")

")

Reports of my death have been greatly exaggerated – Mark Twain

Whether the quote above is a misquote or not from Mark Twain, we believe it applies well to the rooftop solar industry. It is true that the industry is facing a myriad of issues, and several smaller companies have indeed gone bankrupt. Headwinds include higher interest rates making solar system financing considerably more expensive, lobbying by utilities (XLU) where they have succeeded in making solar considerably less attractive in certain states, and then there is the risk of new import tariffs on foreign solar panels. At the start of the year, there was an article from Time magazine saying that the rooftop solar industry was on the verge of collapse. However, we believe that the industry has improved its offerings so much, that it will survive, even if economic and lobbying efforts slow it down.

Looking at Enphase Energy’s (NASDAQ:ENPH) first quarter results, it is clear that the business has been impacted by the previously mentioned headwinds. Shares plunged after it disappointed investors with an earnings miss on profits and revenues, as well as lower than expected revenue guidance for Q2. In this article, we will take a long-term view, to see if this share price correction has made shares attractive, or the price adjustment is fair.

Company Overview

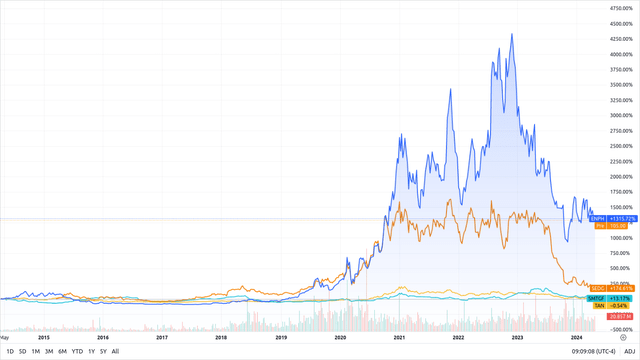

Among renewable energy companies, we find the solar inverter sector one of the most attractive parts of the industry. Solar panel manufacturers have struggled to differentiate themselves, and as a result, solar inverter companies have significantly outperformed.

For example, Enphase Energy, SolarEdge (SEDG), and SMA Solar Technologies (OTCPK:SMTGY) have outperformed by a wide margin the Invesco Solar ETF (TAN), even after their recent price declines.

Seeking Alpha

Enphase is indeed an innovation powerhouse, with over 405 patents globally, and it has been consistently developing improved products and adding functionality enabled by advanced software. It has a massive service addressable market, estimated by Wood Mackenzie and the company at $23 billion by 2025.

Enphase Investor Presentation

Q1 2024 Financial Results

Enphase has been able to deliver impressive gross profit margins and returns on invested capital thanks in part to its CAPEX-lite business model with no big factories. Headcount is also highly distributed around the world, with many employees in lower cost regions.

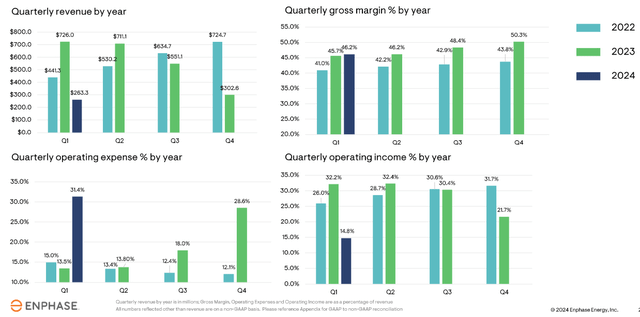

Still, its first quarter 2024 financial results were a little disappointing, with total revenue of only $263 million. The company shipped roughly 603 MW DC of micro-inverters and 75 megawatt hours of IQ Batteries. Its non-GAAP gross margin for the quarter was 46.2%, several points below the 50.3% it achieved in Q4. On the positive side, the company reduced its channel inventory by approximately $113 million. Unfortunately, this was less than expected due to softer demand.

Enphase Investor Presentation

Stock Based Compensation (SBC)

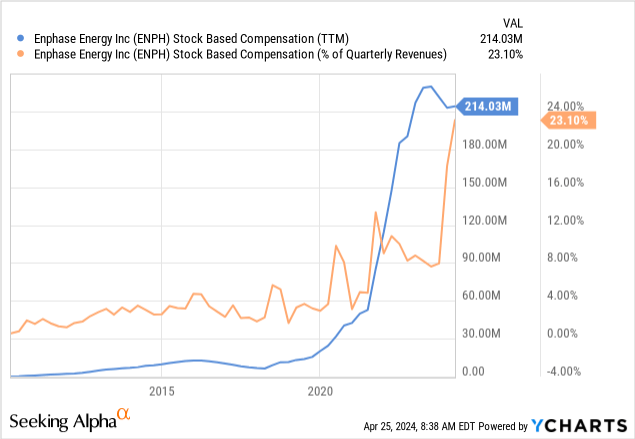

One thing we do not like about Enphase Energy is its high SBC expense, which has been climbing dramatically, both in absolute terms, and as a percentage of quarterly revenues. We believe stock-based compensation is a real expense, even if it is categorized as non-cash by the company, and helps inflate reported free cash-flow numbers.

Peers

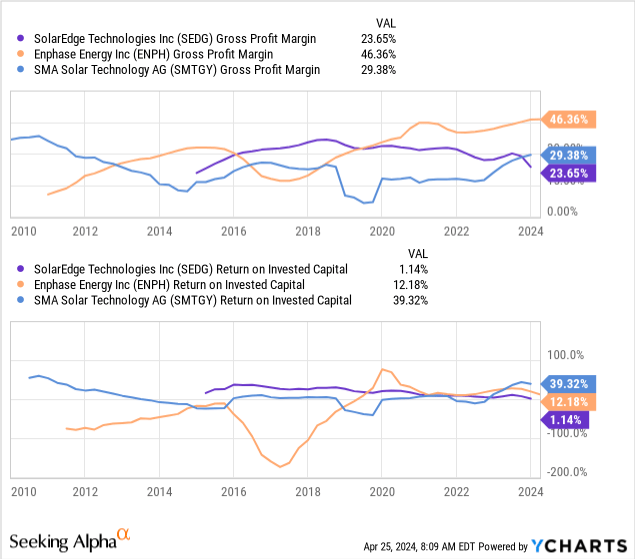

Given its strong technology, brand, distribution relationships, and CAPEX-lite business model, Enphase has been able to deliver impressive gross profit margins. These are much higher compared to competitors SMA Solar Technologies and SolarEdge Technologies.

However, with its focus on commercial and large scale customers, SMA Solar Technologies has been better positioned recently to weather the industry headwinds, as it is much less reliant on the rooftop end-market. As we wrote recently, we find its valuation and recent earnings more attractive compared to peers.

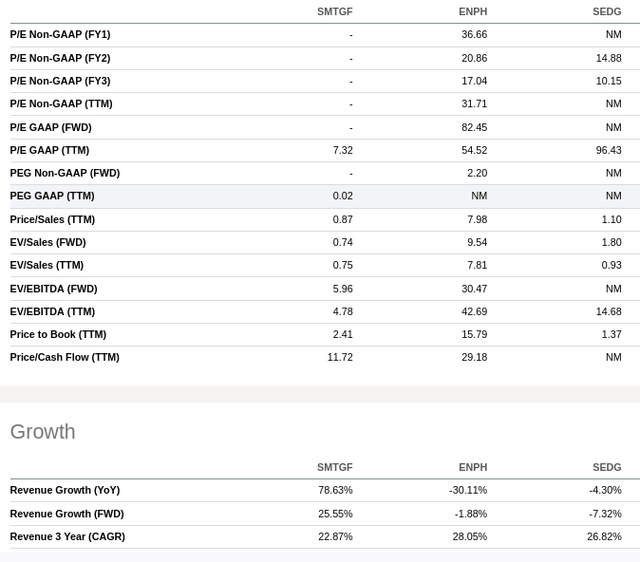

As can be seen in the table below generated using Seeking Alpha’s stock comparison tool, SMA Solar Technologies is trading at much lower valuation multiples on most metrics, and it has been delivering better growth recently too.

Seeking Alpha

M&A

We see Enphase improving its competitive moat through a series of bolt-on acquisitions that should help the company gain additional capabilities to deliver on its vision of selling complete energy systems. Below are some examples of recent transactions, as can be seen, several are either platforms or have a software element to them. They also go beyond their core solar inverter business, and include electric vehicle charging solutions and Internet of Things (IoT) software.

Enphase Investor Presentation

Future Outlook

The company’s guidance for Q2 included revenue in the range of $290 million to $330 million, and shipment of 100 megawatt hours to 120 megawatt hours of IQ Batteries. Enphase believes Q1 was probably the bottom quarter this cycle, with Europe already starting to recover, and non-California states trending positively in Q2.

In its recent earnings call, CEO Badri Kothandaraman answered an analyst question about the relatively low margins compared to previous quarters, asking if it was just a matter of product mix, or if there was something additional impacting profitability. We include below his answer to this question.

Yeah, there what I was talking on the question from Colin, which was microinverters was installer mix. That’s correct. But this question that you are asking, the 39% meaning, we guided 39% to 42% for non-GAAP gross margin without IRA in Q2. Your question is why? And yes, we increased our battery guidance by 30 megawatt hours. As you can see, Q1 guidance was 70 megawatt hours to 90 megawatt hours. We increased 100 megawatt hours to 120 megawatt hours. That means we are — the battery to microinverter ratio is increasing from before. We are getting a — we are getting better and better and better on the gross margin of batteries, and you’ll see those numbers continuously improve.

On batteries specifically, I called out three factors. I said the cell pack costs are continuing to come down rapidly. We are beginning to manufacture now our microinverters, which are used in the battery. We are beginning to manufacture them in the US. Those will provide us with the production tax credit, which is exactly the intention that we need to produce that product in the US, the inverter is made in the battery. And then, the last one, which is exciting one is where we are moving to a more integrated architecture for power conversion and battery management.

And basically, what’s going to happen is our third-generation battery, the Y direction is going to almost get cut by 40%, and instead of six microinverters that we have in the third-generation battery, we will now have two microinverters, one on each side of the fourth-generation battery significantly cutting down the form factor. So, we expect that to bring in another big level of improvement in gross margin. So, those are the gross margin puts and takes on our batteries.

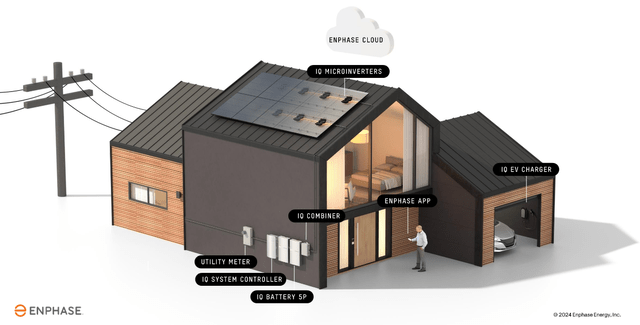

Looking further ahead, the company does sell a very compelling vision where they will offer complete home energy systems, not only micro-inverters and batteries. This will include home energy management software, mobile apps, and even bi-directional electric vehicle (EV) chargers. The vision is to increase the “share of wallet” per customer, from around $2,000 to more than $12,000 per home. They are already taking some steps in this direction, with their next software offering already managing dynamic tariffs in countries like the Netherlands and Germany.

Enphase Investor Presentation

Valuation

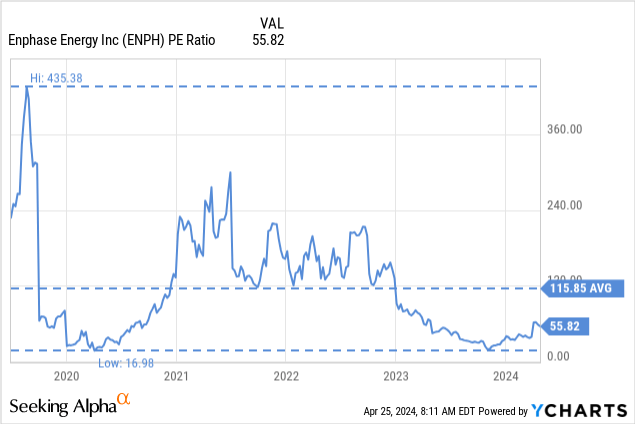

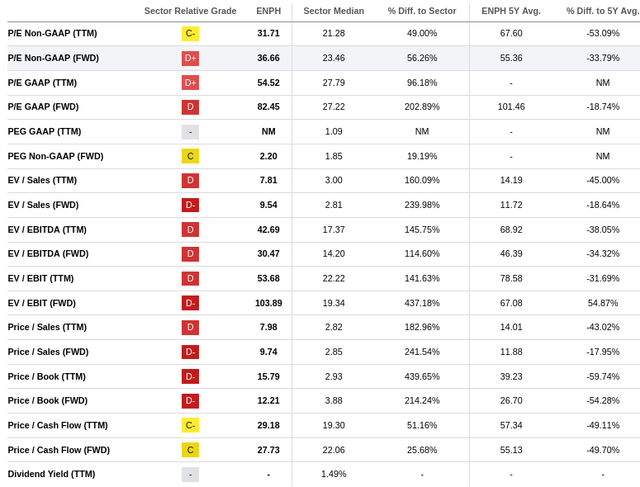

While Enphase has been trading at elevated Price/Earning multiples for several years, this ratio remains high in absolute terms. It will become much harder to justify if high growth is not reignited soon. Despite trading at less than half the five-year average, a 55x P/E reflects significant growth expectations.

Looking at the valuation section in Seeking Alpha, it is difficult to find any valuation metric that does not point to overvaluation. Even the Price/Earnings to Growth ratio, which should be deflated by the high growth expectations, is above 2.0, which is generally considered expensive.

Seeking Alpha

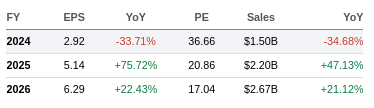

On average, analysts are expecting a very significant earnings improvement for 2025, and the FY26 expected P/E is around 17x. Given the headwinds in the sector we are not convinced the company will be able to deliver these levels of earnings. There is also the issue that analyst estimates are non-GAAP, and we should remember that Enphase has very elevated SBC.

Seeking Alpha

Using average analyst estimates for the next three years, and then assuming 11% EPS growth through 2034, we calculate a net present value for the shares of $110. This is very close to the current share price, and does not provide an attractive enough valuation margin of safety.

| EPS | Discounted @ 10% | |

| FY 24E | 2.92 | 2.65 |

| FY 25E | 5.14 | 4.25 |

| FY 26E | 6.29 | 4.73 |

| FY 27E | 6.98 | 4.77 |

| FY 28E | 7.75 | 4.81 |

| FY 29E | 8.60 | 4.86 |

| FY 30E | 9.55 | 4.90 |

| FY 31E | 10.60 | 4.94 |

| FY 32E | 11.76 | 4.99 |

| FY 33E | 13.06 | 5.03 |

| FY 34E | 14.50 | 5.08 |

| Terminal Value @ 3% terminal growth | 186.56 | 59.44 |

| NPV | $110.46 |

Risks

We see several risks for Enphase, including a high revenue concentration in the U.S. market, which represented 57% of Q1 revenue. The residential rooftop market has been struggling with high interest rates and regulatory changes. In the earnings call the company reported having “visited over 25 installers in California to really understand how their businesses are doing. Many reported that their businesses are down by 50% or more from last year’s high”.

Conclusion

Enphase remains a company at the top of our watchlist, but we would require a significantly more attractive valuation and valuation margin of safety to buy shares.

The company has industry leading gross margins and attractive ROICs given its CAPEX-lite business model. It also has a large addressable market that could enable significant growth to continue for several more years. There are also significant risks, including significant issues in the U.S. residential solar end-market. We are therefore maintaining our “Hold” rating after reviewing the most recent earnings results.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.