")

Dear readers/followers,

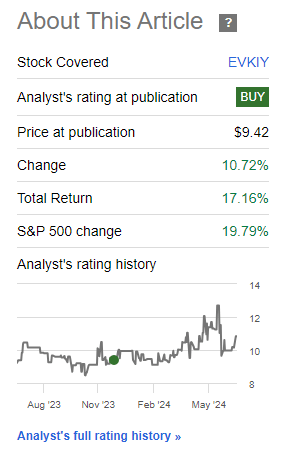

Back in December, I wrote my last article on Evonik Industries (OTCPK:EVKIY) (OTCPK:EVKIF) which I intend to update here. The company, at the time and today, has been a very volatile sort of investment. This shouldn’t surprise you if you follow the company – there’s a lot of volatility to the stock and where It could go, given its operational specifics. 3Q and 4Q23 were good, and the company has grown since that time. In fact, since I posted my last article almost 7-8 months ago, I’ve been up quite a bit since then, almost 19% including FX, but that isn’t unfortunately more than the market since then. Still, a good result in a volatile company, with plenty of more to come. If you look at the native, the figures are a bit different, with a total return of 21.65% and an average price change of 15%.

Seeking Alpha Evonik RoR (Seeking Alpha Evonik RoR)

Evonik is an interesting investment. You can find my overall case on the company here, with that aforementioned latest article. Part of why the company is so volatile is that Evonik is undergoing a strategic realignment of its portfolio and investing in future technologies. This could in turn lead to long-term growth opportunities, which is one of the long-term components of this investment.

In this article, we’ll check if the overall thesis for Evonik still holds, and if this is an attractive investment in today’s market environment.

Evonik – I like volatile chemical/materials companies that come with safety

I made it clear in my last article that despite good trends, the company left 2023 with an EPS drop and more volatile expectations than perhaps I initially thought. Still, we did not buy at over €30/share, as some investors did, but have an average buy-in cost basis of below €20/share. This means that I believe I bought the company close to the right price. Even today, inclusive also of FX and dividends, I am very much in the green with this investment.

The cyclicality of Evonik Industries has never been in question – but being cyclical also means that it will cycle up once again – and the question of timing here is the significant one.

Evonik IR (Evonik IR)

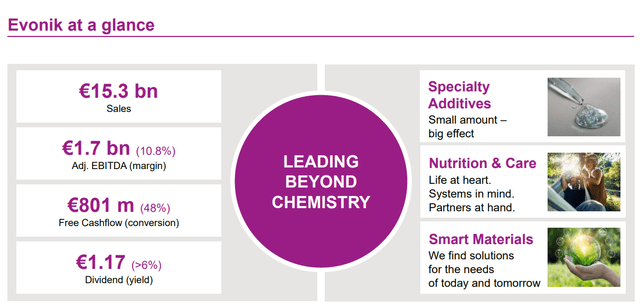

Despite currently negative trends, Evonik still yields over 6% in a market where 6-8% is good for a strong company – and Evonik remains a strong company. With a BBB+ credit rating, and less than 26% long-term debt to cap, it remains one of the strongest specialty chemical companies that I invest in, even at “just” a market cap of around €9B.

There’s also no doubt in my mind that Evonik is still undervalued. The company remains majority-owned by RAG-Stiftung, and debuted as a conglomerate with both energy and RE divisions – but most of the non-core non-chemical businesses were quickly sold off.

End-markets remain clear – consumer care, cyclical automotive, and nutrition are the primary end-market users of products. We have 1Q24 to look at, and this is as follows. As you can see in the share price, we saw a very significant bounce in the company share price – and this has to do with results.

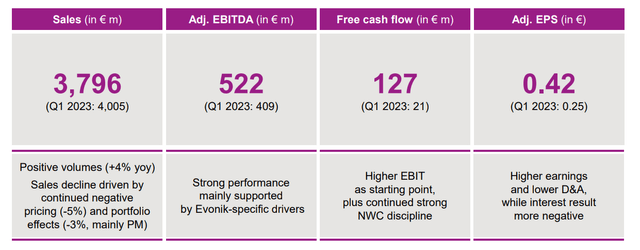

Evonik managed adjusted EBITDA well above previous-year levels, coming as high as 28% above YoY, and this is despite almost zero macro support for such a move. The drivers of this excellent performance were a solid trend in Nutrition & Care, and Animal Nutrition going strong, with very strong trends in Care Solutions as well as Specialty additives due to volume normalization.

Evonik IR (Evonik IR)

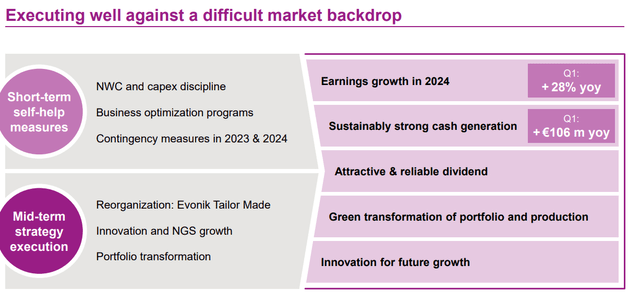

Above this, the company’s transformation is very much on track, ramping up for the €400M worth of savings target, and generating €127M worth of free cash flow during the first quarter.

The company has confirmed an outlook for the year of around €2B in company EBITDA, with 2Q expected to be in line with 1Q. All of this is very positive. We can break this upside down further, to see that yes, in fact, all things the company is doing are “working” here in driving value to EBITDA.

Evonik IR (Evonik IR)

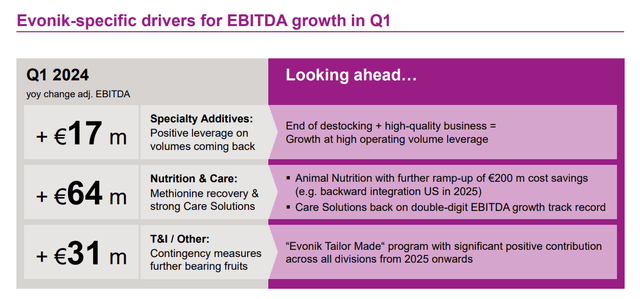

The company’s continued growth in EBITDA margins is supported by operating volume leverages, contingency plans against further downturns, and the fact that pricing is still below the levels that the company expects it to be.

This is what drove an FCF that was 5x the level it was during the YoY period. Evonik has also done some truly superb working capital management, and this is despite restocking needs. Even though CapEx is actually higher, the company still managed this sort of solid performance.

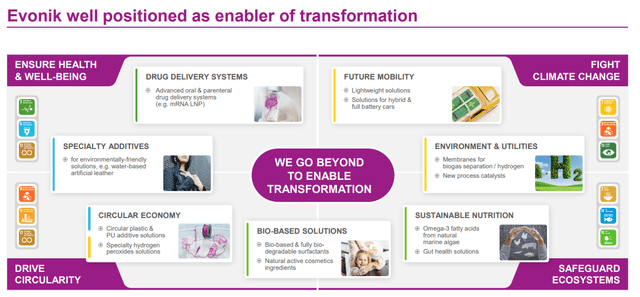

Evonik remains well-positioned going forward, as well, to capitalize on being an enabler of the ongoing transformation across multiple sectors and industries.

Evonik IR (Evonik IR)

Targets here include expansion of the Cosmetic solutions portfolio, Healthcare solutions, and Membranes, for a mix of cosmetics, mRNA therapies, and the separation of biogas and extraction of hydrogen, with new capacities coming online in the coming few years.

I want to mention at this point how very impressive company trends with things like CapEx are, where despite inflation and the need for investment, Evonik has reduced its CapEx as a percentage of sales from 6.7% in 2019 to less than 4.8% in 2024E. This largely has to do with the completion of large CapEx-intensive projects, and the current low asset utilization rates due to macro enabling growth without new investment – provided that your assets are flexible, of course. The company also uses more of a targeted approach, requiring government support before going into new fields – like lipids in the US and aluminum oxide in Japan.

Going forward, Evonik targets a continued FCF conversion of about 40% and is in the process of building up the right circumstances for this to be possible. They have, among other things, lowered bonus payments, improved NWC, lowered taxes, and continued CapEx discipline. I like what the company has done in cost control here, and against what sort of context the company has performed. It means that when things improve, we’re likely to go even higher.

Evonik IR (Evonik IR)

The company’s assumptions and targets for the 2024E period continue to be positive in nature, with changes only really in raw material assumptions. This leads me to talk a bit about the risks and overall upsides to the company if you were to invest here.

Risks & Upsides to Evonik

Obviously, valuation is the central factor – but a few other things exist. The risks to Evonik are, as I see them, mixed. First of all, if you follow the press news for the majority owner, the RAF Stiftung, they intend to reduce their exposure to Evonik to 25% over time. This will without a doubt remain an overhang on the stock until that time that such a stake is achieved. At the same time, these “absolute” sorts of targets also provide us with potential for appealing entries that perhaps disregard some of the long-term potential of the company. So it’s not “Just” a negative here.

Perhaps instead, the biggest risk to Evonik is that it can’t achieve its operational goals with its current asset or operational base. It needs to either expand organically, or inorganically – and recent trading and multiples for chemical companies are not favorable for the buyers at the moment. Any acquisitions that Evonik could end up making here could dilute returns – which is obviously a negative.

Then there’s the fact that some of the company’s business units – Superabsorbers being one (used in baby care/diapers among others) – are likely to remain muted in capacity given industry overcapacity at this time.

The upside for the company is quite positive, though. The company has exposure to many attractive segments which are consumer-oriented. This in turn makes the company less exposed to cyclicality than some of its peers. Evonik has also seen plenty of success with its Methionine product, which it’s pushing to various crustacean-related industries. Also, and I’ve mentioned above, Evonik is well-positioned to take advantage of several megatrends and growth in demand for environmentally friendly products.

Let’s look at the valuation here.

Valuation for Evonik – an upside to a PT of around €27/share.

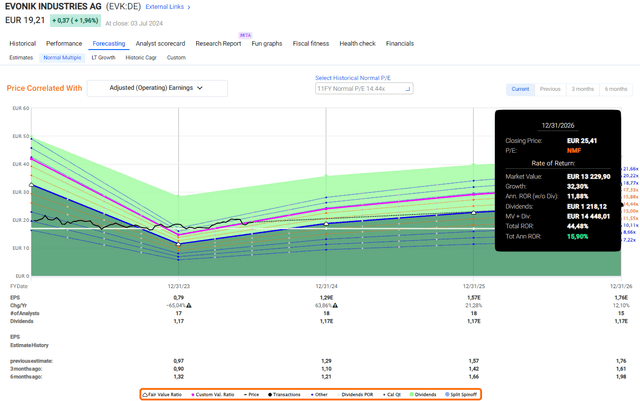

I’m still not changing my long-term price target for Evonik, which stands at €27.5/share. While growth estimates have been corrected downward, I remain firm in my conviction that reversal and growth will see, in 2024E and beyond, the company sees earnings of upward of €2/share. This to me would warrant a 14-15x P/E, which on the higher end of that assumption would come to ~€27/share, which is how I derive my share price target for the company. Even at just 14.4x P/E, the company is implied to have a 15%+ annualized upside here.

Evonik Upside RoR FAST Graphs (Evonik Upside RoR FAST Graphs)

You also have to remember that Evonik as a company has the historical tendency to outperform stated and expected targets by more than 10% at least 40% of the time on a 1-year basis (Paywalled FAST Graphs link).

So the potential for outperformance is certainly here.

2023 was a trough year. I typically add to Evonik when the company dips to, or below €18/share, but I consider it a “BUY” to anything close to at least €23/share in this market, which means that I consider It a “BUY” here.

17 analysts follow Evonik here, and most of them would say that I am being too exuberant in my targets. These targets begin at €17.5 and go all the way to €26, but with an average at around €22 (Paywalled TIKR.com link). The average from analysts, is around 13.4% upside compared to my own upside which is well over 20%. I will not consider the company to be “cheap” over €19/share, though.

We still look at peers like Linde plc (LIN), L’Air Liquide S.A. (OTCPK:AIQUY), BASF SE (OTCQX:BASFY) (OTCQX:BFFAF), Ecolab Inc. (ECL), Sika AG (OTCPK:SXYAY) (OTCPK:SKFOF), Corteva, Inc. (CTVA), and Dow Inc. (DOW). I own many of these myself, but Evonik remains in an interesting position to many of these.

As things stand now, here is my current thesis on Evonik, and it’s a “BUY”.

Thesis

- I’ve been adding more of Evonik Industries over the past few months, building my position slowly.

- I view Evonik as a substantially undervalued, quality enabler of renewables and ESG-based technology, which puts it on a trajectory for growth for the next decade and more. The yield is another big advantage here.

- I use both common share investments, and I’ve also written PUTs, taking advantage of the weakness in the share price.

- My PT for the company remains at a conservative €27.5/share, given the lack of visibility for some of the divestments and trends in 2024-2026E. I could impair it slightly given the flat expectation during this year compared to the next few, but I take a longer stance for Evonik, and that longer stance implies all “upside” to me. The company is a “BUY” here.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansions/reversions.

Evonik fulfills every single one of my investment criteria here, except for being cheap, which I no longer believe it to be.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")

")

")