity (AACR-NCI-EORTC 2023 poster)

Higher doses and/or the 4 days on/ 3 days off regimen will result in longer exposure to therapeutic concentrations (AACR-NCI-EORTC 2023)

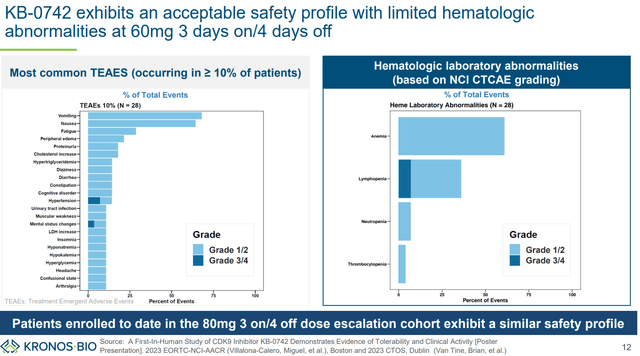

With regard to safety/tolerability, nausea (64%), vomiting (68%) and fatigue (29%) were the most common adverse effects. All were grade 1/2. No grade 3/4 neutropenia was observed (a dose-limited toxicity that has been observed with a prior orally bioavailable CDK9 inhibitor, discussed in next section). Nausea and vomiting were manageable with antiemetic. The MTD has not been reached yet.

KB-0742’s safety profile (KRON’s company presentation)

Safety and tolerability data (AACR-NCI-EORTC 2023 poster)

To sum up above results, KB-0742:

“demonstrated on-mechanism, single agent antitumor activity and a manageable safety profile in heavily pre-treated patients with transcriptionally addicted solid tumors.”

Targeting CDK9- competition

The list of other companies targeting CDK9 is long. This is both good and bad. Good because interest in targeting CDK9 validates the target. Bad because of potential competition. A detailed comparison of candidates under development is beyond the scope of this article, but interested readers can check recent reviews (J. Med. Chem, Biochemistry, and Cancer Biol Ther). Briefly, CDK9 inhibitors /degraders under development vary in terms of selectivity, potency, safety, pharmacokinetics, and route of administration (orally vs. parenterally). All are in early stages of clinical development (phase 1/2 stage). Few are both highly selective and orally bioavailable.

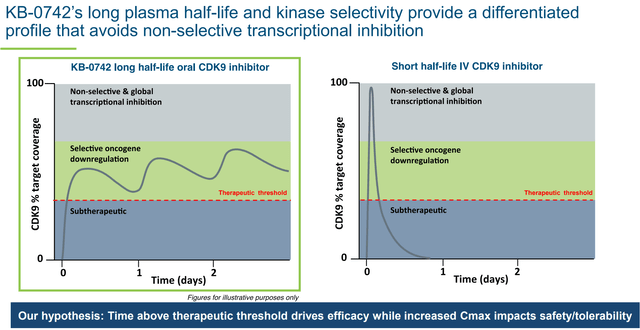

KB-0742 is neither the most selective nor the most potent candidate under development (e.g., see this publication comparing to VIP152). Nevertheless, it is one of the few orally bioavailable candidates that is both highly selective and potent. Furthermore, the oral route of delivery, in combination with a long half life, results in an increased time above therapeutic threshold (a big theoretical advantage over intermittent IV infusion) while avoiding off-target side effects (seen at higher concentrations and/or with less selective molecules). As explained in the latest 10-K, KRON is

“pursuing an intermittent dosing strategy, with the goal of maintaining a consistent level of target coverage for several days followed by a drug holiday to allow for recovery in normal tissue. Many other CDK9 inhibitors possess short half-life and many are administered intravenously, resulting either in pulsatile target coverage or short overall duration of target coverage. By contrast, KB-0742 has demonstrated oral bioavailability and a twenty-four hour plasma half-life in humans. We believe that this is an attractive profile and affords the flexibility to establish a therapeutic index by varying dose and schedule to achieve optimal target coverage in tumor.”

Optimized pharmacokinetics are important to achieve a sustained therapeutic effect without off-target adverse effects (KRON’s company presentation)

Other candidates that are both orally bioavailable and selective are:

- Atuveciclib (BAY-1143572). There are currently no ongoing trials with atuveciclib according to ICTRP Search Portal. One disadvantage of atuveciclib is on-target neutropenia, which was attributed to the daily dosing regimen, resulting in persistent on-target inhibition of MCL-1 in circulating white blood cells. This has led to the development of VIP152 which is more potent, more selective, is administered intravenously and has a short half-life. This allows once weekly dosing, which results in an “oncogenic shock-like disruption of oncogene transcription, followed by a time without target inhibition needed for the recovery of circulating neutrophils.” This is very different from KRON’s approach (described above) which assumes better efficacy with longer time above therapeutic threshold. KRON can achieve this because of a higher therapeutic index for KB-0742. So far, neutropenia does not seem to be a serious issue with KB-0742 (“No grade 3/4 neutropenia has been observed at doses up to 80mg 3 days on/4 days off per week”), although it could be an issue in higher dosing cohorts.

- CDDD11-8. No clinical trials have been conducted so far.

To my knowledge (based on the list of molecules described in above-mentioned publications), other orally bioavailable CDK9 inhibitors (e.g. TP-1287- oral prodrug of alvocidib, zotiraciclib/TG-02, roniciclib, AZD5438, dinaciclib, fadraciclib/CYC065, GFH009/SLS009, seliciclib/CYC202/R-roscvitine, voruciclib) are less selective (a common issue with small orally bioavailable molecules) which results in off-target side effects. Therefore, KB-0742 does not yet face much competition from alternative oral CDK9 inhibitors, while the rest of CDK9 inhibitors under development are administered intravenously.

Summary of reasons for being bullish for KB-0742

To sum up, I believe KB-0742 will be successful for the following reasons:

- Highly selective (= lower off-target toxicity).

- Oral bioavailability (= preferable by both patients and healthcare systems vs. intravenous administration).

- Single-agent activity in preclinical tumor models.

- Single-agent activity in TF-fusion tumors in humans.

- According to KRON’s hypothesis, even better antitumor responses are to be expected from the higher dosing regimens.

- Potentially large target patient population.

KB-0742 potential (KRON’s company presentation)

KB-9558

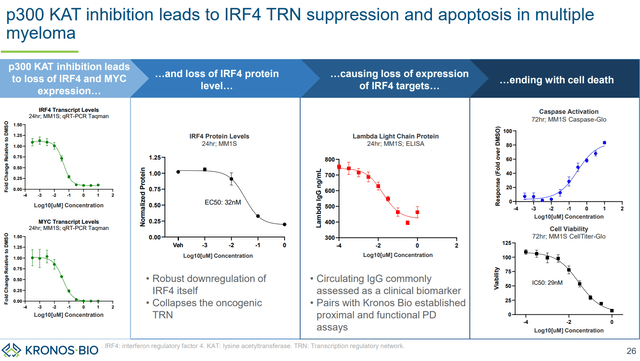

Beyond KB-0742, KRON is also developing KB-9558, a p300 KAT inhibitor. p300 is a key regulator of IRF4 TF, which is a key driver of multiple myeloma. There is strong scientific rationale for targeting IRF4:

- “IRF4 dependency is universal across multiple myeloma cell types”. Furthermore, “this dependency is maintained regardless of prior treatment or therapy resistance suggesting potential clinical benefit across multiple prior treatment regimens and contexts.” In other words, IRF4 inhibition is expected to be effective in most multiple myeloma patients, irrespectively of prior treatments.

- “Downregulation of IRF4 is not only highly potent against multiple myeloma, but also highly context specific vs. other cell lines and tissue types.” In other words, selective inhibition of IRF4 is expected to be well tolerated.

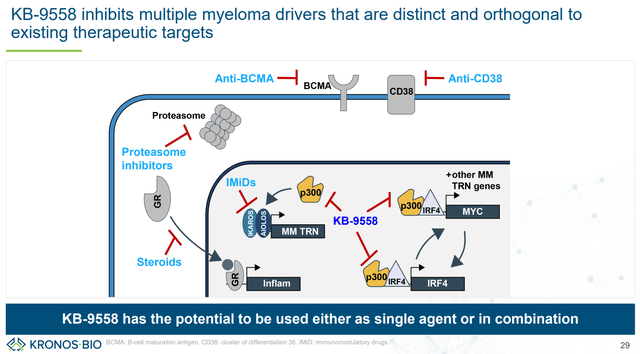

Despite strong scientific rational, directly targeting IRF4 is challenging because IRF4 lacks “amenable ligandable pockets for small molecule perturbation.” By using its discovery platform, KRON identified p300 as a critical node (i.e., selective inhibition of IRF4 is possible by targeting p300). Specifically, KAT domain of p300 was identified as most relevant for selective IRF4 inhibition. This contrasts current clinical approached that target its bromodomain (an approach that is not as effective for IRF4 downregulation). The point of the above paragraphs is to demonstrate the advantages and potential of KRON’s discovery platform.

Based on the above research, KRON developed KB-9558,

“an orally bioavailable small molecule with excellent pharmacological properties, no significant off target activity, and minimal potential for drug-drug interactions.”

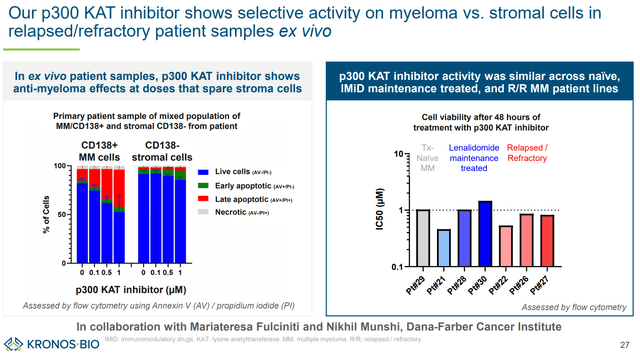

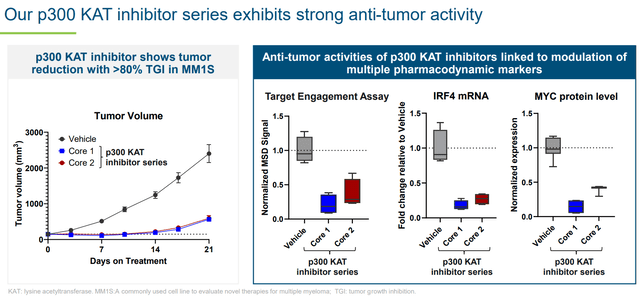

KB-9558 has shown selectivity (sparing stromal cells vs multiple myeloma cells) and strong preclinical antitumor activity. Furthermore, based on distinct mechanism of action and activity regardless of resistance to other therapies, KB-9558 has the potential to be used both as monotherapy (in patients refractory to existing therapies), as well as in combination with existing therapies for earlier line patients. KRON plans to initiate a first-in-human trial in 1H 2025.

p300 KAT inhibition induces apoptosis in multiple myeloma cells (KRON’s company presentation)

KB-9558 spares stromal (vs MM cells) and retains activity regardless of resistance to other therapies (KRON’s company presentation)

Strong antitumor activity (KRON’s company presentation)

Distinct mechanism of action allows use both as monotherapy (where other treatments have failed) and as combination (KRON’s company presentation)

Rest of the pipeline

KRON is also developing other undisclosed candidates targeting other transcription regulatory networks, including the collaboration with Genentech.

According to this agreement, Kronos and Genentech:

“have agreed to initially collaborate on two discovery research programs in oncology, each focused on a designated transcription factor.”

Kronos will lead discovery and research activities using its proprietary drug discovery platform. This includes two phases: (1) a mapping phase to characterize the transcription regulatory network of interest, and (2) a screening phase to identify hits suitable for further preclinical development. Following completion of these phases, Genentech has the right to pursue further preclinical and clinical development, in which case KRON will be eligible to receive preclinical/clinical/regulatory milestones up to $170M per “Hit Program” (i.e., total potential $340M if there are two “Hit Programs”), and sales milestones up to $100M (i.e., total potential $200M if there are two “Hit Program”). Furthermore, KRON will be eligible to receive tiered royalties in the low- to high-single digits. KRON has up to 24 months to complete the discovery research programs (i.e., up to January 2025), which may be extended up to 6 months.

KRON’s pipeline (KRON’s website)

Financials

KRON ended 2023 with $175.0 million in cash, cash equivalents and investments. Operating expenses in Q4 2024 were $29.6M (R&D $18.7M, G&A $10.9M), corresponding to a monthly cash burn of about $9.9M. Based on available cash and assuming similar cash burn going forward, the estimated cash runway is about 18 months. However, following restructurings and resource optimization, KRON estimates a cash runway into H2 2026.

Risk factors

Below is a summary of the main risks:

- ASCO update may be underwhelming (abstracts will be released May 23). The most important will be the update from the expansion cohort (expected H1 2025).

- KRON’s hypothesis for KB-0742 (better efficacy to be expected from longer therapeutic concentrations) may be wrong and alternative approaches employing short-lived intravenous CDK9 inhibition may be more effective and/or more tolerable.

- KRON currently has only one clinical-stage asset and one preclinical asset nearing the clinic. Therefore, KRON is lots of years away (if ever) from potential commercialization of one of its assets. This means that KRON will eventually need to raise a lot more cash, unless a partnership-based business model is used (with already one such collaboration ongoing) or a buyout happens during early stages of clinical development.

- There is a risk that Genentech collaboration may never proceed to the clinic (“Kronos Bio will lead discovery and research activities to a defined preclinical point when Genentech will have the exclusive right to pursue further preclinical and clinical development and commercialization”).

Conclusion

I believe KRON’s potential is underestimated by the market, as KRON is currently trading at a negative enterprise value and is well funded for a couple more years. Potential short-term value drivers for KRON are (1) Clinical updates from the ongoing ph1/2 trial (in ASCO and in 1h 2025), (2) Progress on Genentech collaboration, (3) News on more partnerships (speculative). Long term it may be worth investing in KRON for its drug discovery platform, Genentech collaboration validating big pharma interest. Of course, as with every early-stage biotech, there is very high risk and volatility should be expected.

Your feedback is appreciated

Please comment below if you have any feedback (positive or negative), if you spot any mistakes, or if you believe I missed something important in my analysis.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

")

")

")