")

The hawkish pivot

The Fed Chair Powell signaled that the Fed is making a hawkish turn when he spoke on April 16th. Specifically, Powell said:

Right now, given the strength of the labor market and progress on inflation so far, it’s appropriate to allow restrictive policy further time to work and let the data and the evolving outlook guide us

If higher inflation does persist, we can maintain the current level of restriction for as long as needed

Thus, I expect that the Fed will now have to officially adopt a more hawkish policy stand when they communicate their policy decision at the May FOMC meeting, on May 1st.

As a brief background, the Fed was hawkish until November 28th, 2023, which is when the Fed governor Chris Waller signaled that the Fed could start cutting interest rates, to normalize. This was a surprising dovish turn, especially given that Waller was considered to be a hawk. Even more surprisingly because only two weeks prior to Waller’s statement, Powell stated: “It would be premature to conclude with confidence that we have achieved a sufficiently restrictive stance, or to speculate on when policy might ease.”

However, shortly after, the Fed officially turned dovish at the December FOMC meeting by: 1) suggesting that the interest rate hiking cycle is over, despite the previous intent to hike one more time, and 2) signaling three interest rate cuts in 2024.

Thus, since December 2023, the Fed has been officially dovish, continuing to signal three interest rate cuts in 2024, and supporting the “soft-landing” outlook – lower inflation, and still strong labor market, and solid economic growth.

However, based on Powell’s statement on April 16th, the Fed has already made a hawkish pivot, which now has to be officially adopted by FOMC.

Why hawkish pivot?

So, why is Powell signaling a hawkish pivot? Obviously, the disinflationary process has stalled, and it looks like inflation is actually accelerating.

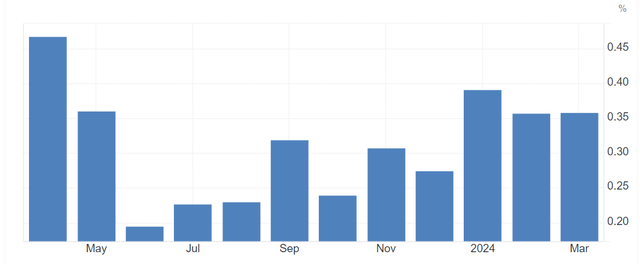

Here is the monthly core CPI inflation data. First, it’s important to understand that a monthly inflation data has to be around 0.17% to be consistent with the annual 2% inflation target. The chart below shows that monthly core CPI has “cooled” during the summer of 2023, and then really picked up during the first three months of 2024 – quarterly annualized core CPI is at 3.93%, that’s double the Fed’s target.

Core CPI monthly (Trading Economics)

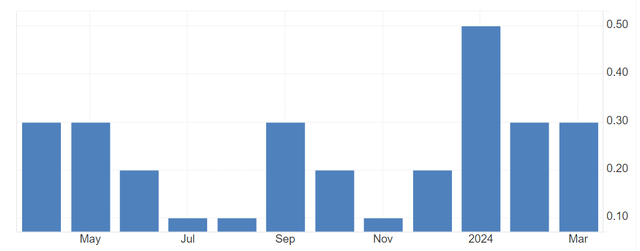

The core PCE inflation, which is the Fed’s preferred inflation measure, also follows the same pattern – after “cooling” last summer, it seems like it’s “heating” up so far in 2024.

Core PCE monthly (Trading Economics)

The Fed had remained dovish even as the core inflation started to “heat up” in 2024, embracing the “inflation bump” thesis. In this view, the current trend of higher monthly inflation is only a temporary bump and the return to the 2% target over time will be “bumpy”. Consistent with this view, the Fed still signaled three cuts for 2024 at the March FOMC meeting.

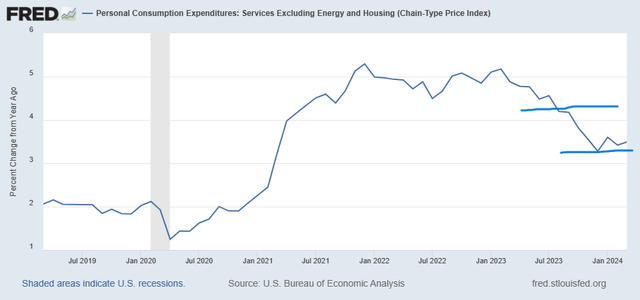

However, it appears that Powell now suggests that “the inflation bump thesis” could be rejected. So, what is the major reason for the hawkish pivot? It’s all about the core services inflation, which is the PCE inflation measure of service inflation excluding energy and shelter.

Here is the chart of Services ex Energy and Shelter inflation. First, the fact that core services inflation remained elevated and sticky from late 2021 to early 2023 was the major reason for the Fed to aggressively increase interest rates, and later embracing a hawkish “higher for longer” regime. However, during the summer and fall of 2023, core services inflation fell drastically – which was the basis for the dovish turn in December 2023.

However, core services inflation seems to have bottomed out at 3.28% in December of 2023, and now it looks like it’s rising again, currently at 3.50%.

Services ex energy and shelter (FRED)

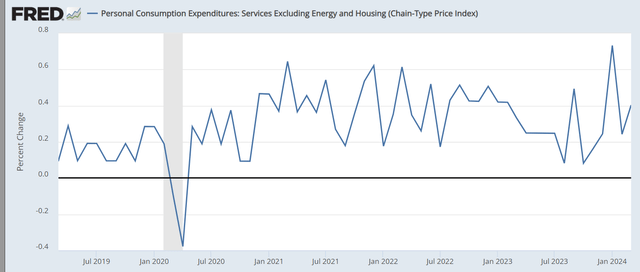

More importantly, the monthly measure of the Services ex Energy and Shelter inflation spiked to 0.73% in January 2024 – the highest level so far in this cycle, and it was at 0.4% in March, still double the Fed’s target.

Services ex energy and shelter (MoM) (FRED)

Thus, the core services inflation is on the rise, and that’s the main reason for the Fed to turn hawkish. Why is the core services inflation rising? It has to do with the tight labor market, and wage growth. The March PCE report showed that wages increased at 0.7% monthly rate – and that’s inflationary, especially for services.

Change in FOMC statement?

The Fed really wanted to cut interest rates early in 2024 (possibly due to a political motive). However, in response to the “inflation bump”, the Fed delayed the cuts in January and March, with the still dovish statement:

The Committee does not expect it will be appropriate to reduce the target range until it has gained greater confidence that inflation is moving sustainably toward 2 percent.

Now, the FOMC needs to change this statement to formalize the hawkish pivot, as signaled by Powell. I expect that the statement above will be replaced with something along the lines Powell’s statement on April 16th:

It’s appropriate to allow restrictive policy further time to work and let the data and the evolving outlook guide us.

This change would signal a return to a “higher for longer” regime, or as I interpret it is as a “higher until recession” regime. Consistently, with the change in the FOMC statement, Powell would have to be more hawkish at the post FOMC meeting press conference, by trying to explain the Fed’s hawkish turn.

Implications

History shows that the Fed needs to hold interest rates until the labor market weakens (until a recession) to restore the sustained price stability. That’s exactly what the Fed will have to do in the current cycle – hold interest rates at a restrictive level until the labor market weakens.

This implies that a recession, and with it a recessionary bear market for S&P 500 (SP500).

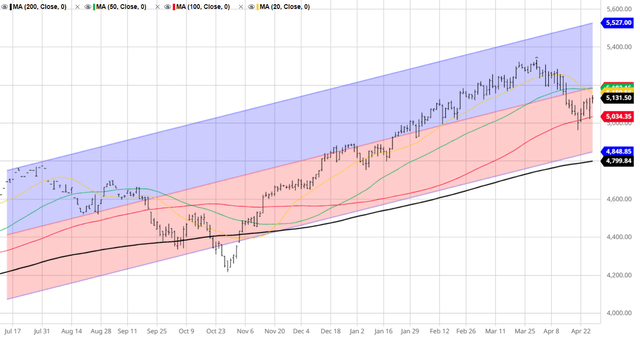

The S&P 500 (SPX) (SPY) is also likely to negatively react to the Fed’s hawkish turn. In fact, it seems like the stock market has already started to negatively price a more hawkish Fed, as predicted by the rising 2Y yields, now at 5%.

The sharp move higher from the October 2023 lows was triggered by the Fed’s dovish pivot – and the soft-landing hopes. However, the Fed’s hawkish turn officially ends the soft-landing hopes, which suggests that the recent downtrend in S&P 500 (since April 1st) has a long way to go, as the recessionary bear market unfolds.

Barchart

Q1 2024 Earnings Call Transcript")

")