")

")

Editor’s note: Seeking Alpha is proud to welcome Tomas Cverna as a new contributing analyst. You can become one too! Share your best investment idea by submitting your article for review to our editors. Get published, earn money, and unlock exclusive SA Premium access. Click here to find out more »

Investment Thesis

As part of the change in the Private Equity division’s strategy, KKR & Co. Inc. (NYSE:KKR) has come up with the concept of long-term value creation and is counting on a higher dividend yield from projects. I think the promise of dividends in PE projects provides the opportunity to increase the leverage of the projects, while the dividend will be a tool to offset initial losses for fund investors. The company’s excellent position in the Japanese insurance market is also contributing significantly to its growth. The short-term tailwind is increased M&A activity in late 2023 and early 2024. KKR is currently trading at a lower forward P/E and P/B compared to peers, but the forward price-to-fee-related earnings ratio (P/FRE) is above the seven-year average.

About KKR

KKR is one of the oldest and best known alternative investment managers. KKR has diversified sources of income, including primarily fund entry fees, performance fees, as well as income from investment divestitures, dividends from companies in its Private Equity division and interest on debt securities. KKR’s funds operate on a limited partnership basis. KKR is the general partner of its funds and the externally qualified investors are limited partners. KKR’s ownership interest in the funds ranges from 8% to 10%. In addition, KKR controls an insurance company, Global Atlantic, of which it is the sole asset manager. Through this insurance company, KKR invests primarily in the bond markets and also in alternative investment funds.

Investors Day

KKR announced very ambitious long-term goals on Investors Day on April 10, 2024. Management expects Adj. EPS to double from current level by 2026 in the range of $7.00 to $8.00 per share. Over a 10-year horizon, Adj. EPS will reach $15, almost 5 times the current value. KKR aims to earn more than $300 million in dividend income by 2026. Then, in 2028, it expects $600 million in dividend income. Fee-related earnings per share are then expected to reach USD 4.5 in 2026, up from USD 2.68 in 2023. I think KKR’s 2026 net profit guidance is achievable and is more or less based on market consensus. Fee-Related Earnings, which are derived from Fee-Related Assets Under Management, will play the biggest role in the net profit trend. I believe that management is also counting on improving market conditions to cause asset prices in the funds to rise, and with it, performance fees, which will increase the FRE margin. On the other hand, the risk is the Fed, which with higher rates for a longer period of time will throttle inflows into the funds and also the asset performance itself.

Interest rates won’t go down just like that

Inflation in the US appears to be more sticky than it might seem at the end of 2023. The market is currently pricing in a maximum of 2 rate cuts by the end of the year, and I think the first one won’t happen until September due to still high inflation and a tight labor market. Higher rates for longer are more of a negative for KKR, mainly due to the higher impact on Private Equity fundraising, which is already under pressure. On the other hand, I believe the Credit strategy will maintain its upward momentum – especially Private Credit, which includes Direct Lending and Asset-Based Finance. Potential defaults on High Yield bonds will not play a key role due to the outflow trend from KKR’s portfolio.

Private Equity

KKR’s Private Equity strategy is about to change. Taking inspiration from Warren Buffett’s Berkshire Hathaway conglomerate, KKR wants to extend the holding horizon of Private Equity investments for dividend income. I expect KKR to operate with more leverage in its Private Equity funds. In fact, the commitment to pay dividends from private equity may be part of balance sheet optimization in the later stages of PE projects, as managers work with higher leverage at the beginning of projects and then optimize initial costs. Dividend investors look for regular payouts, among other things, to cover losses when markets fall. In the case of Private Equity, this is a minor aspect because historically, due to the absence of retail investors in PE, drawdowns have been lower.

Drivers of growth

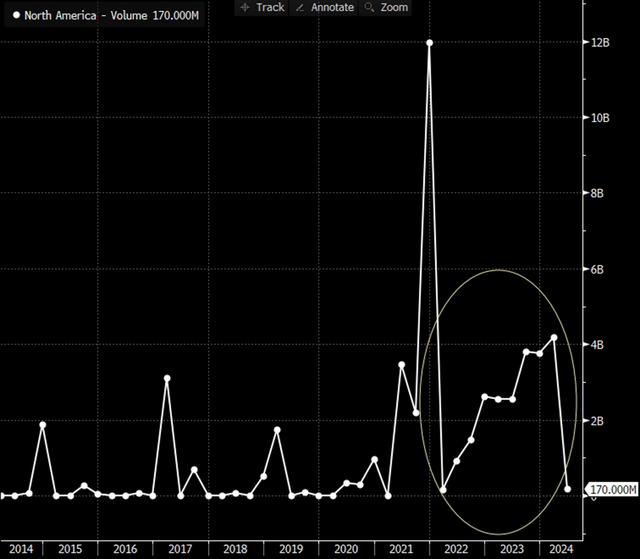

This year, central banks oversee fundraising growth. The pace of fundraising has slowed significantly due to high interest rates. I believe that already in the second half of this year there will be an acceleration not only in the pace of inflows but also in deal activity. However, in terms of mergers and acquisitions made, KKR has been proactive. While deal value in the US has been declining since the end of 4Q2021, KKR has bucked the trend with its proactive approach and gradually increased the volume invested. The decline between the end of 1Q 2024 and 2Q 2024 is due to lack of data, which will be replenished at the end of 2Q2024. In my view, the increasing M&A activity will feed through to the 2024 investment result, offsetting the slowdown from management fees due to the decline in fundraising pace.

KKR’s activity in M&A. Source: Bloomberg Finance L.P.

In the long term, the Asia-Pacific region will be critical to KKR’s success. It is this market that is growing the fastest thanks to Japan, where KKR operates through its funds, but primarily through its Global Atlantic insurance company.

Japan’s life insurance market is specific not only because of its aging population, but also because 90% of households are part of a life insurance program. This is higher than in the US, where the ratio is 70%, and in the UK, for example, with 38%. In addition, the Japanese market is well penetrated by domestic companies, and there are fewer foreign entities operating in this market compared to the US. This gives KKR the opportunity to participate in a market where there is great potential and little foreign competition. Of note is the cooperation with Japan Post Insurance (OTCPK:JPPIF), the second-largest Japanese insurer, and Manulife Japan, which makes Global Atlantic a reinsurer.

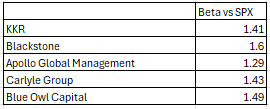

Volatility of shares

Shares of alternative investment managers are highly volatile compared to the S&P 500 equity benchmark.

Beta (β) indicator. Source: Bloomberg Finance L.P.

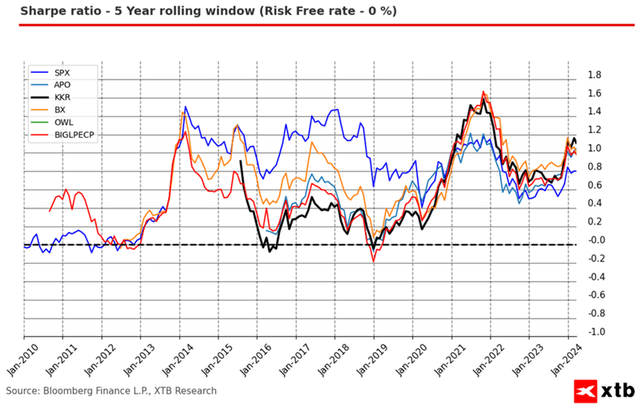

Despite the high volatility, shares of alternative fund managers delivered relatively high returns. In the example below, we calculate a 0% Risk Free rate for the shares of alternative investment managers. The stocks compared were KKR, Apollo Global Management (APO), Blackstone (BX), Blue Owl Capital (OWL), the S&P 500 (SPX) and the Bloomberg Intelligence Global Private Equity Managers Index.

Sharpe ratio. Source: Bloomberg Finance L.P., XTB Research

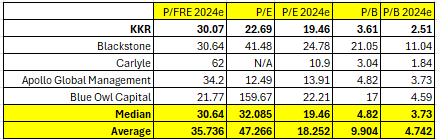

Valuation multiples

Although KKR shares have risen by approximately 15% since the beginning of the year, their valuation is not high compared to peers. However, the P/FRE ratio is now above the seven-year average of 21.48x, indicating a historical overvaluation of the stock. However, the valuation is not very high compared to peers.

KKR stock is trading cheaper than shares of the largest alternative investment manager, Blackstone. Blackstone trades at a premium because it is the only one of the benchmark companies included in the S&P 500 index. This helps investor interest in the stock and boosts valuations. Not only Blackstone, but most of the peer companies are expected to see their valuation multiple decline this year due to valuation catching up with earnings. In the case of Carlyle (CG), the expected valuation P/E and P/B multiple is lower this year due to the low FRE margin, which is a component of valuation (37% Carlyle vs 62% KKR). KKR shares, like Blue Owl Capital, are trading at reasonable forward levels.

Valuation multiples. Source: Bloomberg Finance L.P., Author’s research

Risks

The general risk is the current outlook for rate cuts in the US. Higher rates by the end of the year may not only negatively impact inflows into alternative investments, but also result in a decline in fund performance, which will feed through into performance fees and thus FRE margin. A risk to the investment thesis in the Japanese market is the decline in households enrolled in insurance programs. A longer-term threat is the expanding influence of foreign reinsurers in Japan.

Conclusion

KKR is a quality asset management firm operating in the alternative capital space with diversified sources of capital management fees. At the end of last year, KKR acquired the remaining 37% stake in Global Atlantic, which, I believe, is the main growth driver in the Japanese market. In the short term, the risk is that the Fed keeps interest rates at higher levels until the autumn of 2024. Tight monetary conditions will, in fact, limit deal activity along with fundraising in the Private Equity market, which is key for KKR. KKR shares are now trading at a premium to historical levels; however, forward ratios are at a lower level compared to peers. I therefore recommend a Buy on KKR.

")