")

")

I have been cautious on Green Thumb Industries (OTCQX:GTBIF), and it’s up in 2024, 16.9%. My last article, written in late February, was a downgrade from Neutral to Sell. I warned that the stock was not safe at the time. Despite some great news about the DEA rescheduling cannabis finally hitting the market this past week, the stock is currently down 7.6% since that article. I am upgrading the stock to Neutral.

The DEA Action

Investors have been very excited about the potential rescheduling of cannabis that was rumored to be taking place in late August, when the Department of Health & Human Services recommended that the DEA move cannabis from Schedule 1 to Schedule 3. Many months passed, but on April 30th, the DEA revealed through the media that it was going to do so. It’s still not a done deal, as the White House Office of Budget Management needs to approve it, and there is a mandatory public comment period. This should be wrapped up by year-end, perhaps ahead of the elections in November.

Rescheduling has one huge benefit: If cannabis moves to Schedule 3 (not Schedule 2!), then 280E taxation will end. The 280E tax was devised in the 80s and forces manufacturers or sellers of Schedule 1 or Schedule 2 drugs to pay taxes on gross income rather than net income. The inability to deduct ordinary business expenses was supposed to prevent drug dealers from operating. It has led to the income tax rates being very high for American cannabis companies. In fact, even with operating losses, taxes are owed.

I have been publicly proclaiming for more than a year how essential it is that 280E go away. The removal of that tax will reduce taxes and improve operating cash flow. The cannabis industry analysts provide stock price targets based on adjusted EBITDA, which will not be impacted at all. Net income, though, will improve.

There may be other benefits to cannabis being rescheduled, but there could be negatives too. The one that I think is scary is that the FDA could begin to regulate the industry. Congress legalized hemp in 2018, and what a disaster that has been. The FDA has punted on regulating CBD from hemp so far.

Rescheduling won’t change the fact that each state runs its own medical cannabis program. It also will have no impact at all on adult-use cannabis programs. Some believe that the exchanges will begin to list companies that they won’t include now, but their decision to not include American cannabis operators is not based on a legal restriction. Rather, it is their choice. Perhaps these policies will change, which would be fantastic, but this is very uncertain.

The GTI Outlook

Green Thumb Industries reports its Q1 financials on Wednesday after the close. Analysts project, according to Sentieo, that the revenue will be $269 million, up 8% from a year ago. Adjusted EBITDA is expected to gain 20% to $81 million.

For 2024, the 17 analysts are projecting revenue to grow 6% to $1.119 billion with adjusted EBITDA of $339 million, up 4%. This is a bit better than in late February, ahead of the Q4 report. For 2025, 11 analysts project revenue will increase 8% to $1.208 billion with adjusted EBITDA growing 8% to $365 million, a margin of 30.2%. In 2021, the margin was 34.5% on revenue of $894 million.

GTI Trades at a Premium to Peers

The company ended 2023 with cash of $162 million. Net debt was $147 million, which is low compared to peers. The stock has a tangible book value of $691 million, which is very high compared to its peers. The current price works out to be 4.7X tangible book value, which is not really a bargain except compared to its peers.

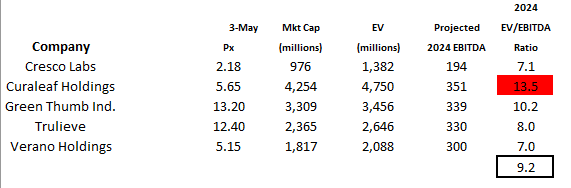

Looking at enterprise value to projected adjusted EBITDA, the stock trades at about 10X the 2024 estimate. This is a big discount to where Curaleaf (OTCPK:CURLF) trades, 13.5X, but it is a premium to the other peers, Cresco Labs (OTCQX:CRLBF), Trulieve (OTCQX:TCNNF) and Verano Holdings (OTCQX:VRNOF). The Tier 2 names have some lower valuations. Here is a table with price to tangible book value and forward ratios for enterprise value to adjusted EBITDA:

Alan Brochstein, using Sentieo

When I wrote the report in late February, I was concerned that the market was overly optimistic about the DEA. While it’s not yet finalized, I expect that cannabis will be rescheduled. While there is substantial downside if this doesn’t happen, I am no longer providing two targets (an optimistic one and a pessimistic one). My optimistic target in that February target was based on an enterprise value to projected adjusted EBITDA for 2025 of 12X, and this worked out to be $18.76. With the lower projected adjusted EBITDA, that same ratio yields a lower target. I am now expecting that GTI will trade to $16.88 at year-end, 28% higher.

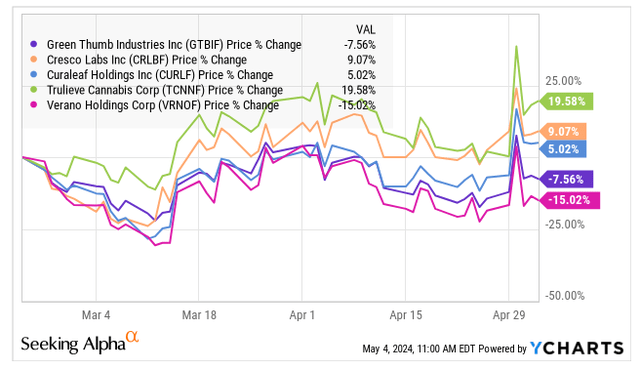

The GTI Chart

Since the late February article, GTI has underperformed the other Tier 1 MSO names:

YCharts

The only stock to perform worse than GTI has been Verano, which I continue to feel is no bargain. The overall cannabis sector, as measured by the New Cannabis Ventures Global Cannabis Stock Index, has climbed by 19.0% since 2/23, which is more than all of the large MSOs except for Trulieve. Given the positive news for the MSOs with the DEA planning to reschedule cannabis, it’s kind of surprising to many that the large MSOs aren’t performing better.

I think it’s interesting that Green Thumb Industries still trades below its peak in late 2022:

Schwab

I see support at $12 and then $10. If it can finally clear $16, I see resistance at $18. 3 years ago, the stock was in the low $30s, and it tested $40 in early 2021 at its all-time high.

I have expressed concern that AdvisorShares Pure US Cannabis ETF (MSOS) owns so much of this stock, and it continues to do so. The 20.4 million shares it holds represent 23.9% of the fund. I am, however, less concerned that MSOS will melt down and have share redemptions, though this may happen if rescheduling fails to take place.

Conclusion

When I wrote about GTI in late February, I had no exposure in my model portfolios. As it underperformed its peers, I did add some to my model portfolio focused on American cannabis operators, and I still own it there. The position size is 8.3% after my purchases on 5/3. This is about the stock’s weight in the index I am trying to beat. It is the only Tier 1 name that I own currently, and I have 12.4% cash.

For those who are bullish on cannabis stocks, this one could be a big winner. Perhaps my target is too low! I remember several years ago when 20X adjusted EBITDA was the typical valuation. GTI has the best balance sheet by far from the Tier 1 names, and its valuation could do better than I currently expect. Of course, there could be problems too. The rescheduling is not a done deal, and it may not happen.

I don’t think that GTI is the best MSO to buy, and I continue to view other parts of the cannabis market as having better potential upside relative to the potential downside. This DEA move has me excited about the ancillaries, which should benefit from a financially healthier customer.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q1 2024 Earnings Call Transcript")

")