Q1 2024 Earnings Call Transcript")

")

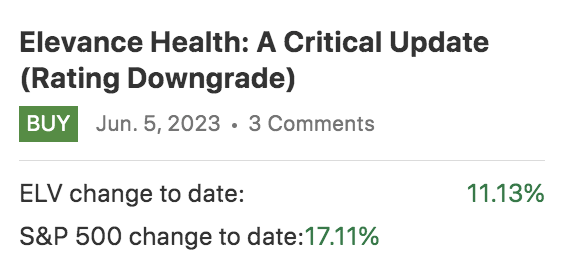

This article dials in on Elevance Health, Inc. (NYSE:ELV), a U.S.-based long-term insurance health company whose stock we last covered in June. Although we maintained our bullish outlook, our previous Elevance Health article downgraded the stock to a buy rating from a previous strong buy rating.

As visible in the diagram below, the rating more or less ticked all the boxes as Elevance Health returned about 11%. However, it is time to revise Elevance Health’s prospects, especially considering its first-quarter earnings beat.

Our Previous ELV Rating (Seeking Alpha)

Here are our latest findings on Elevance Health.

Elevance Health’s Q1 Earnings & Outlook

Earnings Release Summary

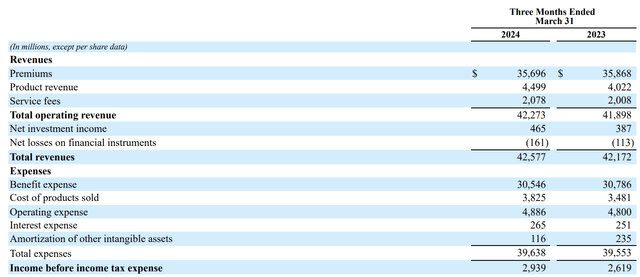

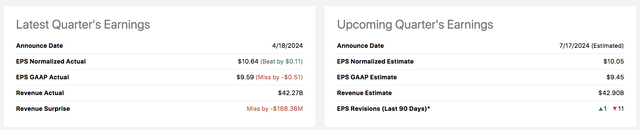

Elevance Health released its first-quarter earnings report last week, revealing staggering results. The long-term insurance firm achieved $42.58 billion in quarterly revenue, beating estimates by $140 million. Additionally, Elevance Health’s non-GAAP quarterly earnings-per-share settled at $10.64, beating estimates by 11 cents.

A more detailed look at Elevance showed a combination of enhanced net insurance profits (not net income statement profit) as the company’s benefits ratio improved by 20 basis points in the quarter to 85.6. Moreover, related operating costs softened as Elevance Health’s expense ratio dropped by 10 basis points to 11.4. However, note that non-core costs, such as acquisition and integration expenses, drove this metric up to 11.6 in Q1.

Lastly, Elevance expects its diluted net income per share to settle at $34.05 in 2024 and $37.20 on an adjusted basis (meaning non-core costs are excluded).

Our Key Takeaways & Outlook

Let’s traverse into our key takeaways from Elevance’s Q1 results. This section is divided into three sub-sections, namely premiums, investments, and other offerings.

Premiums

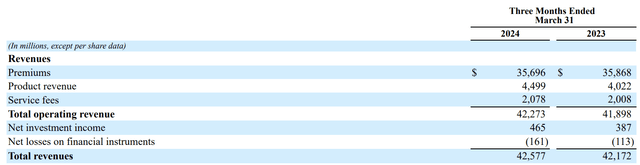

As visible in the following diagram, Elevance Health’s Q1 premiums revenue dropped slightly from Q4.

Elevance Health 10-K

In our previous analysis of Elevance, we accurately forecasted a more subdued premiums-based revenue. However, a tradeoff exists for the rest of the year.

The tradeoff I’m referring to is potential price softening paired with lower operating costs. You see, insurance pricing is cyclical (especially life & health insurance); therefore, today’s hard pricing environment could soon lead to softer prices amid rising competition. Moreover, the U.S. 10-year yield has dropped significantly in the past six months, suggesting a pivot in short-term interest rates is nearing. A pivot will likely decrease demand for fixed-rate products such as annuities (which often use the prevailing 10-year yield to peg a rate of return).

St. Louis Fed

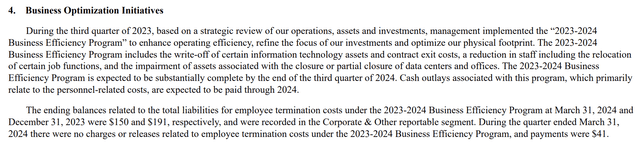

Despite its implied gross income pressures, Elevance Health’s net income from premiums could proliferate. We base this on two reasons, namely, a planned labor force reduction and a softer labor market overall.

As visible in the following diagram, Elevance Health decided toward the back end of last year that it would reduce or at least reallocate its labor. In our view, this message means the firm aims to reduce its labor force, commissions, and salaries. Moreover, the rise in AI will likely introduce a lower need for labor in certain areas.

Elevance 10-K

We just covered cost dynamics and essentially argued that Elevance would go to great lengths to maintain its cost ratios. However, the variability of insurance claims means that Elevance’s benefits ratio is difficult to forecast, meaning we have no input in that regard.

In summary, we anticipate that Elevance Health’s premiums business may experience a decline in gross income. Although potential cost reductions could help alleviate some of the pressure, we are uncertain about the extent to which this will mitigate Elevance’s implied gross income risks.

Investments

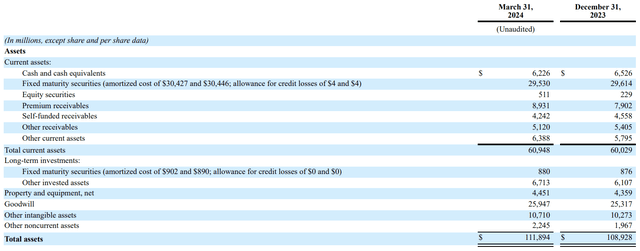

If you scroll back up to the income statement, you’ll see that Elevance’s investments generate a small portion of its income (around 1%). However, Elevance’s investments play a more prominent role than most believe, as they span about 6.8% of the firm’s total assets. Moreover, insurers often allocate more capital toward investments whenever the insurance pricing environment stalls (which we think will occur).

Assets (Elevance 10-K)

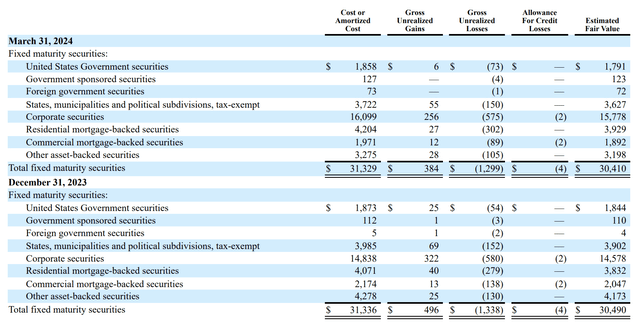

Elevance’s investment assets primarily consist of mortgage-backed securities and corporate securities. Most of these securities and Elevance’s other securities are held to maturity, meaning their incremental unrealized gains and losses are usually not deducted from the firm’s profit and loss statement. However, value fluctuations do influence Elevance’s balance sheet.

Investments (Elevance 10-K)

Our general outlook on mortgage-backed securities and corporate securities is bearish. We believe that lower interest rates will eventually become a reality, concurrently leading to higher credit spreads and mortgage prepayments. Such a scenario could introduce significant valuation headwinds.

Other Offerings

This section focuses on Elevance’s various services and product segments, with a particular focus on Carelon. Carelon is expected to drive significant growth in Elevance’s revenue mix. The company is well-positioned to benefit from an enhanced AI ecosystem. Furthermore, Carelon serves as a growth-by-acquisition vehicle for Elevance, offering synergistic advantages that can be applied across the entire firm.

Elevance’s recent activity demonstrates the company’s strong commitment to Carelon. For instance, in Q1, Carelon acquired Paragon Healthcare, which provides infusion services and injectable therapies. Paragon caters to over 35,000 patients through 40 infusion centers, thereby offering significant end-market potential and cross-selling opportunities. Although the amount paid for Paragon has not been disclosed, sources suggest that it could exceed $1 billion in all-in costs.

While service revenues did not show much momentum in Q1, we believe that long-term synergies and revenue diversification opportunities will enhance Elevance’s prospects.

Elevance 10-K

Quantitative Earnings Metrics

With the aforementioned considered, it’s time to deliver a verdict on Elevance’s earnings prospects.

Based on our analysis, Elevance’s earnings are likely to decrease in the next few quarters. However, analysts have already factored in similar circumstances. For instance, Elevance’s anticipated GAAP-adjusted earnings-per-share (EPS) of $9.45 is noticeably lower than its previous GAAP EPS of $9.59. Therefore, a softer earnings environment is probable and is likely reflected in Elevance’s current stock price.

Seeking Alpha

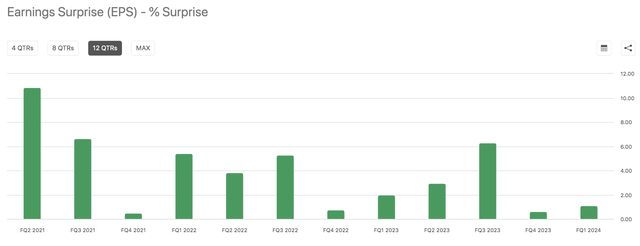

Furthermore, Elevance has a reputation as an earnings beater. The firm has surpassed its quarterly EPS estimates in its last 12 quarters, which is certainly something to be aware of if you’re an interested/existing investor.

Seeking Alpha

In a nutshell, we think Elevance will deliver lower Q2 earnings. However, we recognize Elevance’s cunning ability to surprise analyst estimates.

Valuation and Dividends

The question now becomes: Is Elevance Health’s stock undervalued?

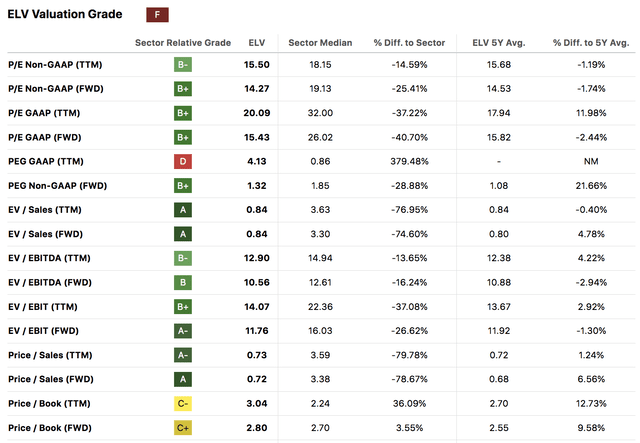

The stock’s key metrics suggest it is relatively undervalued on a sectoral basis. However, we remain concerned about Elevance Health’s salient price multiples being in line with their five-year averages as they communicate little time-series relative value. Moreover, Elevance’s GAAP PEG ratio of 4.13x communicates slow EPS growth versus P/E growth, meaning Elevance’s GAAP P/E ratio of 20.09x probably isn’t as well-placed as meets the eye.

Seeking Alpha

An absolute valuation outlook of Elevance Health coincides with its relative valuation multiples.

A P/E expansion formula was used to set a December 2024 price target, whereby we multiplied Elevance’s 5-year average forward P/E (non-GAAP) with its December 2024 EPS outlook. Our calculations led to a price target of $541, which is near its current market price (the stock opened at $530.11 on Friday, 22 April).

Seeking Alpha

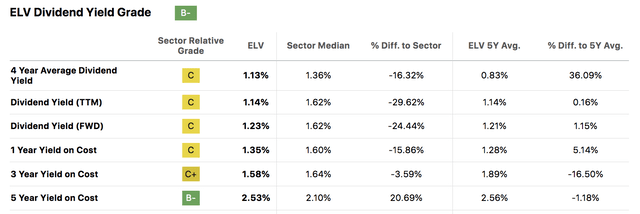

You might’ve realized by now that we consider Elevance Health fairly valued. Well, we don’t consider its dividend prospects ideal either. Elevance has a forward dividend yield of 1.36% and a 5-year average yield on cost of 2.53%. We don’t think these values convey lucrative income or add a floor to Elevance’s stock price.

Seeking Alpha

Final Word

Our latest analysis of Elevance Health dialed in on its Q1 earnings report in an attempt to revise our outlook on the stock. Although Elevance’s stock didn’t react adversely to its Q1 report, key variables suggest risks loom.

In our view, a softer insurance pricing environment lies ahead. Moreover, subdued investment performance is likely, which doesn’t bode well with Elevance’s valuation metrics, which suggest the stock already priced this in.

Although positives, such as developments in Carelon and frequent earnings target triumphs, exist, we downgrade our outlook on Elevance to Hold.

Consensus: Hold/Market Perform