This half yearly letter is lengthier than usual as I am using it to inform you about some changes in the way we manage Fundsmith Equity Fund (‘Fund’).

However, first the table below shows the performance of our Fund and other comparators during the first half of 2026 and since inception.

% Total Return

1st Jan to 30th June

2026

Inception to 30th June 2026

Cumulative

Annualised

Fundsmith Equity Fund1

-2.9

+592.6

+13.1

Equities2

+11.2

+530.9

+12.5

UK Bonds3

+0.7

+32.1

+1.8

Cash4

+1.8

+25.7

+1.5

The Fund is not managed with reference to any benchmark; the above comparators are provided for information purposes only.

1T Class Accumulation shares, net of fees priced at midday UK time, Inception, 1.11.2010, source: Bloomberg.

2MSCI World Index, £ Net, priced at close of business US time, source: www.msci.com.

3Bloomberg Series-E UK Govt 5-10 yr Bond Index, source: Bloomberg.

4£ Interest Rate, source: Bloomberg.

Our Fund was down by 2.9% in the first six months of the year, 14.1 percentage points less than what is perhaps the most obvious comparator — the MSCI World Index (£ net). I have moved the usual analysis of attribution of that performance to an Appendix to this letter as there is another subject I wish to cover first, namely what we are going to do about this performance.

The backdrop to this continues to be a market which is dominated by so-called passive or index funds (of which the majority are ETFs) and the boom surrounding AI which have combined to produce a market dominated by momentum rather than any fundamental factors like profitability, returns on capital and growth — in other words the factors we focus on.

I have already written about the effect of this, but I am indebted to Simon Evan-Cook writing in a Substack called Wealth Yourself* in April for some further observations entitled ‘Victory for Passive! 22 thoughts and questions’, subtitled ‘Passive has conquered the world. What could possibly go wrong? Quite a lot.’

Mr Evan-Cook points out that an original argument for switching to passive investment was that ‘it’s hard to beat the market, and the average investor will fail (because of charges). So why not save time and money by buying the whole market through a low-cost tracker, and get slightly better performance than the average active fund manager’ as a result of the fees saved?

In the recent stunning outperformance of active managers by index funds, this rationale has been conveniently forgotten. In the UK, for example, Vanguard’s UK All Share tracker has made 66% over the past five years, trouncing the average UK equity fund’s return of just 32%. This is seen as a reason to switch even more money from active to passive and so reinforce the feedback loop.

If the average active fund charges 1% and returned 32% after those charges, and the index is supposed to be the sum of those active managers, shouldn’t the tracker have made something like 37%? How did it make 66%?

To quote Mr Evan-Cook: ‘This is great if you’ve held the tracker, but it makes a nonsense of that original ‘settling-for-average’ argument. It also poses the question: If the tracker can perform 29% better than the average active manager, why can’t it perform 29% worse?’

An associated observation is that ‘passive funds are starting to look like active funds’.

Index funds now ‘dominate the fund performance tables. In 2018 the top quartile was filled with active ‘quality-growth’ funds, in 2022 it was filled with active ‘high-growth’ funds, and in 2026 it’s filled with index funds: 12 of the top 20 performers over five years are trackers.’

Plus, index funds are taking more concentrated positions than many active managers. ‘Half of Vanguard’s FTSE 100 tracker is held in just 10 stocks, and it has significant ‘sector bets’ on banks, oil producers and mining companies. Index funds aren’t the low-risk, diversified portfolios they used to be.’

Mr Evan-Cook focuses on the UK, but these statistics and arguments are even more pertinent for the US market where the AI plays dominate the indices and the market performance. The US market delivered a total return of 83% over the five years to the end of May in USD (price return was 71%). Meanwhile the average open-ended equity fund investing in the US (3,107 with 5 year records), returned 59% in USD. So index funds outperformed active funds on average by 24%.

Moreover, whilst AUM in index funds is now >60%, in terms of volume of trades, active fund managers are an even smaller minority than this implies. According to Cboe Global Markets, having been 80% of trades in the 1990s, active funds share of trades is now down to just 10%. The trading activity which drives prices is now driven not by active fund management decisions but by the momentum feedback loop of funds moving from active to passive and reweighting within passive funds.

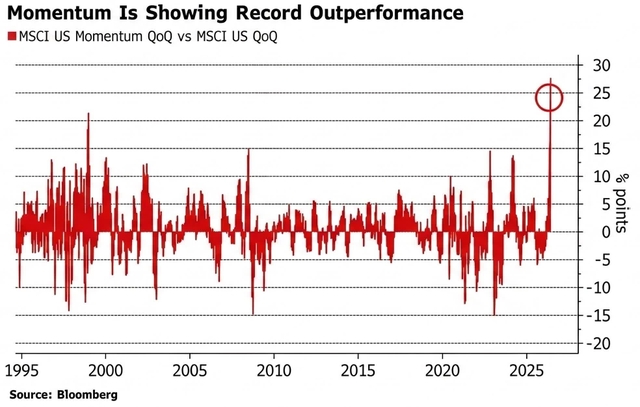

I have read comments about these arguments which suggest that this explanation for what is happening is incorrect. However, the performance of momentum based investment is clear as this Bloomberg chart illustrates:

It is at a 30-year high and more extreme than in late 1999 just before the Dotcom bubble burst. As active fund performance continues to worsen, more people abandon it, producing a pernicious feedback loop.

Yet another illustration that index investing is not truly ‘passive’ was given in an interview with David Booth, co-founder of Dimensional Fund Advisors (which now manages over $1trn of assets) published in Barron’s on 18th June. Asked about the rule changes allowing SpaceX to be included into indices more quickly than usual (to accommodate the June 2026 SpaceX IPO, major indices relaxed their inclusion criteria with the Nasdaq-100 eliminating its 3-month seasoning period — meaning the stock has to be traded for three months prior to inclusion — and its 10% float requirements so that it could be included despite having less than 10% freely tradeable) Booth said, ‘I think you’re hitting on a bigger problem. Say you don’t like active management and go to an index. Well, somebody’s managing that portfolio, which isn’t the fund manager, it’s the index provider. If the index provider changes the index, the fund has to change, so index funds are really trading desks. [Index providers] are sensible people, but they’re not fiduciaries looking out after me. They’re looking out after them… It doesn’t make them bad, but people need to realise what’s going on.’

What we are surely seeing is that index funds, like other financial innovations, start with a good rationale but inevitably end up being taken to extremes, ultimately with dire consequences. The development of credit derivatives in the 1990s and the subsequent Great Financial Crisis of 2007–08 are a recent illustration of this.

With regard to what the headlong dash from active to index funds is doing I rest my case, for now at least.

It is important to state at this point that we remain firmly of the view that owning a group of stocks which have better fundamental characteristics than the index (better and more defensible returns on capital employed plus a source of growth into which to deploy at least part of the cash generated) at a reasonable valuation will produce a superior investment return to the market over the long term, and particularly so if volatility is taken into account.

Every day we seem to be presented with examples of what the rise of passive investment is doing to the market in terms of volatility. On Wednesday 27th May Snowflake (SNOW US), a database company closed trading as a $60bn company and opened on Thursday as an $82bn one. On that Thursday, the baton of volatility was passed to Dell Technologies (DELL US), the computer hardware company. Its stock closed as a $205bn company and opened on Friday as a $273bn one. That opening increase of 33% is after the shares had already doubled since the beginning of March.

I would make several observations about this which is a tale we could write about almost every day (as the sequence above hopefully serves to illustrate):

I am not aware of any fundamental methodology of investment which could help to predict or capture these moves.

Such moves are surely driven in part by the fact that such a small proportion of trades are now conducted by active funds whose managers could think ‘That move is ridiculous, I will sell some’ as few such managers can survive given that investment processes which attempt to fly in the face of momentum jeopardise one’s career.

You may take the view that you can switch into the index and reap the benefits of this momentum and then switch back if or when events cause this momentum to unwind. However, if $200bn market valuation stocks are moving 33% a day in a bull market, you can reasonably speculate about what’s going to happen if or when things reverse. It may make 2000–03 and 2007–08 look like a blip. In 2007–08, the S&P fell 57% in five months. Next time round, it would not surprise me if it accomplished this in five days. In 2000–03 it took even eventual winners like Amazon 10 years to recover their peak share price.

We are particularly mindful of the motor racing maxim, frequently attributed to legends like Rick Mears or Charles Jarrott, relating to the Indianapolis 500 Race, that ‘In order to finish first, you must first finish’. This emphasizes that endurance and reliability are just as crucial as speed in the 500-mile race.

You might say (and we would indeed say) that is exactly what we are trying to do by focusing on investing in companies with good fundamental business and financial characteristics and at least reasonable valuations or better. However, there is another factor at work here — fund flows. We run open-ended funds, and you can and increasingly have been taking money out, we suspect mostly to join the exodus from active to passive, or possibly to invest in managers who profess that they understand quality better than we do. They may be right, or they may just be closet momentum investors, which will be fine until it isn’t. However, there will be little point being proved right about the dangers of passive or momentum investment after our Fund has closed.

It is against this background that we are implementing some adaption in our fund management process.

But let me begin by stressing what will not change. Our investment mantra is to seek to:

Buy good companies

Not overpay

Do nothing

We have no intention of investing in anything other than good businesses whose characteristics are such that they should compound in value over time better than the market average and at reasonable valuations as well as providing some fundamental support for the value of our investment in the event of a market dislocation.

However, it seems clear that the third leg of our strategy which probably needs the most change and our portfolio turnover hit a high of 51% in the first half of this year as we made significant changes in the portfolio. However, you should not expect that level of turnover to become the norm.

In a market in which share price moves of 33% per day for even large stocks are not uncommon a buy and hold strategy can only work if you are not subject to flows, and we are. Sticking to our current approach may well fall foul of the adage that the market can remain illogical longer than we can remain in business. You should therefore expect that we will be more active in future. I still expect our turnover and its cost to be significantly below that of most active funds, but it may well be higher than our historic average.

We will take more account of momentum — both fundamental and share price — in our investment decisions. In particular, we will be much less willing to deploy the time-honoured technique of buying quality companies when they hit a glitch. This was used to good effect, for example, by Warren Buffett to buy Berkshire Hathaway’s stake in American Express (AXP) during the salad oil scandal (look it up) and by us, for example, in buying Microsoft (MSFT) at the end of Mr Ballmer’s tenure as CEO. But in the current momentum driven market buying shares in companies which have hit a glitch is like trying to catch the proverbial falling knife. All we are getting is cut fingers as their downward share price spiral is exacerbated by the index momentum enhancement effect. It is worth noting that Mr Buffett executed this strategy in a closed fund which he controlled not an open-ended fund.

We have no desire to hug the index. You can buy index funds which are much cheaper than us or any other active manager, so what would be the point?

I profess no insight into how or when this passive-led momentum market will end, other than to say badly. It may be that a realisation that the humungous investment in AI cannot produce an adequate return or any clear winner(s) will derail it. Or that the destructive effects of AI on other sectors may be such that it punctures the market narrative and/or even that layoffs amongst workers made redundant by AI who are currently fuelling the passive boom with their 401(k) pension fund contributions will send that flow and the market into reverse. More likely it is something which we cannot foresee. After all a crisis would not be a crisis if we could foresee it. But we do know that trees do not grow to the sky.

During the 6 months ended 30th June we executed a series of trades which reflect this attempt to adapt our strategy to suit the current and expected market conditions:

We began accumulating stakes in AppLovin (APP), GE Vernova (GEV), Legrand (LGRDY), Mastercard (MA), Netflix (NFLX), Nextpower (NXT), Sage (SGGEF), The TJX Companies (TJX), TSMC (TSM), Uber (UBER), Veeva Systems (VEEV), and Yum! Brands (YUM).

We exited or have started exiting: Atlas Copco (ATLKY), Coloplast (CLPBF), EssilorLuxottica (ESLOF), Intuit (INTU), LVMH (LVMHF), Magnum Ice Cream (MICC), Mettler-Toledo (MTD), Nike (NKE), Novo Nordisk (NVO), Otis (OTIS), Unilever (UL), Wolters Kluwer (WOLTF), and Zoetis (ZTS).

The rationale for each sale and purchase is covered in Appendix 2 to this letter. The sales were often driven by a complex mix of factors including lack of fundamental momentum, mismanagement and simple valuation.

We are well aware that in some cases we have sold stocks at a loss and/or after purchasing them recently. We are also aware that some of the stocks we are buying have been bought and sold by us before or could have been purchased at much lower prices in recent years. But those stocks do not move on the basis of whether or not we own them.

A quick snapshot of the fundamental characteristics of the resulting portfolio is as follows:

ROCE

31%

Gross margin

62%

Operating margin

29%

Cash conversion

92%

Interest cover

43.0x

FCF yield

4.3%

Source: Fundsmith, as at 30th June 2026

Hopefully this reinforces the suggestion that we have not abandoned our strategy of seeking to own good companies at fair or better valuations but have rather sought to refine it.

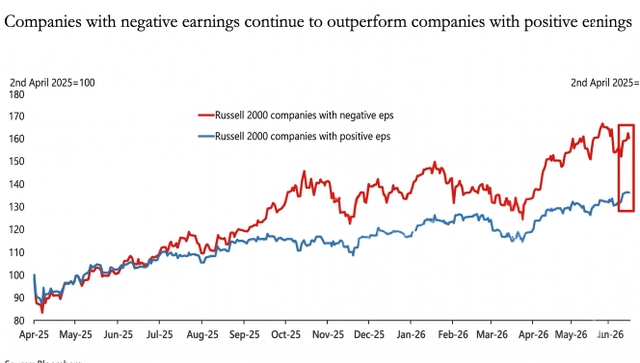

The weighted average Free Cash Flow (‘FCF’) yield of 4.3% is worth mentioning. The S&P 500’s FCF yield is estimated to have fallen below 2% primarily due to the cash flows of its largest constituents — the major tech companies — having been absorbed by the spending on the AI ‘arms race’. Whilst this relative valuation would normally be cause for optimism, given recent market trends it might be a source of worry. The chart below (which covers the Russell 2000 Index) shows that companies with negative earnings — or losses as they are usually termed — have been outperforming those which are profitable and continue to do so.

The movie which this brings to mind is It’s a Mad, Mad, Mad, Mad World (made in 1963, starring Spencer Tracy, Sid Caesar, Mickey Rooney, Phil Silvers and Terry-Thomas).

Our portfolio’s relatively low valuation is a source of comfort to those like us who concern ourselves with the fundamentals of a company as opposed to those who follow a momentum strategy.

Moreover, we estimate that these companies will grow their cash flow by about 14% p.a. over the next 3-5 years. If so — and many of them are relatively predictable — they will either be even more lowly valued or their share prices will have risen to reflect this. We hope you are still invested with us to see that happen. We will be.

Yours sincerely,

Terry Smith CEO, Fundsmith LLP

APPENDIX 1 – Attribution

What did well for us in the first six months of 2026? Here are the five biggest positive contributors to performance:

Stock

Attribution

Fortinet

+2.8%

Texas Instruments

+1.7%

Marriott

+1.3%

Alphabet

+1.0%

Philip Morris

+0.7%

Source: State Street

Fortinet and Texas Instruments are obviously tech companies but neither is directly involved in the AI phenomenon. We have held Philip Morris since inception.

The five biggest detractors from our Fund’s performance during the period were:

Stock

Attribution

LVMH

-1.4%

Zoetis

-1.1%

IDEXX (IDXX)

-1.1%

Microsoft

-1.0%

Coloplast

-0.9%

Source: State Street

Coloplast, LVMH and Zoetis have been sold for the reasons given in Appendix 2. We have reduced our stakes in IDEXX on valuation grounds and in Microsoft.

Our portfolio turnover in the first half was 51.8%. Voluntary dealing (dealing not caused by redemptions or subscriptions) cost £11,404,962 during the half year (0.084%). The Ongoing Charges Figure for the T Class Accumulation shares was 1.05% and with the cost of all dealing added, the Total Cost of Investment was 1.12%.

APPENDIX 2 – Sales and Purchases Sales

Atlas Copco – Organic growth has been anaemic over the last two years, which in our view does not justify a <3% FCF yield which has resulted from the shares rising sharply over the past year.

Coloplast – Organic growth has fallen from a long term average of 8% to 6%. Not coincidentally there have also been a couple of high-profile screw-ups involving acquisitions.

EssilorLuxottica – The lower margins on smart glasses forced the company to abandon its long-term profit targets. It is still a very interesting company with the rise in wearables and smart glasses, but increased competition in this segment is inevitable.

Intuit – Although we only recently repurchased Intuit we were sensitive to the way in which they have reacted to the poor Mailchimp acquisition as this is why we sold the shares in the first place. The fact that they have now taken to giving results ex Mailchimp both shows how bad the acquisition was but also worries us about a continuing state of denial.

LVMH – The key China market seems unlikely to recover until the property market does. Family succession plans are also an increasing concern.

Magnum Ice Cream Co. – The company is too small and illiquid for us to build a meaningful position.

Mettler-Toledo – Underlying growth so far this year is only 1%, which isn’t enough to justify its traditionally premium valuation.

Nike – It is clear that any turnaround from new CEO Elliott Hill after the damage done in the pandemic period will take longer than we’d initially expected, especially as China and Converse continue to be problems.

Novo Nordisk – Parlayed a market leading position in the biggest drug discovery in decades into an investment disaster.

Otis – The growth in maintenance and modernisation of lifts hasn’t been fast enough to offset the decline in new construction from China.

Unilever – When Hein Schumacher was appointed as CEO we breathed a sigh of relief after the Poleman/Jope years of woke. He said he had no intention of indulging in acquisitions or divestments until he had got all the businesses producing the results they should be capable of benchmarked against the best of their competition. We applauded that approach.

After 18 months he was fired and the CFO Fernando Fernandes was appointed as CEO. We thought Fernades was very capable both as an operating manager and a CFO. However, his appointment was swiftly followed by the spin out of the ice cream business as the Magnum Ice Cream Company allegedly because its separate distribution chain did not fit with the rest of Unilever. At the time we asked if that was all the disposals for the foreseeable future and were told it was.

This was then followed by the announcement of the intention to transfer the remainder of the food business to McCormick (MKC).

Apart from the fact that this flies in the face of what we were told and what we liked about Hein Schumacher’s approach, it has all the hallmarks of Nelson Peltz, the activist investor who is on the board. We have seen Nelson in action back to the 1980s. We are not fans of the idea that corporate activity solves fundamental problems. Nor are we fans of boards who listen to activists who are not long-term investors.

Moreover, whilst Unilever management will be rid of the food business Unilever shareholders would still own it and it will be managed by the McCormick management. We know them well having owned the stock and we are not convinced they are good enough for the existing business let alone a massively enlarged one. McCormick has a ROIC which is consistently in single figures.

Oh, and the structure of the deal means we don’t get to vote on it.

Wolters Kluwer – While we still think this is a business that won’t be affected by AI as much as the current valuation suggests, we think there is better value in other businesses which have been affected by the Saaspocalypse such as Sage and Veeva Systems, which have higher growth rates and/or lower valuations.

Zoetis – we are unimpressed with management. They haven’t been able to respond effectively to new generics being launched in competition to its main franchises or even express themselves clearly.

Purchases

Industrials:

GE Vernova – GE Vernova builds and services the gas turbines and electrical grid equipment that power the modern world. Its competitive ‘moat’ stems from the scale and high switching costs of energy infrastructure: once its turbines are installed, customers are locked into high-margin, inflation-protected service contracts for decades. Unlike elevators and escalators, these generators cannot be serviced by independent providers because all the technology and materials are proprietary. GE Vernova’s equipment generates approximately a third of the world’s total electricity. Future growth depends on upgrading ageing power grids to handle the high voltages needed to deliver power from where it is produced to where it is needed, and on increasingly ‘behind-the-meter’ power generation at AI data centres. That growth is also fairly predictable as the current order backlog is $163bn (4x 2025 revenues). They are also the global leader in small modular nuclear reactors (SMRs). They currently have the only commercial SMR project (BWRX-300) under construction in the Western world, with the first deployment in Canada expected to be finished by 2030. ROIC: ~20% but rising rapidly, FCF yield: 2.6%.

Legrand – Legrand is a French manufacturer of the physical infrastructure behind electrical and digital building systems. Its competitive advantage relies on an entrenched distribution network and deep brand loyalty among electricians who refuse to risk their reputation on unfamiliar components. It makes mundane things in buildings, from fire escape signs to electrical sockets to the busways that carry cables in data centres. Legrand holds a nearly 20% global market share in wiring devices, meaning roughly 1 in 5 electrical switches and sockets globally are made by it. Growth opportunities lie in the rising demand for energy-efficient smart buildings and specialised power distribution systems for data centres. ROIC: low 20s, FCF yield: 4.4%.

Nextpower – Nextpower manufactures mechanical systems and software that enable utility-scale solar panels to track the sun throughout the day. Its competitive ‘moat’ combines a flexible, outsourced manufacturing setup that keeps fixed costs low with proprietary tracking software that makes switching to a competitor’s system difficult once installed. Nextpower technology increases the energy yield of a solar installation by 20% to 30% compared to traditional panels bolted in a fixed position. Growth is directly tied to the growing global demand for renewable energy, especially clean energy generation that can be built next to data centres. To further expand into data centres, Nextpower acquired battery maker Prevalon Energy for $365m in May 2026. ROIC: ~50%, FCF yield: 3.2%.

Uber – Uber operates a platform that connects users with ride-hailing and food-delivery drivers. It relies on a two-sided network effect: more drivers mean shorter wait times, which attracts more riders, making the platform highly sticky and difficult for local competitors to disrupt. Now that most of these challengers (Karhoo, Sidecar, Juno, Fasten, Hailo, etc.) have disappeared and Uber has survived, the network effects become very attractive. This is shown in the company’s cash from operations, which went from -$4.3bn in 2019 to -$445m in 2021 (last year of negative) to $3.6bn in 2023 and over $10bn in 2025. Uber’s logistics network is massive, coordinating roughly 42m trips and delivery orders every single day globally. Future growth opportunities include expanding into grocery and package delivery and eventually integrating autonomous (self-driving) vehicles (‘AVs’) into their fleet to drastically lower costs. Some see AVs as a threat to Uber, but we think it is more likely that Tesla, Waymo, etc., will use Uber’s distribution and global licenses to reach customers and maximise their asset usage rather than having to get licenses, build an app, and get tens of millions of people to download. ROIC: mid-20s, FCF yield: 7.4%.

Financials:

Mastercard – Mastercard operates a digital payment network connecting consumers, merchants, and banks worldwide. It benefits from a classic network effect: the more consumers use the card, the more merchants are forced to accept it, making it difficult for a new entrant to replicate. A new entrant would need to negotiate agreements and integrate its technology with the majority of global financial institutions. While digital payments feel ubiquitous in developed nations, roughly 1.4bn adults globally remain entirely unbanked. Future growth depends on bringing this unbanked population into the financial system, shifting remaining cash transactions to digital payments, and expanding into business-to-business payments, a far bigger market than C2C or C2B payments. We now own both Visa and Mastercard in the portfolio as payments is one of the few sectors that we expect to grow no matter what happens with AI, and Mastercard and Visa are equally good businesses. This gives us a way to achieve >6% exposure to payments without excessive stock-specific risk or breaching UCITS concentration rules. Also, with 46% of all global transactions still done in cash and B2B payments 85% of the value of total global payments, there is plenty of room for two companies to grow and compound. ROIC: >75%, FCF yield: 4.5%.

Health Care:

Veeva Systems – Veeva provides specialised cloud-based software designed specifically for the pharmaceutical and life sciences industries. Its software tracks the entire lifecycle of a drug from clinical trials through manufacturing and final sales. For example, during a clinical trial for a new drug, Veeva’s Vault eTMF (Electronic Trial Master File) is used to maintain the thousands of critical documents (trial protocols, investigator qualifications, ethics committee approvals). eTMF is the digital vault that organises these documents so the FDA or EMA can audit them at a moment’s notice to ensure the trial is safe and compliant. Veeva’s Vault QMS (Quality Management System) is used on the manufacturing floor. If a batch of medication is manufactured at the wrong temperature, Vault QMS is the software used to log the deviation, launch an investigation, and track the CAPA (Corrective and Preventive Action) to ensure it doesn’t happen again.

Its competitive ‘moat’ is built on extremely high switching costs: once a drug company integrates Veeva to manage strict clinical trials and regulatory compliance, it is risky and expensive to replace it. Pharmaceutical companies rarely switch from Veeva because replacing the software risks halting clinical trials or drug manufacturing, which would cost vastly more than any savings a cheaper vendor could offer. Additionally, moving to a new system requires a massive, expensive effort to pass strict regulatory approvals and transfer sensitive data without breaking legally required audit trails. Veeva holds roughly 80% of the market share in pharmaceutical customer relationship software, meaning almost the entire industry relies on its platform. Growth is fuelled by upselling new software modules to existing clients and by using AI agents to manage the administrative work of drug trials, which is currently very labour-intensive. ROIC: headline is ~15%, but that is due to a very large cash balance. Excluding cash it is well in excess of 100%; FCF yield: 5.7%.

Information Technology:

AppLovin – AppLovin provides software and artificial intelligence that assists mobile apps to find new users and sell advertising space. It is the company that shows you an advert between levels in Candy Crush or similar mobile games that you can’t skip. Its ‘moat’ is AXON, an advanced AI recommendation engine. AXON creates a powerful network effect by matching the right ads to the right users, driving better returns for advertisers and higher payouts for app developers, which makes it very hard for either side to leave. AXON can increase

AppLovin’s revenues by 20% p.a. for the foreseeable future simply by improving customer targeting. AppLovin’s platform serves over 1bn daily active users and generates advertising revenue that surpasses the combined totals of Snap, Pinterest, Reddit, and X. Future growth depends on expanding this highly profitable AI ad-matching technology beyond advertising new mobile games into e-commerce and potentially the Connected TV (CTV) advertising market. Unlike Alphabet and Meta, which price advertising based on the number of eyeballs who see or click the advert, AppLovin gets a percentage of the spend the advertisement triggers, so it gets significantly more revenue from higher-value items sold through its adverts (a room in a Marriott hotel or cosmetics vs a $5 mobile game). They are also launching a self-service platform for small to medium-sized businesses to buy advertising space. ROIC: >100%, FCF yield: 3.6%.

Sage – We switched our position from Intuit into Sage, the other main operator in accounting software. Sage has much less reliance on share based compensation, a lower rating and does not have Intuit’s record of injurious acquisitions. ROIC: 18%, FCF yield: 6.0%.

TSMC – Taiwan Semiconductor Manufacturing Company (TSMC) is the world’s largest contract chipmaker, physically manufacturing the semiconductors designed by companies like Apple, Broadcom and Nvidia. Its ‘moat’ is an unmatched technological lead in making the smallest chips, protected by the capital barrier of the $20bn it costs to build just one advanced factory. TSMC manufactures roughly 90% of the world’s most advanced semiconductors. Future growth stems from global demand for computing power, particularly the chips needed to train and run AI models. ROIC: 33%, FCF yield: 2.7%.

Consumer Discretionary:

The TJX Companies – TJX is the parent company of discount ‘off-price’ retailers like TJ Maxx (TK Maxx in the UK) and Marshalls. It has a highly agile supply chain and decades-long relationships with premium clothing brands, which allow it to buy excess inventory at steep discounts. TJX relies on a network of over 1,400 specialised buyers sourcing from 21,000 different global vendors, and creates an unpredictable ‘treasure hunt’ experience for shoppers that e-commerce struggles to replicate. Growth comes from physical store expansion and taking market share from traditional department stores. ROIC: 33%, FCF yield: 3.1%.

Yum! Brands – Yum! Brands is the parent company of major fast-food franchises, including KFC, Taco Bell, and Pizza Hut. However, it is finally selling Pizza Hut, which has been a significant drag on overall results. It has global brand recognition, franchising, and economies of scale in marketing and food purchasing, which independent restaurants cannot match. The speed of its global expansion is a key selling point: Yum! Brands opens a new restaurant somewhere in the world roughly every two hours, 365 days a year. Future growth depends on continuing this aggressive franchise expansion in emerging markets and on improving the digital ordering and delivery systems. There are also significant near-term opportunities for KFC in the US, where it has been underperforming, and for Taco Bell outside the US. ROIC: 50%, FCF yield: 4.0%.

Communication Services:

Netflix – Netflix is the pioneer of subscription-based streaming entertainment. It has a huge subscriber base which funds an annual content budget of over $17bn that smaller competitors simply cannot afford to match without losing money. Netflix now accounts for nearly 8% of all television screen time in the US, more than any single traditional broadcast network, but also underscoring its growth potential. Future growth will be driven by its newer advertising tier, cracking down on password sharing, and expanding local content in emerging international markets. The advert supported tier has 250m monthly active users, of whom 45% are in the US. After stopping password sharing in 2024, Netflix added 41m new subscribers (vs 325m total). They are increasingly moving toward live sports with NFL games on Christmas Day and ‘boxing’ matches like Mike Tyson vs Jake Paul. Why now? When Netflix was growing, there were many competitors (Hulu, Discovery+, Tubi, Disney+, HBO Max, etc.), so the network effects of streaming and content production did not work as well, as it had to compete for both customers and content. Now, many of these rivals have failed or are losing users, which highlights the quality of Netflix’s ‘moat’ but also presents an opportunity as those customers return to Netflix. ROIC: >30%, FCF yield: 3.8%.

Disclaimer: A Key Investor Information Document and an English language prospectus for the Fundsmith Equity Fund are available via the Fundsmith website or on request and investors should consult these documents before purchasing shares in the fund. Past performance is not necessarily a guide to future performance. The value of investments and the income from them may fall as well as rise and be affected by changes in exchange rates, and you may not get back the amount of your original investment. Fundsmith LLP does not offer investment advice or make any recommendations regarding the suitability of its products. This document is a financial promotion and is communicated by Fundsmith LLP which is authorised and regulated by the Financial Conduct Authority.

The views and opinions expressed herein are those of Fundsmith as of the date hereof and are subject to change based on prevailing market and economic conditions and will not be updated or supplemented.

Sources: Fundsmith LLP, and Bloomberg unless otherwise stated.

`* https://substack.com/@simonevancook

Data is as at 30th June 2026 unless otherwise stated.

Portfolio turnover is a measure of the fund’s trading activity and has been calculated by taking the total share purchases and sales less total creations and liquidations divided by the average net asset value of the fund.

P/E ratios and Free Cash Flow Yields are based on trailing twelve month data and as at 30th June 2026 unless otherwise stated. Percentage change is not calculated if the TTM period contains a net loss.

The MSCI World Index is a developed world index of global equities across all sectors and, as such, is a fair comparison given the fund’s investment objective and policy.

The Bloomberg Series-E UK Govt 5-10 yr Bond Index shows what you might have earnt if you had invested in UK Government Debt.

The £ Interest Rate shows what you might have earnt if you had invested in cash.

MSCI World Index is the exclusive property of MSCI Inc. MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or final products. This report is not approved, reviewed or produced by MSCI. The Global Industry Classification Standard (GICS) was developed by and is the exclusive property of MSCI and Standard & Poor’s and ‘GICS®’ is a service mark of MSCI and Standard & Poor’s.

Original Post

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Q4 2026 Earnings Call Transcript")

(NASDAQ:CSGP)")