")

Article Thesis

TORM plc (NASDAQ:TRMD) is a shipping company that offers a gigantic 22% dividend yield right now, based on its most recent quarterly dividend payment. A yield this high is risky, of course, and even though TORM is very profitable right now, the dividend yield is likely not sustainable in the long run. That being said, TORM plc is a well-managed shipping company, and total returns could be attractive even if there is a dividend reduction in the foreseeable future.

Company Overview

TORM plc is a UK-based shipping company that is focused on product tankers. Its ships move products such as diesel or gasoline from one port to another, but they don’t move any crude oil — crude oil tankers have different specifications. TORM’s history dates back to the late 19th century when Captain D. E. Torm founded the company that is still named after him. The company grew in size over the decades and has become more easily investable for US-based investors in 2017 when TORM plc got listed on the NASDAQ. Asset management company Oaktree holds a significant stake of around 47% in TORM plc, meaning the free float is around half as high as TORM’s share count of around 94 million.

At the end of the first quarter, TORM plc had 89 vessels, which was up by a couple of percentage points compared to the previous year’s quarter. Thus, the fleet is growing for now. The company’s fleet size grew further due to the acquisition of another 8 product tankers that was announced in July. The company sold one vessel since its Q1 results had been published. Thus, the vessel count was 96 after accounting for the acquisition of 8 additional vessels and the disposition of one ship when the company announced its Q2 results a couple of weeks ago.

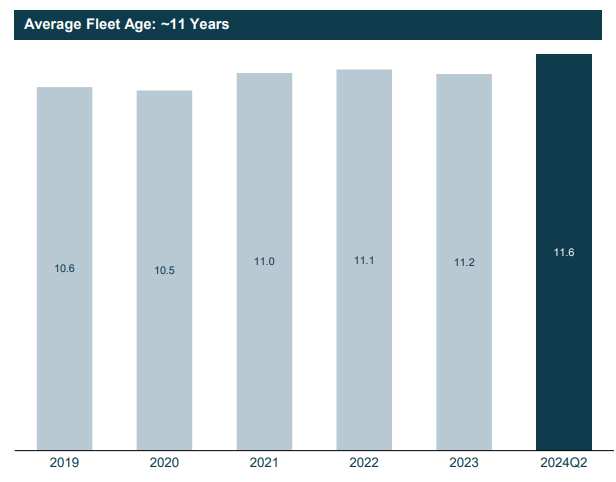

While the size of a company’s fleet matters, the average age of its fleet is important as well. Newer vessels oftentimes have lower operating expenses due to more efficient engines, for example, and they can also demand higher rates in some cases. Importantly, newer vessels also have a longer life span left. Thus, they don’t need replacement in the foreseeable future.

The average age of TORM plc’s vehicles over the last couple of years looks like this:

TORM plc average fleet age over time (TORM plc Q2 results presentation)

The average fleet age has moved up slightly over the last couple of years, and also over the last year, and is now at a solid level of between 11 and 12 years. TORM’s fleet thus is not ultra-new at all, but its ships have still many years left until they will not be useful any longer. Many product tankers are used for 20 years or more, thus TORM’s fleet age is not especially high.

The trend is pointing to a somewhat aging fleet, however. Despite TORM’s decision to sell older ships from time to time while acquiring newer vessels, those efforts have not kept the average age at a constant level. This is not an issue in the near term, but TORM plc will likely have to step up its fleet renewal efforts in the coming years in order to prevent its fleet from aging further.

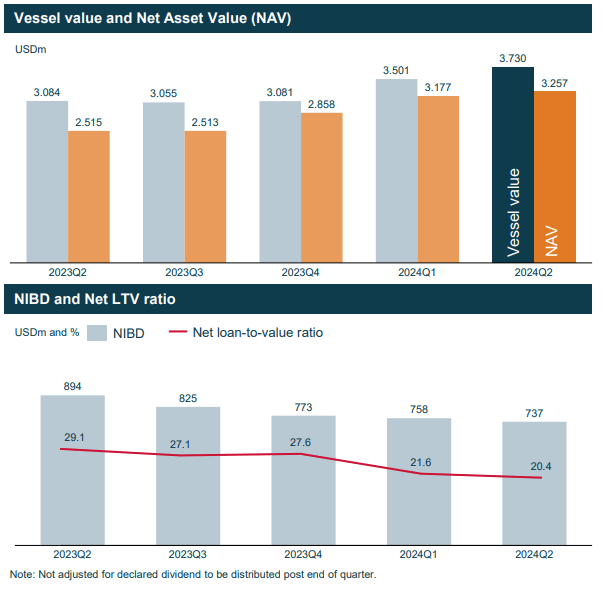

TORM plc should be easily able to do so, as its strong balance sheet gives it considerable financial firepower:

TORM plc’s net asset value and average loan to value (TORM plc Q2 earnings presentation)

We see that TORM plc’s net asset value is relatively close to its gross asset value, due to the fact that TORM’s net debt position is rather small. At the end of the second quarter, TORM had $560 million of cash on its balance sheet, while its long-term debt totaled $1,080 million at the same time. TORM’s net debt thus stood at around $500 million.

On a relative basis, compared to the value of TORM’s ships, debt levels are pretty low as well, as the net loan-to-value ratio stood at just 20% at the end of the most recent quarter. That was down on by 120 base points compared to the previous quarter, and down by a nice 870 base points compared to one year earlier. TORM thus has been deleveraging very successfully in the recent past, which was made possible by strong profitability. The balance sheet is now pretty clean, which is why TORM shouldn’t have any problems in acquiring further (young) vessels to reduce the average age of its fleet.

TORM Benefits From A Strong Market

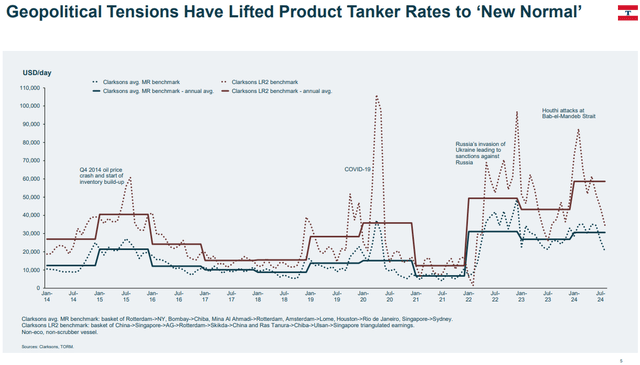

Shipping companies can have famously volatile results, as shipping rates can see substantial ups and downs, depending on what the supply of ships and demand for shipping capacity look like. It is not rare to find shipping companies that report losses during phases when the market is rather weak for the type of ship they own.

TORM plc, as a product tanker company, naturally depends a lot on what rates for product tankers look like. In the recent past, rates have been strong, with geopolitics and unrest being a key factor. The Suez Canal is one of the most important shipping lines in the world, and since the conflict in the Middle East escalated last October when Hamas attacked Israel, Houthis have been attacking ships that traveled through the Suez Canal. On top of that, there is also the ongoing war in Ukraine, which adds to global tensions. In the following chart, we see that these factors have resulted in steep increases in product tanker rates:

Product tanker rates (TORM plc Q2 earnings presentation)

Since early 2022, when the war in Ukraine began, rates have been elevated, and they rose further when the conflict in the Middle East escalated. This has resulted in substantial growth in TORM’s time charter equivalent rates, which rose from around $36,000 in Q2 of 2023 to around $42,000 in Q2 of 2024.

This increase in rates, combined with growth in TORM’s fleet, has boosted the company’s profits nicely. TORM earned $251 million of EBITDA in Q2 2024, up a little more than 25% compared to the previous year’s quarter. TORM’s share count grew over the last year, due to some shares being issued to finance acquisitions, but earnings per share were still up by a nice 17% year-over-year despite the headwind from share count dilution. With $2.08 per share in profits in Q2, TORM’s annualized earnings pace is around $8.30 — for a company that trades at $33 per share right now, that’s excellent, as it pencils out to an earnings multiple of around 4.

It is thus not surprising that TORM plc can offer very nice dividend payments right now. The company’s most recent quarterly dividend payment stood at $1.80 per share, which pencils out to $7.20 on an annual basis. Relative to a share price of $33, that makes for a dividend yield of 22%, or more than 5% per quarter.

Risks And Sustainability Of Dividends

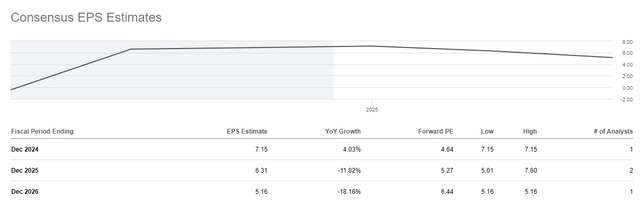

When a company’s dividend yield is as high as that of TORM plc, the market clearly believes that dividends will decline in the long run. And in TORM’s case, that makes sense. Profits are forecasted to peak in 2024, with lower earnings per share being forecasted for 2025 and 2026, looking at the Wall Street analyst consensus estimates for these years:

TORM plc earnings per share estimates (Seeking Alpha)

Profits are forecasted to decline by around 30% by the end of 2026, relative to what is forecasted for this year. And even when we look at this year’s estimate, we see that the analyst community expects a slowdown during H2 — TORM earned $4.40 per share in H1, but the full-year estimate is just a little north of $7, implying that profits in Q3 and Q4 will be well below $2 per share, respectively.

If earnings drop to around $5 per share by 2026, then the current dividend of $7.20 per year is not sustainable. There is, of course, no guarantee that the analyst community is right about lower profits in 2025 and 2026, but it would, I believe, not be a major surprise. After all, the current geopolitical problems will hopefully come to an end, and if tensions in the Middle East ease, then product tanker rates will likely decline.

When it comes to TORM’s profits, geopolitical tensions are “positive”, while waning tensions are “negative” as they will result in lower TCE rates and lower profits, all else equal. Peace in the Middle East and an end to the Suez Canal attacks is thus a “risk” for TORM. There is also the risk that further fleet aging will eventually hurt TORM’s profits, although I believe that the company’s clean balance sheet will give the company the ability to renew its fleet in time.

Is TORM A Buy?

TORM is well-managed, has a sizeable and growing fleet, and a very clean balance sheet. Profits right now are excellent, but they will likely not remain this high forever. The dividend is very high right now, but will likely decline in the coming years.

That being said, even if the dividend were to be cut in half, the yield would still be very strong, at 11%. And considering that TORM trades below net asset value (NAV of $3.3 billion, versus a market capitalization of $3.1 billion), TORM could be a good investment still — investors shouldn’t think that the dividend will always remain this high, however.

")