")

")

Introduction

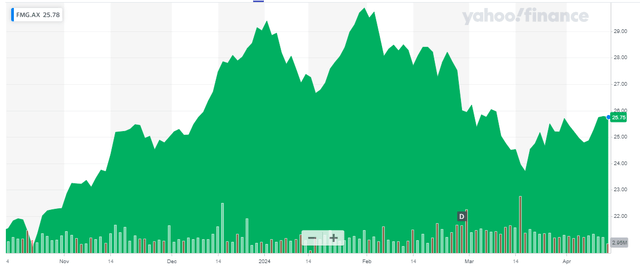

About seven months ago, I argued Fortescue (OTCQX:FSUMF) (OTCQX:FSUGY) was a good call option on the iron ore price, and I have not been disappointed with its performance. The stock is currently still up about 25% from the September 2023 share price, while the received dividend of A$1.08 represents an additional income for a total return of approximately 30%. The share price reached a high of around A$30/share at the end of January before losing some momentum as the iron ore price weakened.

Yahoo Finance

Fortescue’s primary listing is in Australia, where it is listed with FMG as its ticker symbol. The average daily trading volume is just under 6 million shares. Fortescue reports its financial results in US Dollar, so I will use the USD as the base currency throughout this article. As a reminder, 1 share of FSUMF represents 1 underlying share. A share of FSUGY represents two shares. While I will use the company’s financial results and performance in USD in this article, it goes without saying I recommend to trade in the company’s shares using the most liquid exchange, and in this case, that definitely is the ASX.

The cash flow kept (and keeps) on pouring in

The company’s financial year runs from July 1 st until June 30 th, with means the most recent detailed financial results made available by Fortescue are zooming in on the first semester of the financial year.

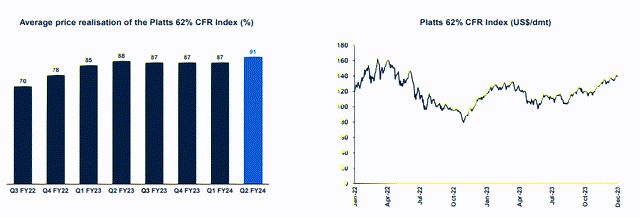

As Fortescue’s iron ore consists of lower grade material, the price it receives for its concentrate is obviously lower than the benchmark price (which is based on a concentrate with an average grade of 62% Fe). As you can see below, that discount has been pretty stable and actually narrowed in the second quarter of the current financial year.

Fortescue Investor Relations

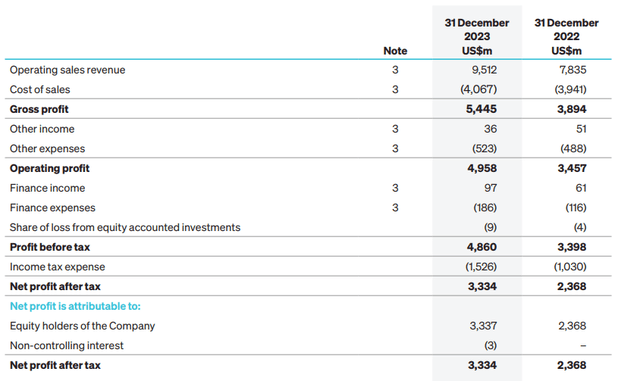

In the first half of the financial year, the company produced and sold a total of just over 95 million wet metric tonnes at an average realized price of US$108.19 per dry metric tonne. This resulted in a total revenue of just over $9.5B (of which $8.5B came from the iron ore sales in the first half of the financial year) after accounting for the moisture content in the iron ore concentrate.

As the company’s production cost is still industry-leading low at less than $18 per wet metric tonne, its margins and financial performance are obviously very strong. As you can see below, the gross profit came in at $5.4B for a gross profit margin of just under 60% and the cost of sales isn’t just the normal production costs but it also already includes the rail & port costs, the shipping costs (which it gets reimbursed for), the $ 640M in royalty payments and the close to $900M in depreciation and amortization expenses.

Fortescue Investor Relations

Thanks to the pretty robust balance sheet the net finance expenses are pretty low (at just over 1% of the total revenue from iron ore sales), resulting in a pre-tax profit of $4.86B and a net income of $3.33B which represents an EPS of US$1.09 per share. Fortescue clearly is a major contributor to the local economy and Australian economy as the company owes close to $2.2B in taxes and royalty payments based on the H1 FY 2024 results.

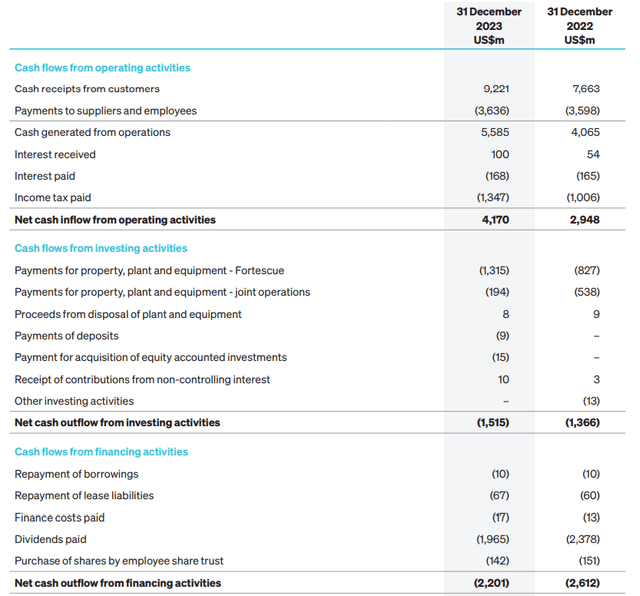

The cash flow statement below shows a total operating cash flow of $4.17B and roughly $4B after taking the normalized amount of taxes owed into account. After also deducting some of the finance costs (other than interest payments) and the $67M lease payments, the adjusted operating cash flow was approximately $3.9B.

Fortescue Investor Relations

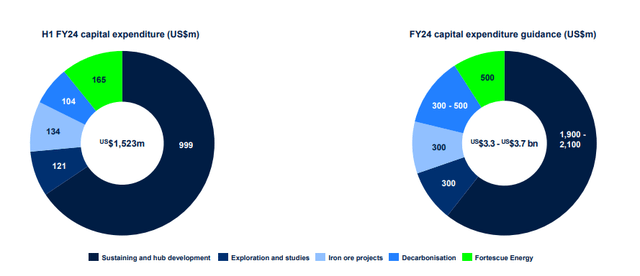

With just $1.5B in capex, the free cash flow result was approximately $2.4B. Keep in mind this includes some changes in the working capital position as well but unfortunately the company did not provide a detailed cash flow statement outlining the working capital changes. But considering the depreciation charges were just $922M while Fortescue spent $1.57B on capex and lease payments. The image below, published in the H1 presentation, also clearly indicates the sustaining capex in H1 was just $999M and is estimated to be around $2B for the entire financial year.

Fortescue Investor Relations

The average received price should increase in the near future while the capex should decrease as the Ironbridge project will contribute 22 million tonnes of higher grade concentrate per year at a C1 cash cost of US$45/wmt. As explained in my previous article, this would contribute an operating profit of just over US$1.1B per year using a benchmark price of $100/t and a 67%Fe price of $120/t.

That’s a rather conservative estimate for the premium as the current spot price for 62% Fe concentrate is US$110/t while the spot price for 65% Fe is approximately $122/t indicating a 67% Fe concentrate would currently command an even higher premium over the benchmark price.

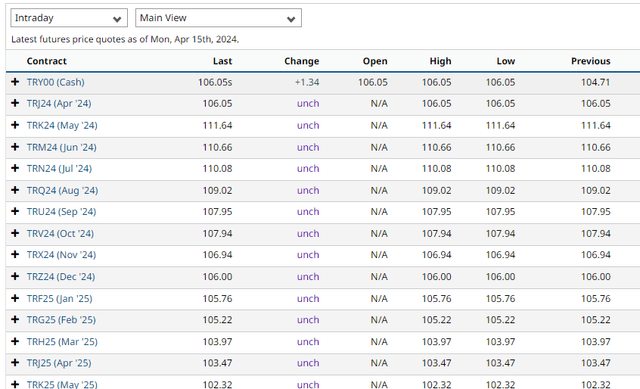

Looking at the futures market we see a slightly downwarding trend of the iron ore price but the prices are expected to remain above US$100/t for 62% Fe concentrate for the next five quarters (but of course, the futures market can change fast).

barchart.com

This means that based on the current situation, Fortescue will likely continue to print cash and may very well be able to keep its earnings above US$2/share on an annualized basis, which means the stock is trading at around 8 times earnings.

Investment thesis

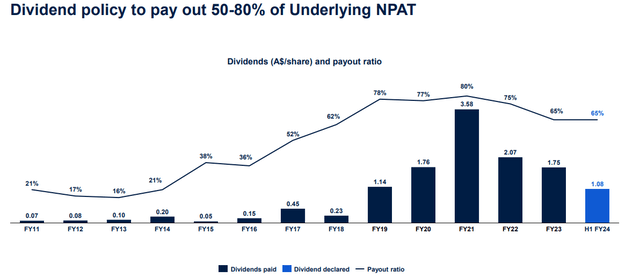

Although Fortescue Metals has been trying to diversify into copper, it is still an iron ore player. I own some Fortescue, not for the Fortescue Energy division where it expects to spend $500M on this year, but just for the iron ore price. I understand it’s a very volatile sector, so I’m not putting all my eggs in one basket, but Fortescue has plenty of experience with running large-scale operations where economies of scale are extremely important. The company has a strong history of letting its shareholders share in the wealth it creates and currently still plans to use 50-80% of its net profit to pay dividends.

Fortescue Investor Relations

That also was the case after the end of the first semester. Fortescue reported an EPS of US$1.085/share and declared a dividend of A$1.08/share which was approximately US$0.701/share for a payout ratio of approximately 65%. Due to the volatility of the iron ore price I am reluctant to call Fortescue a ‘dividend stock’ but in the past five years (since January 2019) it paid out a cumulative US$8/share in dividends. And since my March 2016 article, when the stock was trading at just US$1.87, the company has distributed about $8.65 in dividends. This means the total return in the past eight years was approximately 1,250%.

I am a happy shareholder.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")

")