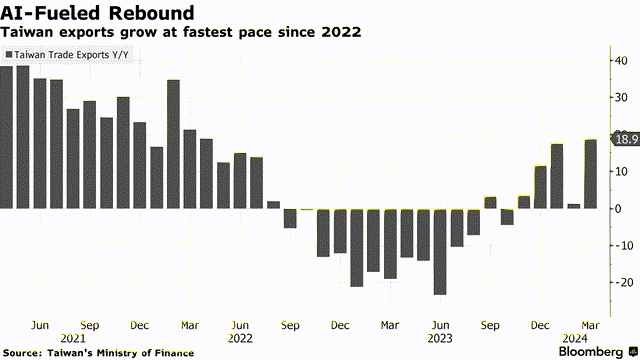

Taiwan may have seen two successive rate hike surprises (first in March and another one in June), but external demand tailwinds have been so strong that markets have outperformed anyway. Accelerating macro indicators for Taiwan’s tech-dominated equity universe, including export and industrial production data, indicate that this trend isn’t likely to slow anytime soon.

Bloomberg

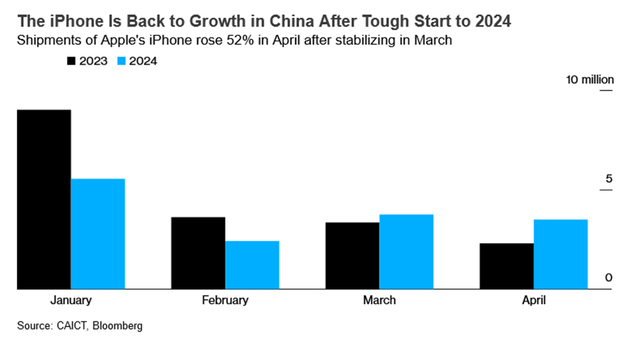

At the micro level, pipeline updates from this year’s Apple (AAPL) ‘Worldwide Developers Conference’, spanning new AI features and other product updates, further supports the case for longer-term tech momentum. And in the near term, a rebound in handset shipments bodes well for the many Apple-focused supply chain names in Franklin Templeton’s FTSE Taiwan ETF (NYSEARCA:FLTW) portfolio.

Bloomberg

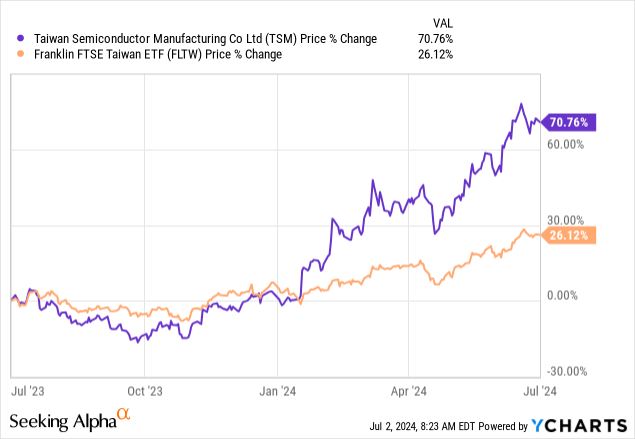

Besides the fundamental ‘picks and shovels’ tailwind, FLTW offers an interesting technical setup to boot. The key lies in how staple holding Taiwan Semiconductor Manufacturing (TSM), the world’s premier semiconductor foundry, has seen its stock not only double since last year but also outperform the other large-cap index components by a long way. The implication here is that as TSM breaches concentration limits, passive flows will rotate into the ex-TSM components at each review, boosting the other liquid Taiwanese names. By virtue of a stricter weightage cap on TSM, FLTW stands to benefit disproportionately from each rebalancing.

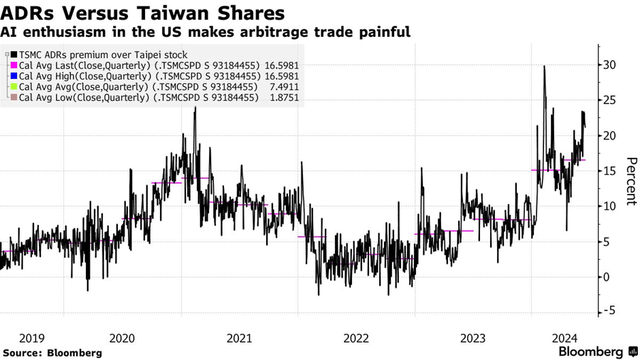

The other big technical tailwind for FLTW is its access to TSM’s Taiwan listing. For context, US-listed depositary receipts (or ‘ADRs’) have seen their premium to the equivalent Taiwan listing blow up this year – likely in reaction to TSM’s ‘picks and shovels’ AI appeal. Yet, arbitrageurs have caught on, and the current unsustainably high +20% ADR premium is bound to narrow eventually, in my view. Either way, FLTW’s exposure to the discounted Taiwan listing makes it appealing – both as a potential beneficiary of a narrowing spread and a much safer way to gain TSM exposure. In the meantime, FLTW investors get paid a well-covered low-single-digit (and growing) yield to wait.

Bloomberg

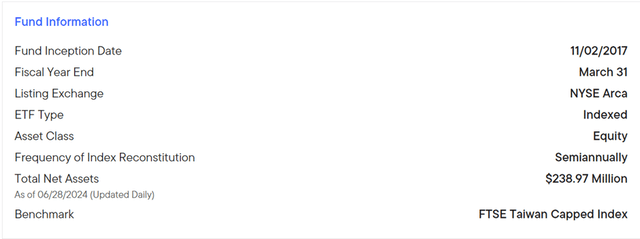

FLTW Overview – The Go-To Taiwan Vehicle for Fee-Sensitive Investors

The US-listed Franklin FTSE Taiwan ETF is one of two major US-listed large-cap Taiwanese tracker funds, the other being iShares’ MSCI Taiwan Capped ETF (EWT). Fundamentally, FLTW’s key difference is its more rigid concentration limits – particularly relevant in the Taiwanese market, where one major stock (TSMC) dominates.

Unsurprisingly, given how the Taiwan market has performed, managed assets have grown further since I last covered the fund (see FLTW: Taiwan Gets The Post-Election Green Light). But liquidity, as evidenced by a slightly wider ~9bps bid/ask spread, hasn’t improved quite as much. In combination with its industry-low fee structure (~0.2% expense ratio vs ~0.6% for EWT), though, FLTW retains its cost advantage by a clear margin.

Franklin Templeton

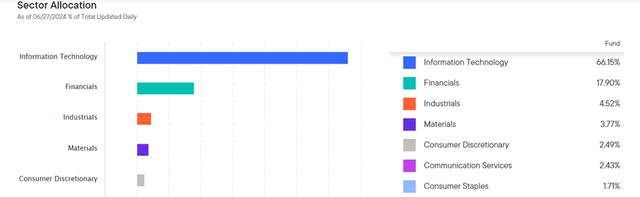

FLTW Portfolio – Tech Heavy but with Limits

FLTW may have added to its 124-stock portfolio this quarter (vs. 90 holdings for EWT), but its sector exposure to Information Technology has reached a larger-than-ever 66.2%. The other major sector allocation, Financials, is also up to 17.9%, while Industrials and Materials are down to 4.5% and 3.8%, respectively. From a sector perspective, FLTW is now the more top-heavy of the two Taiwan ETFs, so investors should continue to be mindful of the concentration risks.

Franklin Templeton

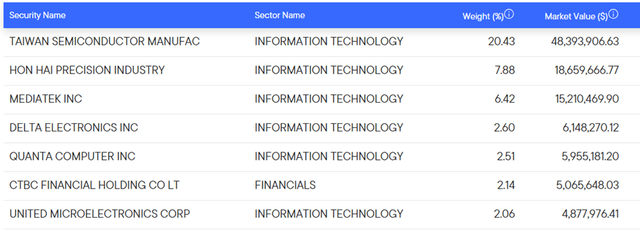

FLTW is, however, the more diversified option at the single-stock level. Its largest allocation, Taiwan Semiconductor Manufacturing, continues to bump up against the 20% cap, though a semi-annual rebalancing process helps with the position sizing. By comparison, EWT, by virtue of its less rigid weightage caps, has a slightly larger TSM allocation at ~24%.

The rest of FLTW’s major holdings gain a bigger allocation as a result of the TSM cap, with weightings for tech supply chain names like Hon Hai Precision (OTCPK:HNHPF) (7.9%) and MediaTek (OTCPK:MDTTF) (6.4%) running slightly higher than EWT. In essence, FLTW investors benefit not only from a more balanced cross-section of Taiwan but also from flows rotating out of TSM (and into the rest of Taiwan tech) at upcoming rebalancing exercises.

Franklin Templeton

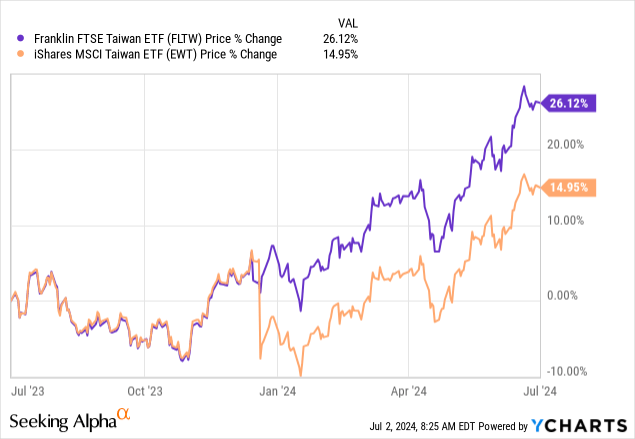

FLTW Performance – The Upward Momentum Extends into 2024

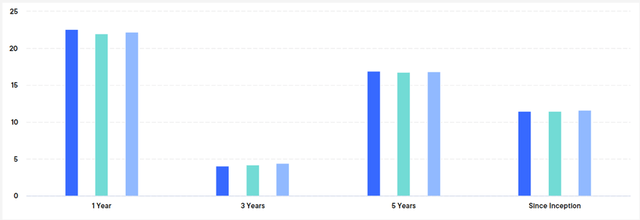

After a standout 2023, which saw FLTW return low-double-digits, the fund is once again on a red hot streak this year. Helped by a Q2 surge, the fund has now returned +18.2% year-to-date (+18.6% total return at NAV) – despite a shaky start to the year amid election uncertainties. Note that FLTW is also ahead of EWT by around one percentage point to date and by a much larger margin over the last year. Thus, purely from a performance standpoint, FLTW has been the pick of the Taiwanese large-cap ETFs.

To be clear, this delta isn’t a one-off. Over longer three and five-year timelines, FLTW has compounded at a slightly higher pace than EWT, highlighting the advantages of its broader, more diversified approach to portfolio construction.

Franklin Templeton

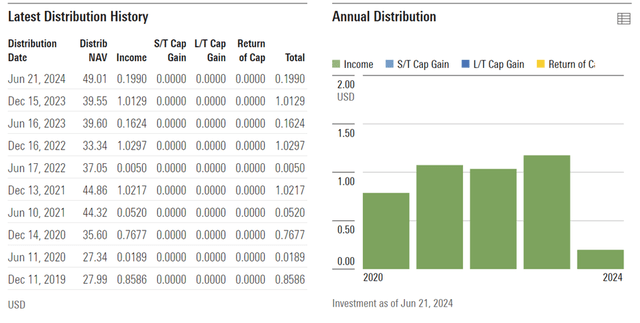

Having rallied strongly this year, FLTW’s distribution yield is also lower, though, at ~2.5%. But with Taiwanese large-caps poised to ride some very attractive near and long-term tech tailwinds, the case for further earnings growth and, by extension, dividend growth is as strong as it’s ever been.

Morningstar

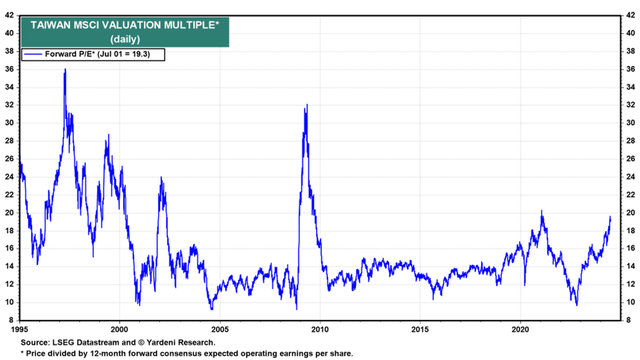

The higher June payout only lends support to this view, as does consensus forecasts for Taiwan earnings to grow at a region-leading +26% pace this year (high-teens % in 2025/2026). So, while the fund isn’t optically cheap at ~21x trailing earnings (~19x forward P/E for MSCI Taiwan), there remains ample room here for FLTW to grow into its valuation over time.

Yardeni

Ride the Tech Tailwinds with Taiwan

Taiwanese stocks have gone from strength to strength post-election, and deservedly so, given the way earnings growth is pacing. Both macro (export, production) and micro (handset shipment) indicators point to more momentum going forward as well, so this rally likely still has legs. As the lowest cost and highest returning passive fund, tech-heavy FLTW screens attractively from a fundamental perspective, though the technical setup, by virtue of its access to discounted Taiwan listings, makes it particularly interesting as well. Net-net, I remain upbeat on this tech-heavy fund.

")

")