")

Almost every time that there is a major merger or acquisition in the market, there is bound to be drama. Often, this is on the regulatory side of the equation. However, it can sometimes bleed into the shareholder side. Undoubtedly one of the most controversial transactions currently in progress is the deal by which integrated energy giant Chevron (CVX) will acquire Hess Corporation (NYSE:HES) in a deal valued at $53 billion on an equity value basis and about $60 billion on an enterprise value basis. In addition to the companies facing regulatory scrutiny, there is also a lot of drama on the side of shareholders. This is creating some uncertainty as to whether or not the deal will ultimately be completed.

The good news is that, on May 28th, Hess Corporation’s shareholders are expected to vote on the transaction. But with many major shareholders in the business planning to abstain from the vote, it remains unclear what the end result will be. Normally when a transaction fails, shares of the business that agreed to be acquired would fall, sometimes drastically so. And it is true that Hess Corporation, even today, is pricey compared to some other similar enterprises. But given where the stock was prior to the deal being announced and the high quality of operations today, I actually think that the chance of the stock falling in response to the deal being scuttled is very limited. On the other hand, there does appear to be some upside potential, creating a modest risk to reward opportunity for shareholders to enjoy.

Investors should consider Hess Corporation

Back in late October of 2023, news broke that Chevron would be acquiring Hess Corporation in an all-stock deal valued at about $53 billion on an equity value basis. In exchange for each share of Hess Corporation outstanding, investors would receive 1.025 shares of Chevron. That worked out to roughly $171 per share. At that time, I wrote an article wherein I acknowledged that the market was not happy about the transaction, as evidenced by the fact that shares of both companies fell after the announcement. Even so, I ended up rating Chevron a ‘buy’, citing the quality of the company and talking about the upside potential of the deal, particularly if the $1 billion in planned synergies would come to fruition. Ever since then, however, there has been a lot of drama that has created uncertainty about whether the deal will ultimately be approved.

When the transaction was originally announced, both parties believed that everything would be completed in the first half of the 2024 fiscal year. However, if it does get completed, it will likely be some time past that. During its earnings call transcript for the first quarter of 2024, the management team at Chevron announced that they are continuing to work with the FTC in order to receive regulatory approval. Although nothing is guaranteed, management thinks that this will be concluded by ‘midyear’. So we are likely looking sometime between the beginning of June and the end of July.

Chevron

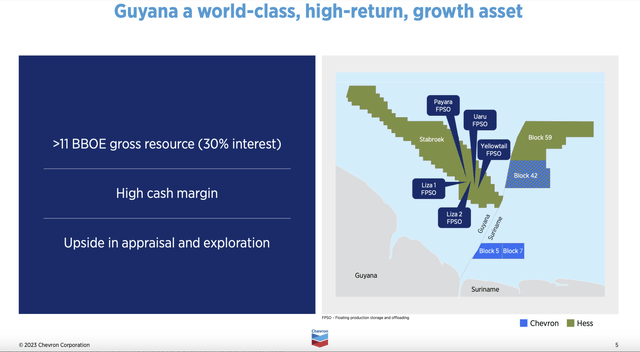

Unfortunately, it’s almost certain that the transaction would not be completed at that point in time. This is because of arbitration that must occur between Hess Corporation and Exxon Mobil (XOM). You see, as of 2022, over 40% of the oil output generated by Hess Corporation came from a joint venture that it has in Guyana. The company has a 30% stake in that asset with estimated reserves of around 11 billion boe (barrels of oil equivalent). But of course, even that number can change. This is because the operator over the 6.6-million-acre Stabroek Block that the company invested in has made over 30 discoveries since 2015. It’s not unthinkable that additional ones could occur as time goes on. And the fact of the matter is that, by 2027, the company believes that the joint venture could result in around 1.2 million boe per day by the year 2027. That’s triple what is currently estimated for the area. The company also has a 20% ownership interest in the operations of the Kaieteur Block.

Regarding the Stabroek Block, Exxon Mobil claims to have a right of first refusal over any change of control. This means that, for any given price that Hess Corporation would sell that stake for, the energy giant has the ability to buy the assets instead. The argument being made by Exxon Mobil is that the purchase of Hess Corporation by Chevron constitutes such a change of control. However, Hess Corporation and Chevron believe that this does not apply to a sale of Hess Corporation in its entirety. I am not an attorney, so I cannot say what the courts will ultimately decide. But given that we are talking about a sale of Hess Corporation as a whole, as opposed to just a sale of its ownership interest in the joint venture, I would have to disagree with Exxon Mobil. Regardless of what ultimately comes to pass here, the CEO of Exxon Mobil, Darren Woods, stated that arbitration is likely to last into 2025.

There are other potential impediments to this deal getting completed. Back in November of last year, 23 senators, led by Chuck Schumer, urged the FTC to investigate not only the purchase of Hess Corporation by Chevron, but also to investigate the acquisition of Pioneer Natural Resources by Exxon Mobil (a deal that closed earlier this month). Concerns center around the possibility of these major oil companies becoming even larger leading to an environment where smaller players cannot adequately compete and where those firms boast unprecedented market power. More recently, earlier this month, Schumer called for the FTC to stop the merger between Chevron and Hess Corporation.

There’s also some pressure from investors regarding whether or not this deal will be completed. On May 20th, for instance, Hess Corporation issued a press release wherein it stated that the independent proxy voting and corporate governance advisory firm, Glass, Lewis & Co, recommended that shareholders vote in favor of the merger. The organization stated that ‘the strategic and financial merits of the proposed merger are sound and reasonable’. It then went on to state that ‘Hess shareholders will have the opportunity to participate in the potential future upside of the combined company’.

However, Glass, Lewis & Co seems to be alone in this regard. Another player in the advisory space, ISS (Institutional Shareholder Services) announced earlier this month that it was recommending that shareholders abstained from voting on the buyout. This was to allow for more time for the details of the arbitration process that I mentioned previously to come to light. Specifically, they stated that ‘investors are presently unable to make an informed assessment’ about the transaction and that voting in favor of it today would prevent investors from considering a more attractive offer.

It does appear as though many investors with sizable stakes in Hess Corporation are following that recommendation. According to reports, DE Shaw which owns 4.38 million shares of Hess Corporation, plans to abstain from the transaction. Another major shareholder, Pentwater Capital Management, also intends to abstain. For context, that hedge fund owns about 4 million shares of Hess Corporation. An even larger player that is planning to abstain from the vote is HBK Capital, which owns 8.32 million shares of the company. Just these three firms combined own 16.7 million shares, or about 5.4% of the enterprise. Other shareholders are also pushing back. On May 21st, news broke that Hess Corporation is now facing three separate lawsuits seeking to delay or block the sale of the company to Chevron on the basis that, allegedly, the company provided inadequate disclosures. It remains to be seen what the end result will be when voting takes place later this month.

Author – SEC EDGAR Data

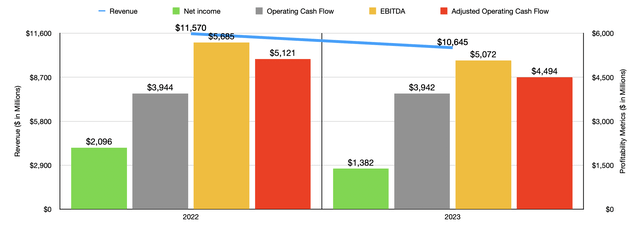

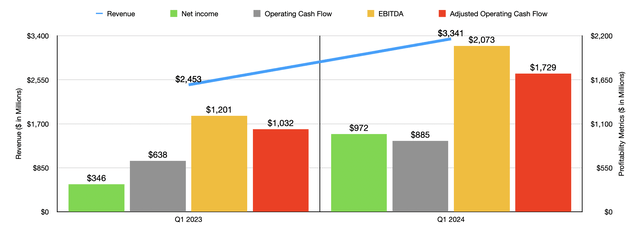

I am not a psychic, so I have no idea what will come to pass. As I mentioned at the start of this article, transactions that fall apart do tend to result in the acquiring company seeing its share price plummet. However, the fact of the matter is that shares were already trading at around where they are today prior to the deal being announced. In fact, they were a bit higher. Shares today are at $154.61. But the day prior to the announcement, they traded at $163.02. Fundamentally speaking, Hess Corporation has been doing quite well as of late. In the chart above, you can see financial performance for the 2022 and 2023 fiscal years. Although 2023 was weaker than 2022 was, the chart below shows robust performance for the first quarter of 2024 compared to the same time of 2023.

Author – SEC EDGAR Data

Obviously, we don’t know what the rest of 2024 will look like. And unfortunately, management has not provided any guidance. But if we use the results from the past two years, we can see how shares are priced as illustrated in the chart below. On a price to earnings basis, Hess Corporation does look quite expensive. But relative to both adjusted operating cash flow and EBITDA, the company is trading at levels that I would consider to be fairly attractive.

Of course, we do run into the issue that shares, while attractive, are pricey compared to similar enterprises. In the table below, you can see what I mean. In each of the three pricing scenarios, Hess Corporation ended up being more expensive than any of the five firms that I decided to compare it to. But as I discussed earlier in this article and provided even more details on in my initial article last October, there is a lot of potential, particularly regarding the assets in Guyana. And it’s likely because of that opportunity that shares are trading, justifiably speaking, at levels above what similarly sized integrated energy companies are going for.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Hess Corporation | 34.6 | 10.6 | 11.1 |

| Diamondback Energy (FANG) | 11.1 | 6.0 | 6.7 |

| Devon Energy (DVN) | 9.5 | 4.8 | 5.1 |

| Coterra Energy (CTRA) | 16.3 | 7.0 | 6.4 |

| EOG Resources (EOG) | 10.2 | 6.8 | 5.5 |

| EQT Corporation (EQT) | 29.8 | 6.4 | 8.6 |

Given everything that we know today, I would peg the probability of the stock falling in response to the deal collapsing as being quite low. But there are two other scenarios where upside could be decent. The first would be if the deal gets approved and is completed as agreed upon. If we assume that shares of Chevron don’t change from where they are today, this would result in upside of about 6.1%. The other scenario is that regulators approve the transaction but shareholders push back enough to force a higher price. It’s unclear whether or not Chevron would be willing to proceed with a higher offer. I would say that the probability of them doing so is definitely comfortably above 50%. Obviously, we have no idea what that kind of upside might look like. But it would certainly be more than the 6.1% we are looking at today.

Takeaway

At this point in time, this is certainly something of a quagmire. However, I view this as an interesting risk to reward opportunity. Unless shares of Chevron fall, I don’t see any meaningful downside to Hess Corporation’s stock if things don’t go as the management teams of both companies plan. But if things do go well, then upside could be anywhere from decent to some unknown number that is quite attractive. Because of this, I’ve decided to rate Hess Corporation a soft ‘buy’ at this point in time.

Q2 2024 Earnings Call Transcript")