")

Investment thesis

Gaming and Leisure Properties, Inc. (NASDAQ:GLPI) operates within a gaming properties sector that offers unique value drivers compared to other triple net lease REITs. To name a few of them:

- Mission-criticality of assets that often come with a brand value in itself.

- High occupancy rates are derived from a low supply of suitable properties and regulations limiting tenants’ ability to move.

- Strong, triple net leases with outstanding terms and favorable lease escalators.

- Immunity to some major secular trends (incl. the “Amazon effect” or advancing digitization).

Combining an attractive dividend, yielding ~6.4%, potential for multiple appreciation, and further growth resulting from both contract-embedded rent escalations, as well as investment activities, GLPI offers an opportunity for double-digit total returns.

Introduction

GLPI is the most geographically diversified gaming-oriented REIT.

Within this analysis, I’ve presented GLPI’s overview, its financial situation, and its investment outlook.

I’ve also included a valuation outlook, risk factors, and key takeaways summarizing my investment thesis.

GLPI – overview

Quality properties in a unique sector

With gaming-oriented properties remaining at the core of GLPI’s portfolio, the Company offers unique value drivers compared to other triple net lease REITs. To name a few of them:

- High barriers to entry due to limited supply and the rigorous regulatory environment surrounding the gaming market.

- Absolute mission-critical characteristics of the assets as many of them represent a brand in themselves. Moreover, the tenants’ ability to move locations is limited due to the previously mentioned regulations.

- Referencing the above point – unlike the properties of the most popular net lease REITs that often target retail or service-oriented properties, GLPI’s assets are highly differentiated, and non-commoditized which further increases their value proposition.

On top of that, GLPI’s business shows low cyclicality and immunity to some major secular trends (incl. the “Amazon effect” or advancing digitization), as well as experiential character with a favorable supply-to-demand balance.

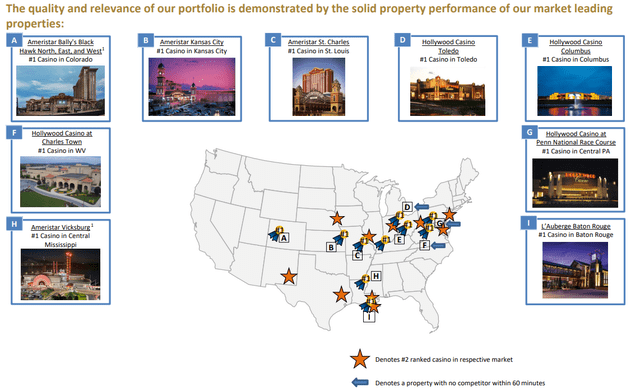

GLPI has the most geographically diversified gaming portfolio, owning 65 gaming properties across 20 states (only 1 in Las Vegas) – including its latest acquisition announced on May 16, 2024.

Despite lacking such recognizable establishments like one of its closest peers – VICI Properties Inc. (VICI) which owns 10 trophy assets, GLPI’s portfolio features properties that are often leaders within their markets.

GLPI – Investor Presentation

Outstanding business metrics

1. Lease terms

GLPI secures arrangements with lease terms significantly exceeding triple net lease REITs operating within other niches.

Most of its current leases have renewals incoming in the 2030 – 2040 period with renewal options amounting to 15 – 25 years. Its recent acquisitions involved initial lease terms of 25-30 years with renewal options.

For reference, some of the most popular net lease REITs like Realty Income Corporation (O), NNN REIT, Inc. (NNN), Essential Properties Realty Trust, Inc. (EPRT), Agree Realty Corporation (ADC), or EPR Properties (EPR) have weighted average lease terms of 9.8, 10.0, 14.1, 8.2, and 12 years, respectively.

2. Occupancy rate

According to O’s Investor Presentation, the historical median occupancy rate of an S&P 500 REIT is 94.8% with the lowest year-end level of 91.9% during the 31.12.2000 – 31.03.2024 period.

However, according to the Investor Presentation, GLPI has operated at a 100% occupancy rate since inception, which corresponds to (and confirms) the mentioned mission-criticality of leased assets to their tenants and limited possibilities for tenants to switch locations.

3. Rent escalations

The Company operates based on triple-net lease agreements that require tenants to bear a substantial portion of the costs associated with the operation and maintenance of the property, including property taxes and insurance.

These contractual increases generally amount to 1% – 2% annually, with GLPI tending to stick closer to the higher end of this range and sometimes exceeding it. GLPI’s acquisition announced on May 16, 2024, resulted in a contract with a 25-year initial lease term and is subject to 2.0% annual rent escalations in years 3-10, followed by increases of the greater of:

- 2%.

- CPI.

in years 11-25 (capped at 2.5%).

These low single-digit rent escalators may not seem like a lot. However, they tend to add up over time and heavily impact the bottom line due to the triple-net character of leases.

Financial stance

GLPI brought quite a modest AFFO per share growth at a CAGR of 3.0% for the 2019 – 2023 period (with 2018 as a base year). However, it’s a result of mainly the 2020 – 2021 period when its AFFO per share marked a year-on-year change of 0.3% and (0.3%), respectively.

During Q1 2024 GLPI showed the same AFFO per share level of $0.92.

At the time, GLPI updated (in plus) its 2024 guidance to $3.71 – $3.74 AFFO per share (assuming 0.9% year-on-year growth on midpoint).

However, as GLPI’s guidance has been updated on April 25, 2024, it doesn’t reflect the impact of its latest acquisition according to the indicated assumption:

The guidance does not include the impact on operating results from any possible future acquisitions or dispositions, future capital markets activity, or other future non-recurring transactions.

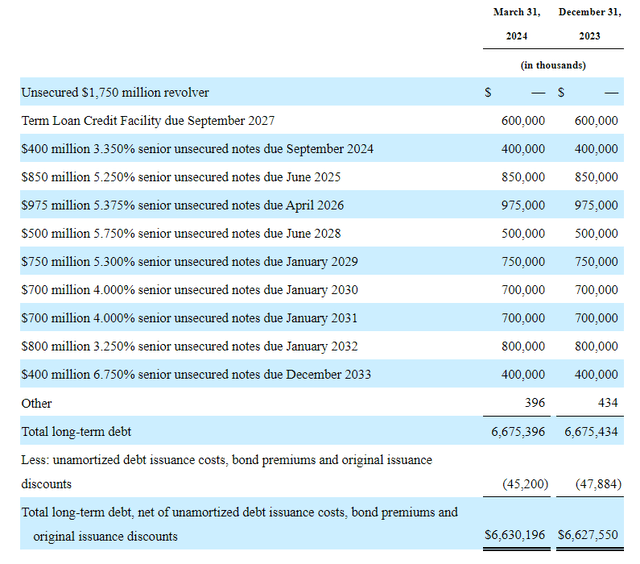

From a liquidity standpoint, GLPI has an investment-graded balance sheet with a BBB- rating.

Referring to the latest SEC filings, unsecured debt amounted to 100% of the Company’s total debt.

GLPI has a well-laddered debt maturity profile with ~6.0% of its debt maturing in 2024. Therefore, the current high-interest rate environment has a limited impact on its capabilities of refinancing and future financial performance.

GLPI’s 10-Q report for Q1 2024

With a higher-than-average AFFO payout ratio of 79.7%, there might be some investors concerned about GLPI’s capabilities to sustain and grow its dividend. To address that, I would like to quote Matthew Demchyk, Senior Vice President and Chief Investment Officer from Q1 2024 Earnings Call:

Our focus on stability and dependability continues to show in the consistency of GLPI’s cash flows and the solid four-wall coverage across our leases. Our business model is built to navigate business cycles, including economic and interest rate volatility.

History suggests that heightened volatility, often leads to opportunity for those who are prepared. At GLPI, we have worked hard to prepare. Our leverage and liquidity are at levels that strengthen and support our business model.

The Company’s management remains confident in GLPI’s liquidity and position to fund its further activities.

Investment activity

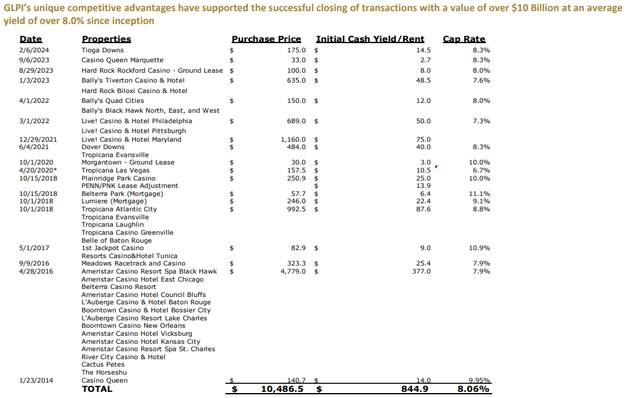

GLPI has been able to secure attractive cap rates (avg. 8.06%) with over $10 billion worth of investment volume since inception.

GLPI – Investor Presentation

The above summary doesn’t reflect its latest acquisition announced on May 16, 2024. The funding amount consisted of $105 million of acquisition price and $ million of capital improvements to be funded.

As previously mentioned, the acquisition comes with a 25-year lease agreement subject to two 10-year renewals and favorable rent escalations. GLPI achieved a high cap rate of 8.4%.

In my recent analysis on NNN, I’ve mentioned Realty Income facing some size-related headwinds including being forced to step outside of its main business scope to keep the ball rolling. In October 2024, we’ve also seen VICI complete an acquisition of 38 bowling centers within the non-gaming experiential sector.

Some might link VICI’s move to a limited supply of gaming properties, thus opportunities.

However, GLPI keeps concentrating on gaming properties and remains capable of sourcing attractive opportunities within this sector (e.g. acquisition of real estate assets of Tioga Downs Casino Resort announced in February 2024).

To summarize this point, I would like to quote Peter Carlino – Chairman of the Board and Chief Executive Officer who shared his view on the investable market size during the Q1 2024 Earnings call:

I don’t think there’s any shortage of opportunity, if I understand the question correctly. We see a horizon of some pretty, I hesitate to say juicy, but good opportunities with partners and others that we have on the drawing board on a constant basis.

Valuation

Being an M&A advisor, I usually rely on a multiple valuation method that is a leading tool in transaction processes, as it allows for accessible and market-driven benchmarking within a specific peer group.

With that said, please review the reference group presented in the table below.

| Entity | Reference rationale | P/FFO (TTM) |

|---|---|---|

| GLPI | – | 12.6x |

| O | Triple net lease REIT. It generally targets retail and service-oriented properties, however, has some activity within the gaming sector. | 13.9x |

| ADC | Triple net lease REIT | 15.6x |

| EPRT | Triple net lease REIT | 15.2x |

| NNN | Triple net lease REIT | 12.9x |

| VICI | Triple net lease – the closest peer to GLPI business-wise as gaming properties remain at the core of VICI’s operations | 12.0x |

| EPR | Triple net lease REIT targeting experiential properties | 8.4x |

Numerous metrics are available for a company valuation, with EV/EBITDA being a rule of thumb for most sectors. However, in REIT analysis, FFO and AFFO indicators are more appropriate – depending on the instance. I chose P/FFO as this metric is standardized, meaning that different companies will use a standard formula (making them easier to compare), unlike P/AFFO which is more suited for financial performance assessment.

For transparency, I’ve included EPR in the reference group as it’s a triple net lease REIT targeting experiential properties.

I don’t consider EPR’s valuation to be well-representative as it is heavily undervalued and currently offers the best risk-to-reward ratio in the entire sector, which I’ve discussed in my recent analysis.

Nevertheless, as you may not agree with my views on EPR, you could also perceive its valuation as an appropriate benchmark while considering GLPI. Therefore, I’ve included it and for the above reasons – marked red.

Without further ado, gaming establishments are often considered riskier than retail and service-oriented properties targeted by many popular REITs.

However, many value drivers associated with operating within this sector support GLPI’s value proposition. To restate a few of them:

- Mission-criticality of assets that often come with a brand value in itself.

- High occupancy rates due to a low supply of suitable properties and regulations limiting tenants’ ability to move.

- Strong, triple net leases with outstanding terms and favorable lease escalators.

- Immunity to some major secular trends (incl. the “Amazon effect” or advancing digitization).

Adding GLPI’s ability to secure attractive acquisitions, its outstanding business metrics, and its coherent investment strategy, I don’t believe that the market appreciates GLPI’s long-term ability to generate cash flows and unique value drivers accompanying its niche.

Therefore, even assuming no major movements in the market environment (FED policy), I expect the P/FFO multiple to appreciate to 13.5-14.0x. Interest rate cuts will further support the appreciation.

Some of you may ask: “Hey, why do you expect GLPI’s P/AFFO to appreciate to that range since VICI, its closest business peer, is trading at just 12.0x?”.

That’s a reasonable question that I will address in a separate analysis of VICI, as I consider it to be undervalued. I actually believe that VICI will likely outperform GLPI. However, we will return to this matter.

The above doesn’t affect my views and investment thesis on GLPI. I’ve briefly shared my perspective on VICI and its P/AFFO multiple for transparency and to show my reasoning behind GLPI’s valuation outlook.

Risk factors

Prolonging the high interest rates environment will hurt both Companies’ performance, forcing them to refinance in worse conditions. However, this risk is limited due to low debt maturities ahead – especially in 2024.

Naturally, potential problems with major tenants heavily impacting financial performance are always a risk to consider while evaluating a REIT – especially given the relatively high tenant concentration. However, this risk remains limited as GLPI uses strong triple net leases with outstandingly long terms, and most of their rent roll is derived from publicly traded companies being key players in a specific niche, making it easier to monitor and address their financial health.

During the most recent Earnings Call, Peter Carlino shared his optimistic views regarding GLPI’s project pipeline within the gaming sector. Thus, don’t expect acquisitions outside of this niche to occur, however, if that were the case I believe that it would result in a higher stock price volatility. It could also shift my bullish attitude as I value the consistency between the management’s communication and investment decisions – depending on the instance.

Key takeaways

A strong balance sheet, outstanding business metrics, transparent investment strategy, high and well-covered dividends, as well as numerous benefits related to the unique character of the sector, are a testament to GLPI’s value proposition.

The Company offers an attractive risk-to-reward ratio with a potential of double-digit total returns resulting from:

- multiple appreciation,

- annual rent escalations and further acquisitions,

- attractive dividend yield.

I intend to monitor the Company’s future activities and evaluate my views.

Q2 2024 Earnings Call Transcript")