Co-authored by Treading Softly.

Many people are fascinated by the luxuries and lifestyles of celebrities. Numerous media outlets, such as TV shows, award ceremonies, and magazines, are dedicated to documenting their every move. What often fascinates us about them is their complete disconnect from the standard reality of the working American. The vast majority of these individuals have a very high net worth and a high level of income that they don’t understand the everyday struggles that you, or I, go through. These top 1% of income earners can often feel like they live in an unimaginable ivory tower. Yet, the average high-income earner, an individual who earns $500,000 or more annually, typically has about $2.68-$3 million saved towards retirement. This means that the vast majority of them have about 5 times more in their retirement account than the average American, who retires with an average savings of $537,000.

If we apply the golden rule of retirement planning and use the 4% withdrawal rule, that individual who has $3 million in their retirement account would retire with about $120,000 annually from their portfolio. Comparatively, if we were to use our unique income method and apply the principles found therein (we can use these two examples we provided you with today) to earn an excess of 13% yields from your money. For instance, if you had $1,000,000 in your retirement account, you could retire on $130,000 a year, outperforming many from the top 1% of income earners within the United States. This means that you can hypothetically join the 1% in their retirement by using simple tools to elevate your earnings to higher levels. While there is often more risk involved in taking on a higher yield, careful application of fundamental research on the securities and adequately diversifying will reduce that risk considerably.

Let’s take a look at two great ideas today!

Pick #1: XFLT – Yield 14.6%

XAI Octagon Floating Rate & Alternative Income Trust (XFLT) has been a fantastic investment for income investors. However, if you are the kind of investor who is looking for share prices that rocket up and “beat” the market with unrealized gains, XFLT isn’t for you, nor is any other CEF (Closed-End Fund) for that matter.

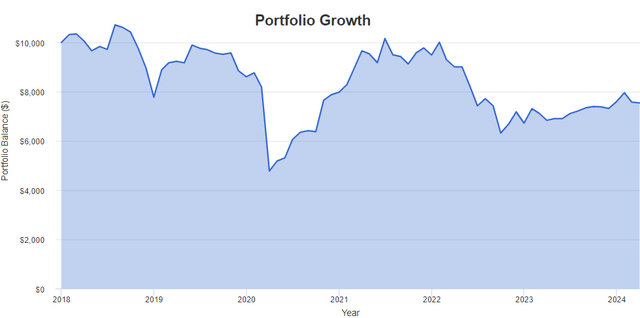

Those who love to stare at charts aren’t going to find much to be excited about XFLT. If you invested $10,000 in January 2018 and withdrew all your dividends, you have seen the value of your principal swing down to about $4,800 during COVID, climb back to slightly over $10,000, and is now down to about $7,500. Source.

Portfolio Visualizer

It’s been a bit of a ride, but there isn’t enough volatility in the price to interest a swing trader. Sure, there are some people who will sit there and tell me, “The way to make money on this is to trade it.” This doesn’t make sense to me because you are going to get a lot bigger swings with growth stocks or crypto.

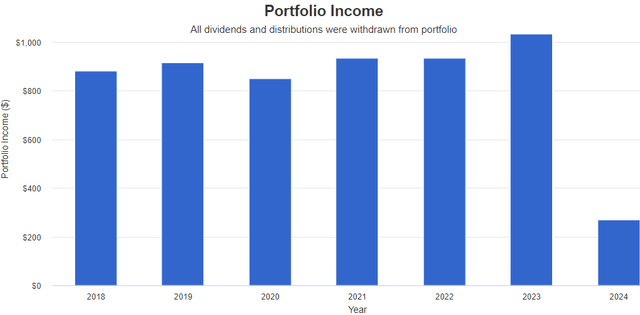

I know a good number of people who would look at this and wonder why anyone in their right mind would buy XFLT. An even larger number will declare that XFLT is “irresponsible” and “risky” because its yield is over 14%. Why do I own XFLT? For the income. Here is the income that XFLT has produced over the years – without reinvesting a single penny:

Portfolio Visualizer

A $10,000 investment in XFLT in January 2018 has produced $5,814 in dividends. That’s cash, in your pocket, that you spent on whatever you felt like spending it on. Maybe you reinvested some of it; perhaps you didn’t. I know, on Wall Street the idea of spending your money is sacrilege. How can you have the highest total return if you dare to spend your own money?!

The best part is that XFLT is paying out the highest dividend it has ever paid. So, in this scenario, despite withdrawing 58% of your original capital, you are on pace to collect more dividends in 2024 than any other year.

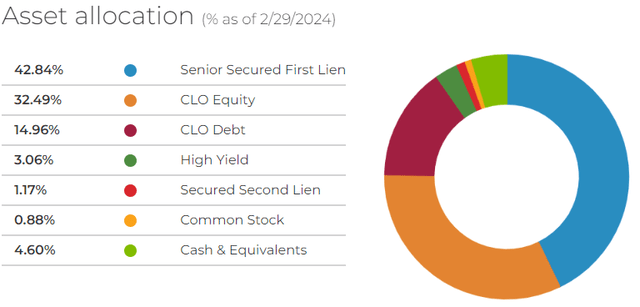

How does XFLT produce so much cash flow? It invests in debt. Specifically, XFLT focuses on “leveraged loans,” which are senior secured loans made by banks to companies that typically fall in the B/B+ credit rating range. XFLT invests in these loans directly, and indirectly through CLOs (Collateralized Loan Obligations). Source.

XFLT Website

CLOs are vehicles that “securitize” debt. The CLO buys up leveraged loans, and then sells the right to collect the cash flow in various tranches that are paid out on a “waterfall” basis. The senior debt tranches get paid first, then the junior tranches, and finally, the equity gets the remaining excess.

Even if borrowers are paying as agreed, the terms for the senior tranches often have numerous protections. For example, if the value of the loan collateral declines, there is a provision to “redirect” payments that would have gone to the equity tranches to prepay the senior debt. This forces the CLO to deleverage and results in a temporary disruption in cash flow to the equity tranche.

During COVID, there was a significant number of CLOs that were redirecting some or even all the payments owed to the equity tranches to prepay senior debt. This drove distribution cuts across the sector, including for XFLT, which cut from $0.073/month to $0.06/month. However, XFLT’s diversification into the debt tranches of CLOs and direct ownership of loans meant that XFLT only had to reduce the distribution for six months. Today, XFLT pays out a dividend of $0.085 – over 16% higher than it paid before COVID.

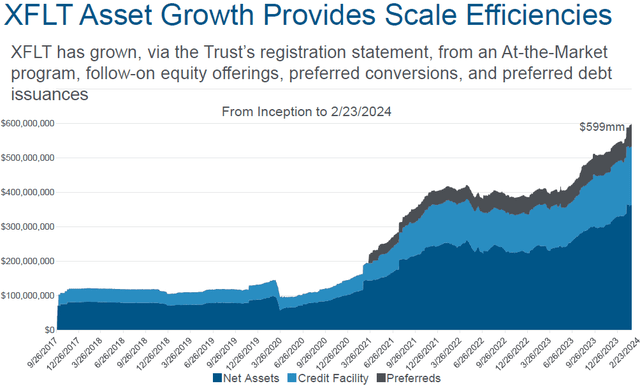

Prices are lower for loans following the Fed’s aggressive hiking cycle, and XFLT hasn’t been immune to that. However, it is paying out more than it ever has. Lower loan prices mean that buyers of loans receive higher yields – XFLT has been buying. Source.

XFLT Q4 2023 Presentation

It is this growth that has driven XFLT’s dividend higher following COVID. The disruption of the debt markets caused by the Fed has created a generational buying opportunity. XFLT is buying loans, and I’m buying XFLT to enjoy even more income pouring into my portfolio!

Pick #2: AWP – Yield 13.1%

Have you ever driven a long distance with a child in the back seat screaming, “Are we there yet?” It’s a classic tantrum that certainly didn’t happen with my parents driving because they would pull over, and nobody would enjoy the outcome of that particular pit stop. But I’ve seen it happen in movies. The impatient child, creating a scene, somehow imagining that their antics would get them home sooner.

The market is throwing that tantrum over rates, and every time the car slows down, it throws another fit. The Fed isn’t going to cut in May? SELL! The Fed isn’t going to cut in June? SELL!

The focus of that selling is everything the market considers “interest rate sensitive,” and REITs fall squarely into the category of interest rate sensitive. abrdn Global Premier Properties Fund (AWP) is a CEF that invests in REITs around the world. It has been directly impacted by the market’s tantrums over rates.

I’m not going to tell you when rates will be cut. I can’t control the Fed, and if the past four years have illustrated anything, it is that if the governors of the Fed read my Market Outlooks, they ignore them.

What I can tell you is that, much like that minivan inching its way through traffic those last few miles, we will eventually get there. Every day, we are a little bit closer. It is inevitable. Interest rates will not be over 5% forever.

So, while the market is in the backseat throwing a fit, I’m sitting in the front enjoying the drive and buying up all the income I can find while it is on sale.

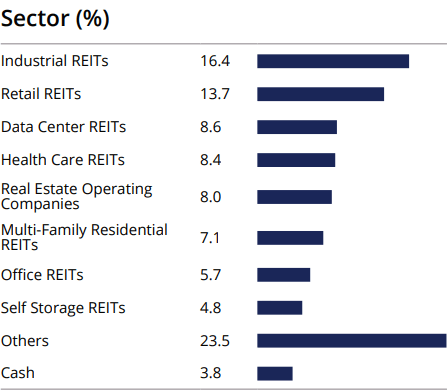

AWP has a diversified portfolio with its highest concentrations in industrial and retail REITs. Source.

AWP Fact Sheet

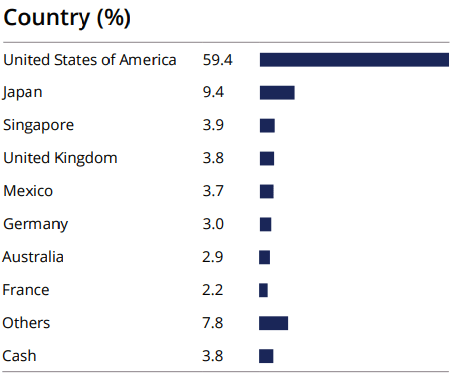

What makes AWP very different from any other REIT-focused funds we hold is its significant non-U.S. exposure. Approximately 60% of its portfolio is in the U.S., and a little over 40% is outside the U.S.

AWP Fact Sheet

AWP’s non-U.S. REITs slightly outperformed its U.S. exposure in 2023, as U.S. REITs have been disproportionately impacted by the uncertainty over when the Federal Reserve will cut rates.

AWP’s price has been trading in the high $3 to low $4 range, and will likely continue to be in that ballpark until there is certainty about when the Fed is cutting. I’m happy to buy up more shares, and buy before this high yield comes down.

Conclusion

With AWP and XFLT, we can leverage the skills and abilities of portfolio managers to enjoy high yields from sectors that can offer considerable value. XFLT provides us with exposure to individual secured loans as well as CLO investments along with a little bit of leverage to provide us with strong income in the present and going forward. With AWP, we get to benefit from quality real estate assets from all over the world. Both CLO investments and real estate investments are proven means to generate long-term wealth, something that the top 1% of income earners or high-net-worth individuals effectively and frequently use. By mirroring their techniques, you’re also able to mirror their retirement lifestyle as far as income is concerned. I don’t expect you to go buy a millionaire mansion in Malibu and try to rub shoulders with the stars of Hollywood. But I do want you to have the retirement that you have always dreamed of.

When it comes to retirement, many of us dream of having less stress and more leisure time. Financial failure is a major reason retirement plans fail. This leads to running out of money or income before your retirement is over, forcing you back into the workforce in your old age. By using our unique Income Method and investing in its quality income investments found across the market, you can vastly reduce the chance of failure, thereby eliminating a massive source of stress in retirement.

That’s the beauty of my Income Method. That’s the beauty of income investing.

")