")

")

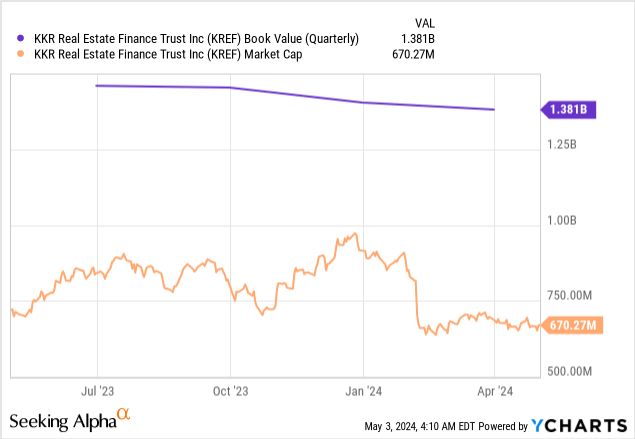

KKR Real Estate Finance Trust’s (NYSE:KREF) book value as of the end of its recent fiscal 2024 first quarter came in at $1.38 billion, $15.18 per share, and dipping by 34 cents sequentially. The continued dip in book value has essentially cratered investor sentiment in the real estate lender and opened a material gap to its book value of 51%. KREF’s CECL allowance also increased to $3.54 per share from $3.06 per share in the prior fourth quarter with the mREIT last declaring a quarterly cash dividend of $0.25 per share, a material 41.9% decline from its prior distribution and $1 per share annualized for a 10.3% dividend yield. The cut was brutal but means a moderation of a vicarious dip in book value since the Fed embarked on its ongoing fight against inflation.

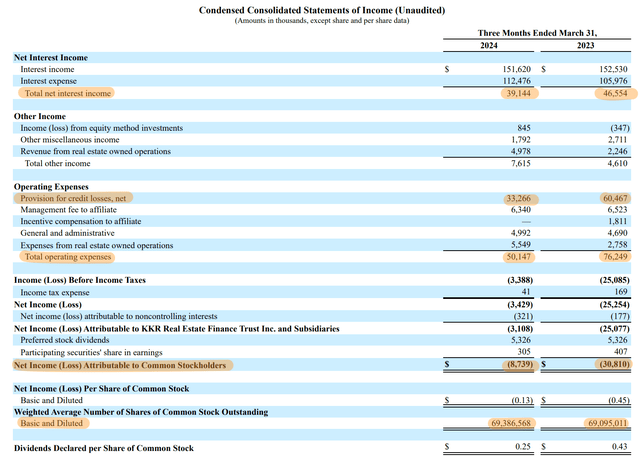

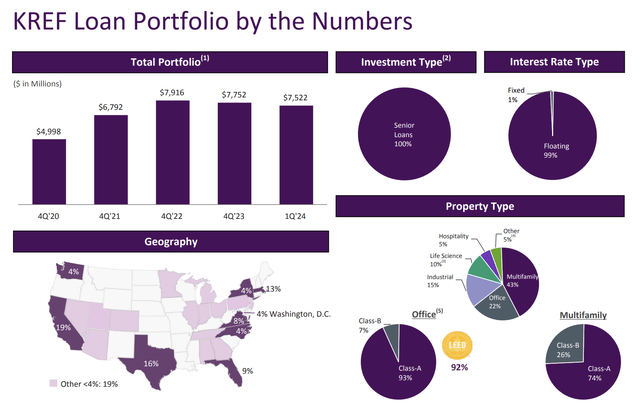

Is KREF a buy? That’s not clear. During the first quarter, the mREIT generated a GAAP net loss of $8.7 million, or $0.13 per share. However, this was a material improvement from a net loss of $30.8 million, $0.45 per share, a year ago. KREF’s operating expenses during the quarter included a $33.27 million provision for credit losses, down from $60.47 million a year ago, but came as total net interest income at $39.14 million dipped 16% from its year-ago comp with KREF pushing through a broad reduction of its overall loan portfolio against the headwinds of office real estate which constituted 22% of its $7.52 billion senior loan portfolio at the end of the first quarter.

KKR Real Estate Finance Trust Fiscal 2024 First Quarter Form 10-Q

Loan Portfolio, Credit Quality, And Originations

KKR Real Estate Finance Trust Fiscal 2024 First Quarter Form 10-Q

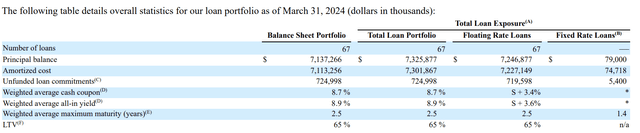

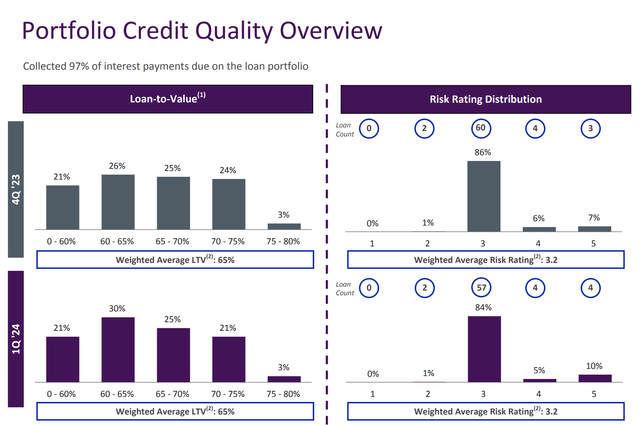

KREF’s portfolio had a weighted average unlevered all-in yield of 8.9% at the end of the first quarter, with a weighted average loan-to-value of 65%. The all-in yield dipped by 10 basis points sequentially, with the weighted average maximum maturity standing at 2.5 years. KREF collected 97% of interest payments due in the quarter, down sequentially from a 98% interest collection rate. A 100 basis points dip quarter-over-quarter is not immaterial, but KREF’s weighted average risk rating of 3.2 was unchanged sequentially.

KKR Real Estate Finance Trust Fiscal 2024 First Quarter Supplemental

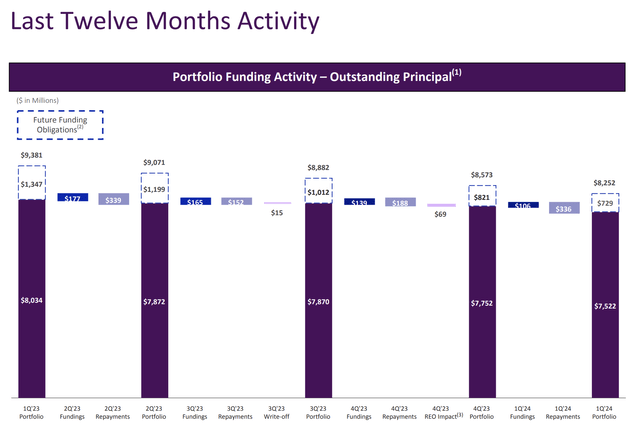

Multifamily properties constituted 43% of KREF’s loan portfolio, with the mREIT receiving $336 million in loan repayments in the first quarter. Industrial properties and life science at 15% and 10% of the loan portfolio respectively, also highlight KREF’s broad diversification despite the headwinds being faced by office from work-from-home trends. The mREIT is essentially in a phase of consolidation, with repayments being allowed to run ahead of originations as KREF moves to manage one of the most disruptive periods for real estate lenders in a generation.

KKR Real Estate Finance Trust Fiscal 2024 First Quarter Supplemental

There was $106 million in new loan funding during the first quarter, with net repayments of $230 million. KREF generated distributable earnings of $26.7 million, $0.39 per share, during the first quarter. This meant a substantial 156% coverage of the reduced dividend and a 64% payout ratio, which ensures the safety of the double-digit 10.3% dividend yield. The mREIT’s first quarter credit quality averages were broadly unchanged versus its fourth quarter, but loans with a risk rating of 5 jumped by 300 basis points.

KKR Real Estate Finance Trust Fiscal 2024 First Quarter Supplemental

Watch List Migrations, Risk, And The Preferreds

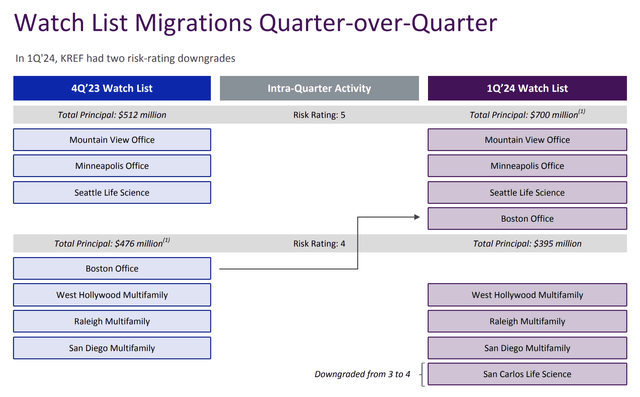

KREF had two risk rating downgrades during the quarter with a Boston office loan with a risk rating of 4 downgraded to 5 and a San Carlos life science loan downgraded from 3 to 4. The mREIT does not think it will need to migrate any more office properties to its watch list. Aggregate CECL reserves were $246 million with roughly $165 million of equity held in Real Estate Owned (REO) properties.

KKR Real Estate Finance Trust Fiscal 2024 First Quarter Supplemental

The definitive KREF play remains the mREIT’s 6.50% Series A preferreds (NYSE:KREF.PR.A) which pay an 8.8% yield on cost but are trading at a substantial 25% discount to their $25 per share liquidation value. This undervaluation comes especially against KREF’s liquidity. The mREIT held $107 million in cash on hand and $450 million in its undrawn corporate revolver capacity as of the end of the first quarter. I’ve been buying more of the preferreds in recent weeks with their total $5.3 million of required payments per quarter covered 5x by distributable earnings. The core risk for both the commons and preferreds remains sticky inflation disrupting the timeline for Fed rate cuts with expectations being for both the discounts on the commons and preferreds to begin to tighten once the Fed begins to start cutting rates.

")

")