")

")

Shares of KB Home (NYSE:KBH) have been a strong performer over the past year, rising over 50% as the housing market has held in better than many feared, despite elevated interest rates. Still, shares have fallen 10% from their recent high as long-term yields have moved higher again. Back in January, after being a long-time bull, I downgraded shares to hold, expecting market-like returns, and since this, shares have returned 4% vs. the 5% S&P 500 rally. KB has continued to report strong results, but concerns about the macro environment are increasing, leaving shares in a tricky position.

Seeking Alpha

In the company’s first quarter reported on March 20th, KBH earned $1.76, beating estimates by $0.19. I would note Q1 ended on February 29th, before the most recent uptick in interest rates, which created the risk that trends the company was seeing could be moderating. Revenue rose by 6% to $1.46 billion, while deliveries increased 9% to 3,037. The average selling price was down 3% to $480k. This was also down 2% from Q4 levels.

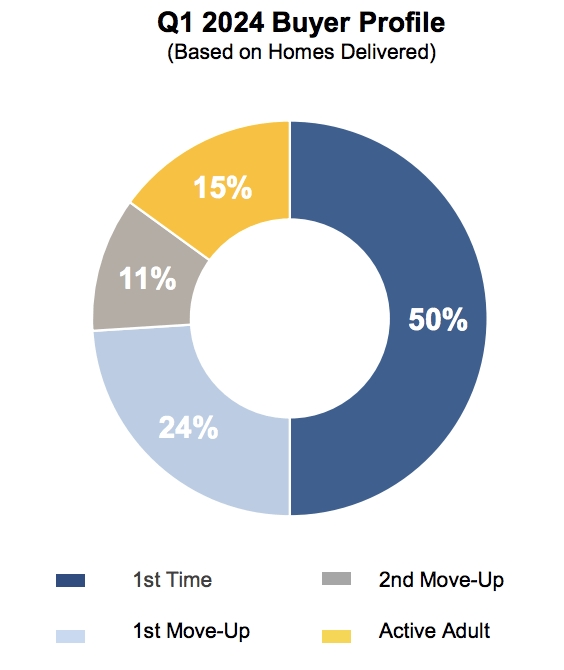

KB’s price point remains at the lower-end of the major homebuilders. That is because the company primarily caters to first-time homebuyers, who generally have smaller budgets than those upgrading their home. These buyers can also be more interest-rate sensitive, as many “stretch” in order to afford the monthly payment, with the aim of growing into their mortgage payment as their careers progress and salaries rise. As you can see, half of KB Home’s buyers are first-time buyers and another 24% are making their first trade up. This customer base is a reason KB can trade at lower multiples than peers like Toll Brothers (TOL) as its buyer base is likely to be more economically sensitive.

KB Home

Still, this buyer base has not shown a sign of weakening. Net orders of 3,323 were about 1.1x deliveries. Last year when orders were weak, KB and other builders delivered homes out of their backlog, which is why it is down from last year by 17% to 5,800 homes. Because the book-to-bill ratio was above 1x, the backlog did rise $125 million sequentially to $2.8 billion. Overall, orders rose 58% from last year, suggesting buyers have acclimated to higher rates after the shock of how much rates had risen last year.

Even with a lower selling price, volume growth and supply chain improvements are assisting gross margins, which improved 80bp sequentially to 21.6%. This was offset by SG&A expense, which rose by 70bp from last year and 90bp sequentially to 10.8%. This is a multiyear-high. This growth in SG&A offset rising gross margins. So while, homebuilding operating income was up 1% to $157.7 million, margins contracted 80bp from last year to 10.9% – they were flat from Q4 levels.

SG&A expense is somewhat higher because after working through its backlog last year, KBH has gone back onto a more aggressive, growth-oriented footing. It now has 55,509 lots owned or controlled with an inventory of $5.24 billion, up 2% sequentially. 72% of lots are owned outright. In Q1, KBH invested $587 million in land, up 60% from a year ago. KBH has more than enough lots to fill demand through the end of next year, but it is adding to its land portfolio, to create a longer runway for growth.

I see positives and negatives to this strategy. On the upside, if the rising demand, which management saw in Q1 and was sustained into March, persists, KBH will have the lots to meet this demand, growing deliveries and cash flow. On the flip side, if demand declines due to higher rates, KBH will have more land than it needs and would have been better having retained cash flow for capital returns.

I think it is critical to note that KBH is funding these investments out of operating cash flow and not via debt, which reduces the risk of this strategy. It has just a 30.4% debt to capital ratio, down 9% over the past two years. Its first maturity is not until 2026, limiting refinancing risk, and it has generated $1 billion of free cash flow over the past year. I expect free cash flow to fall toward $500 million this year as KBH pivots from inventory reduction to inventory growth. Still, this investment is crowding out other uses of cash flow. Notably, it did just $50 million in Q1 buybacks.

Now, last week on April 18th, KBH raised its dividend by 25%, shares now have a 1.5% dividend yield. Alongside this, it announced a $1 billion buyback authorization. However, this is really a multiyear plan, as the company aims to do $200-$400 million this year, which would reduce the share count by 4-8%. Absent the high level of growth investment, buybacks could be $400-550 million.

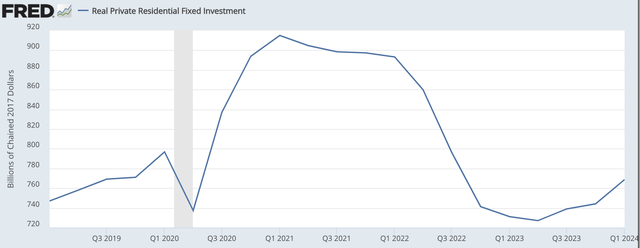

I would note that KBH is not the only builder returning to growth, Real residential investment rose at a 13.9% pace in Q1, the fastest quarterly growth since 2020, according to the latest GDP report on Thursday morning. We are still well below post-COVID highs, but it appears the bottom is in. Increased construction activity does have the potential to increase supply and reduce prices.

St. Louis Federal Reserve

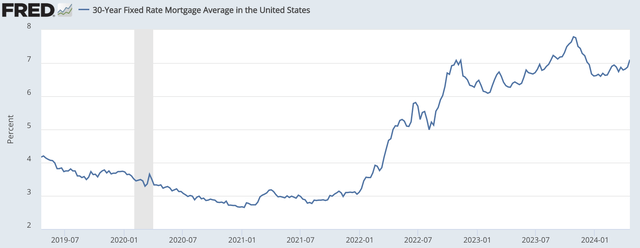

Most new construction/investment decisions are made weeks or months in advance, and it is important to note the rate environment has changed considerably. At the start of the year, markets expected the Federal Reserve to cut rates ~6 times this year. Now, it looks like 0-2 cuts is the central case. As such, rather than continue to fall, as many expected, mortgage rates have moved back higher, above 7% again. As I have written about in past articles on KBH and the builders, I believe the US housing market is fundamentally under-supplied, which is why even with higher rates, I do not see demand collapsing. However, I am not confident we can see demand continue to rise with rates so high, particularly given KBH’s first-time buyer orientation.

St. Louis Federal Reserve

Now, just in March, KBH raised guidance. It sees $6.5-$6.9 billion in revenue with an average selling price of $480-490k and a 10.9-11.3% operating margin. This is slightly above the $6.4-6.8 billion in sales at an 11% margin that the company previously guided to. This outlook does assume a moderating rate environment. Of course, interest rates are volatile, and they could moderate later, but for now, the rate environment is not cooperating. Accordingly, I do have some concern that KBH was too aggressive in lifting guidance. We may see supply weigh on prices, which could also keep margins from expanding.

Back in January, I argued the company had about $7.25 in earnings power. Q1 was a bit stronger than I expected, and the growth in the backlog does provide a cushion for Q2-Q3 results, and so revenue should rise sequentially to at least $1.6 billion in Q2. I, however, am not yet modelling in a faster acceleration in H2. Whereas guidance implies EPS of $7.75-$8.00, depending on the magnitude of buybacks, I see EPS closer to $7.40, higher than previously, but lower than guidance given my concern demand could stall.

Shares appear to be factoring in some downside risk to estimates, as at my $7.40, the stock has just an 8.5x P/E. In this rate environment, I believe shares are likely to struggle past 10x earnings, which has been a ceiling in recent years, as investors price in a risk of a downturn in housing. At the midpoint of its share buyback target, KBH does offer a capital return yield of about 7.6-8%, which should provide a floor under shares. At 9-10x earnings, shares can rally back to about $70. This provides about a ~10% total return opportunity, right on the threshold for moving shares back to a buy.

For now though, I am maintaining a hold recommendation, as given the momentum in rates, I fear rate-sensitive stocks, like homebuilders, will face pressure, particularly with housing supply increasing. If the 10-year treasury returns to 5%, I would expect KBH to trade weaker. While we are nearing a point where it makes sense to buy back into KBH, a better opportunity may present itself. I would look to add shares closer to $60, providing a ~15-20% upside opportunity, given the rate risk. KBH is getting interesting, but given its focus on growth, there could be a better time to buy.

")