")

")

Investment summary

My recommendation for Genuine Parts Company (NYSE:GPC) is a buy rating. 1Q24 results showed very positive signs of growth ahead for the APG segment, which I expect to continue recovering as macro pressure eases (assuming the Middle East conflict doesn’t result in a full-blown modern conflict) in the coming months. While the IPG segment is still a drag, the US PMI index, which IPG has historically tracked well against, has broken above the 50points threshold, suggesting an expansionary environment that is positive for GPC as well.

Business Overview

GPC distributes auto parts and industrial replacement parts to all parts of the world, primarily in the US, which represents >70% of its sales as of FY23. In terms of profits, ~2/3 of its profit before taxes originates from the US as well. By segments: Automotive Parts Group [APG], which distributes automotive parts and accessories; Motion Electrical Specialties (previously known as Industrial Parts Group [IPG]), which distributes industrial parts like bearings, hoses, and other related components. GPC’s competitive advantage against smaller players stems from its scale which enables capacity to have more inventories on hand and better inventory turnover. Larger scale also means GPC is better capitalized to invest in assets (inventory, DCs, trucks) and using technology to widen the moat (IT helps where to place inventory to optimize cost and speed). In terms of market share, it was noted in the Raymond James 45th Annual Institutional Investors Conference that GPC automotive business is the largest player in Canada and APAC (20% market share) and 6% share in Europe. As a leading player, GPC definitely benefits from a macro turnaround faster than smaller players given the resources they have (can reinvest more aggressively).

1Q24 earnings results and FY24 guidance

Reported yesterday, GPC saw total sales growth of 0.3% to $5.78 billion, gross profit of $3.709 billion (35.9% gross margin), EBIT of $543 million (9.4% margin), and EPS growth of 3.5% to $2.22. Driving the growth was 1.9% APG growth and 2.2% decline in the IPG segment. APG revenue growth is further broken down into comparable sales grew 0.2%, acquisitions contribution of 2.8%, and FX headwind of 1.1%. IPG sales growth is broken down into comparable sales decline of 2.6%, acquisitions contribution of 0.5%, offset by 0.1% FX headwind. While keeping their total sales growth outlook at 3%-5%, management increased their adj EPS outlook to $9.80-$9.95, up from $9.70 to $9.90 previously (implying margin expansion). I believe this EPS guide is achievable as the macro environment improves and management continues execute on its initiatives in the APG segment.

APG segment positive growth outlook

The APG segment is GPC’s largest segment, and hence, more attention is to be put here. Over the past few quarters, since 3Q22, the concern is that growth has been decelerating – from 8.9%y/y growth in 3Q22 to just 0.8% in 4Q23 (growth decelerated every single quarter between 3Q22 to 4Q23). Comparative sales were also down consecutive since 3Q22 from 9.2% to -2.7% in 4Q23. After 6 quarters of deceleration, 1Q24 finally showed signs of positive growth ahead. 1Q24 global auto comp saw a strong recovery to start the year, supported by improvement in US trends (0.6% growth vs 4Q23 6.1% decline), continued momentum in Europe (0.6% growth), and Australasia (1.2% growth), albeit Canada was still a drag (3.3% decline). The highlight is on US Automotive (largest geographical exposure for GPC) as trends improved sequentially. Moreover, average daily sales growth improved every month of the quarter, which, in my view, is evidence that management’s efforts to enhance the company are starting to bear fruit, particularly their emphasis on enhancing in-stocks and in-store service levels. I am expecting these benefits to continue showing results throughout the remainder of the year, and for U.S. automotive trends to improve sequentially.

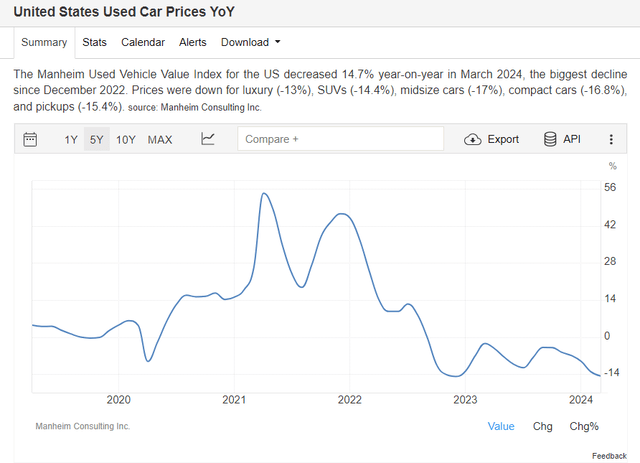

Additionally, I expect macro tailwinds to turn in favor of GPC in the coming months as the federal government looks to cut interest rates, which will reduce the cost of car loans and increase consumers’ spending confidence, which should improve the demand for car purchases. Used car demand should see more benefit from this macro situation, as prices have declined by double digits over the past few months. Relative to new cars, used cars have a higher tendency to breakdown (due to wear and tear, old parts, more mileage driven, etc.), which drives the demand for more auto parts (for repairs and upgrades).

Trading Economics

I believe the signs of positive macro tailwinds are already surfacing, as management noted positive buying behavior from independently operated NAPA (National Automotive Parts Association) stores during the quarter. Wage and rent increases, as well as interest rate hikes, have dampened demand from these operators in recent quarters, making it harder for them to buy inventory from GPC. The fact that the purchase trend has ticked up shows that either these operators are seeing increasing demand or they now have more budget (less cost pressure) to take on more inventory risk. Either way, it is a very positive sign of GPC APG sales growth ahead.

IPG showing signs of turnaround

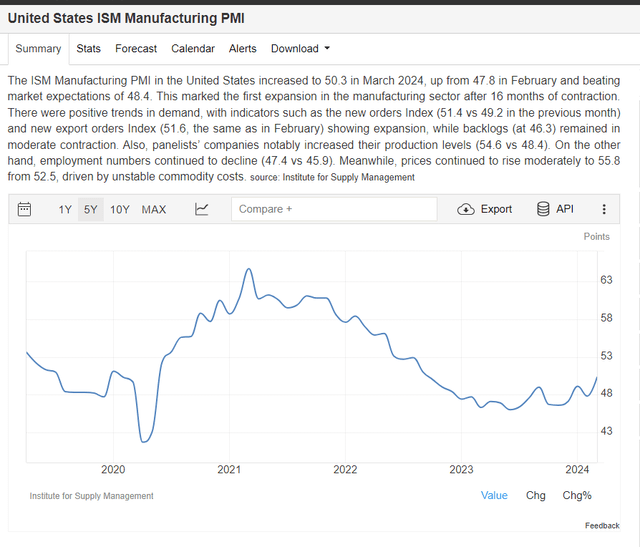

Trading Economics

The bigger drag now is still the IPG segment, which has seen comparable sales dips in the negative region, continuing the downtrend since 3Q22. However, there are early signs of manufacturing recovery in March that highlight 2H’24 upside for Motion. Looking at the US ISM Manufacturing PMI, it marks the first time it has passed the 50point threshold since 2023. The 50point threshold is an important gauge because >50 implies an expansionary trend, while <50 implies a contractionary trend. Historically, IPG comparable sales track in the same direction as the PMI index; hence, I believe the PMI index is a good indicator of growth. A recent report by S&P Global also paints a positive outlook on this front. While this trend could reverse, I note potential upside for industrial growth into 2H24 if optimism across the manufacturing industry continues.

Valuation

Redfox Capital Ideas

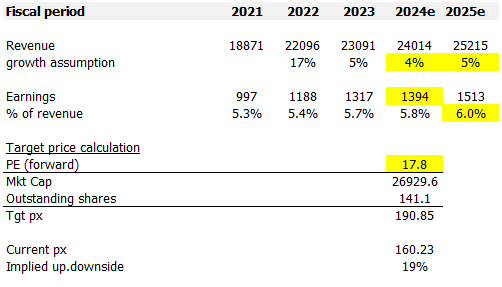

I model GPC using a forward PE approach, and using my assumptions, I believe GPC is worth $190.85. For revenue, given the APG segment positive growth outlook and early signs of IPG growth recovery, I believe GPC can grow as guided (midpoint of FY24 guidance) at 4% in FY24, followed by 5% (the high end of FY24 guidance) as demand continues to recover with macro pressures easing. As GPC scales the business by growing revenue, I would expect margins to continue expanding, which has been a historical trend when we compare GPC’s revenue size vs. net margin (FY17 revenue: $16.3 billion with a net margin of 4.2% vs. FY23 revenue sales of $23 billion with a net margin of 5.7%). The market has reacted very well to the early growth signs revealed in the 1Q24 results, as seen from the sharp reversal in share price (from $145 to $160 post-results). GPC valuation (15x forward PE) also compares favourably against peers like O’Reilly Automotive (ORLY) that trades at 25x, Advance Auto Parts (AAP) that trades at 17x and Autozone (AZO) that trades at 16x. Historically, GPC has traded in line with peers but because of the recent slowdown, valuation has traded at a discount. Hence, as GPC continues to recover, we should see the PE multiple slowly trend back upwards, towards its historical trading average of 17.8x (closer to peers average of ~19x).

Risk

A macro slowdown would put further pressure on GPC recovery strength, similar to what happened last year. As I am writing this, Israel has retaliated against Iran by launching a missile attack. This could spark an entire conflict throughout the Middle East, driving oil prices up, which will dampen the demand for cars and naturally lower demand for car parts. Another risk is that the Fed might not cut rates as inflation and the US housing undersupply situation have not been fully addressed yet. In this scenario, the pace of consumer spending recovery may not be as great as I expect. Naturally, this would impact auto demand because car loans are going to stay expensive for longer, dampening the recovery strength.

Conclusion

My view for GPC is a buy rating. The APG segment, which is GPC’s largest, is showing signs of recovery with improving sales trends, particularly in the US market. I expect this trend to continue throughout the year, fueled by potential macro tailwinds such as easing interest rates and increasing consumer spending confidence. Additionally, the IPG segment may be nearing a turnaround as suggested by the recent uptick in the US ISM Manufacturing PMI. Overall, as this trend continues, GPC should see revenue growth, margin expansion, and a return to its historical average forward PE multiple. The main risk to this outlook is a potential macro slowdown, particularly a full-blown conflict in the Middle East.

")