Q1 2024 Earnings Call Transcript")

")

Introduction

Leggett & Platt (NYSE:LEG), a diversified manufacturer with a rich dividend history, offers a tempting 10.24% yield. This Dividend King’s diverse product portfolio across bedding, furniture, and specialized products is appealing. However, a closer look reveals a troubled core bedding segment (42% of sales) facing stiff competition and cost disadvantages. While a potential housing market recovery and a restructuring plan offer hope, the company’s heavy debt load and limited cash flow raise concerns.

Investment Case

Leggett & Platt is an old, robust, and versatile manufacturing company, as revealed in its recent 10K report. The company designs and produces a wide range of engineered components and products that are essential for many households (especially bedding products) and automobiles. Leggett & Platt’s operations span three key segments: Bedding Products, Specialized Products, and Furniture, Flooring, and Textile Products, showcasing its adaptability and resilience across diverse industries.

Bedding Products takes the biggest share of Leggett & Platt’s sales. It brought in 42% of total revenue in 2023. This segment makes innerspring units for mattresses, foam products, and complete mattresses, too. It also supplies adjustable beds to many bedding companies. They build machines used by other mattress makers as well. The Specialized Products division works with different industries like transportation and aerospace. They make car comfort systems, tubing and assemblies for aircraft, and hydraulic cylinders for various uses. Furniture, Flooring & Textile Products manufactures parts used in home and office furniture. It produces carpet cushions, underlayment for floors, and geo components used in construction.

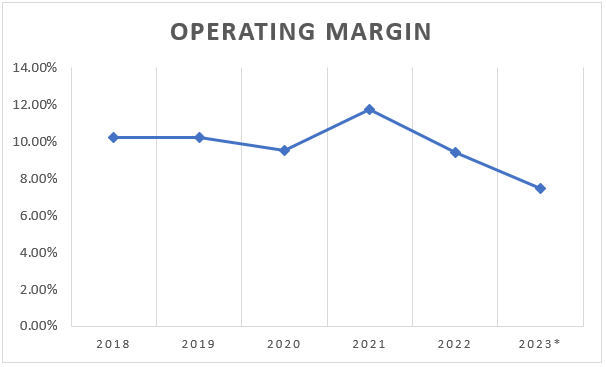

Most importantly, Leggett belongs to a group known as Dividend King, which means that the company has to increase its dividend payment yearly so as not to lose its investment category. In fact, this is true even when sales dropped by 8.2%, net income was negative, and operating margin compressed. Still, the company declared a quarter dividend increase of $0.02 per share for each common stock owned, thereby bringing the quarter dividend per share up to $0.46 and annual dividends up to $1.84. Based on current outstanding shares (133,730,089), it’s possible that the firm will spend more than $246 million in cash on dividends throughout 2024.

Though the dividend increase is there, Leggett stock continues to show weakness as its price keeps falling below pandemic lows. As I stated in my article about Flexsteel Industries, companies related to the furniture (and related products) sector have underperformed the S&P500 if we only look at what has happened to their prices. From my perspective, the main cause of the underperformance was severe competition in the market that pushed outstanding returns down, together with low industry growth, making it harder for most firms in this field to work.

Nevertheless, as I also showed in my article, furniture industry experts expect a recovery until 2024. This anticipated recovery should be associated with lower interest rates, a stronger housing market, and fewer inventories. Hence, even though Leggett may not be an attractive long-term investment opportunity, it is worth considering by income investors who want to make a quick buck because of its current FWD dividend yield of 10.24%, which outperforms most, if not all, Dividend King companies’ dividend yields.

However, the yield wouldn’t be that high without more risks. In the next section, we’ll explore Leggett’s most significant risks in the next few years.

Risks

Persistent Macroeconomic Headwinds

The future may seem brighter than 2023, but inflation remains stubbornly high above 2%. This has led financial analysts to reconsider how many interest rate cuts might happen in 2024. The high inflation data has caused risk-free interest rates to increase again, which could delay a recovery in the housing market this year. A delayed recovery could make the market more challenging for bedding products, which account for 42% of Leggett’s sales, increasing the risk of further revenue decreases.

However, management appears to be proactive. They are projecting a sales decline of around 2-8% in 2024 despite the Specialized Products segment having a high backlog and positive outlook. Work furniture is expected to remain steady, while home furniture may dip slightly. This means the Bedding and Flooring Products segments will drive the forecasted revenue decline. Nonetheless, a better-than-expected housing market could positively impact demand for these products, transforming a negative situation into a significant opportunity for revenue growth.

Cost Structure Disadvantage

According to Statista, the US bedding industry has grown at a CAGR of 5.54% since 2018, while the Bedding Group sales have grown at 17.22%, mainly due to the acquisition of ESG for $1.25 billion. Comparing 2019 to 2023, the US bedding industry rose 5.33% annually, while the Bedding Segment decreased by 3.43% annually. Leggett is losing market share because of a severe cost structure disadvantage, evident in the constant antidumping and countervailing orders on mattresses, steel wires, and innerspring imports imposed by different US government institutions to protect local production from foreign price-competitive products. Foreign producers enjoy lower labor wages than in the US, which makes Leggett US-based operations highly vulnerable to regulations and actions from foreign producers. Nevertheless, the current tendencies in re-shoring in the US may continue to bring a protective environment, so I think the company will keep its revenue at least flat in the short term as it’s protected against foreign competition.

Moreover, as bedding sales are expected to decrease and most other segments are expected to increase, its importance for company sales will decrease in the next year.

Debt

As of December 2023, the company had a debt of $1,679 million, of which $300 million is due in 2023, $186 million in 2026 and $500 million in 2027. The management expects to generate around $325-375 million in operating cash while spending $100-125 million in capex; hence, it will be barely enough to pay the estimated $246 million in dividends. I doubt any dividend cut will occur as the company is pressured to remain a dividend king company. Moreover, in the last earnings call, the management stated they feel comfortable with the current leverage ratio, so I think they will probably roll over the debt. The current debt carries a 3.8% interest rate, considerably lower than current interest rates. Therefore, the interest expense will likely increase in 2025 as debt is rolled over in a higher interest rate environment and a lower credit rating. In this sense, the coverage ratio with adjusted EBIT (excluding impairment) in 2023 was 4.26, so net interest expenses were 23.47% of operating income; higher interest rates will increase interest expenses and decrease cash available for dividends. Consequently, from my perspective, if the company doesn’t return to a growth path in the next three years, it may be unable to keep raising its dividend.

Positive Outlook

Despite the abovementioned risks, Leggett has opportunities to improve and keep raising its dividend. First, even if inflation remains higher than 2%, it is considerably down from its peak, and it’s just a matter of time until the FED begins to cut interest rates. Lower interest rates will improve the current housing market, increasing consumer confidence and spending on furniture and bedding products. In this sense, the global bedding market is expected to grow at a CAGR from 5.20% to 6%, while the US bedding market will grow at 7.3%. These expected rates are high for a mature industry and higher than the growth experienced in the last five years, so the company will face a more favorable environment.

Furthermore, in the last earnings call, the management stated that Leggett & Platt’s bedding segment is undergoing a restructuring plan to prioritize profitability. This means shifting production towards in-demand products like ComfortCore innerspring units and specialty foam while consolidating manufacturing and distribution facilities for better efficiency. The goal is to reduce costs, improve customer service through strategically located distribution centers, and align production with current and future market forecasts. While this might lead to lower volume and profitability for the steel rod mill in the short term due to less demand for Open Coil and wire grids, Leggett & Platt expects the bedding market to recover and is exploring diversifying the mill’s customer base. This restructuring prioritizes long-term sustainable growth over short-term capacity utilization.

Accordingly, the company will strengthen its weakest segment in a more favorable environment while the other segments continue to grow. Nevertheless, the results of the restructuring plan are unknown. Still, I think it’s a move in the right direction, as the company will focus on products with higher added value (such as ComfortCore) and try to develop a more favorable cost structure to remain price competitive.

Moreover, Leggett has room to recover its profitability, which may offset the adverse effects of a possible higher debt burden (higher interest rate).

Author’s Elaboration with data from 10K Reports

*Impairment cost excluded

Nonetheless, the company may face a future cash shortage to pay increasing dividends if the restructuring plan doesn’t pay off and the macroeconomic environment deteriorates, so even if I think the company will be able to pay its dividends in the next couple years, it’s highly vulnerable as it lacks a solid competitive advantage, its cash generation roughly can cover capital expenditure and dividend payments, and a higher interest rate environment may increase interest payments as old debt becomes due.

Conclusion

Leggett & Platt’s 10.24% dividend yield is a siren song for income investors. It boasts a diversified portfolio and Dividend King status, but don’t let the crown blind you to the risks. Their core bedding segment, representing 42% of sales, is losing market share due to fierce competition and cost disadvantages.

While a potential housing market recovery and a restructuring plan aimed at profitability offer glimmers of hope, Leggett & Platt walks a tightrope. The company carries a heavy debt load, and its cash flow generation barely covers dividends and capital expenditures. Rising interest rates could exacerbate this issue, potentially jeopardizing future dividend increases.

Leggett & Platt presents a gamble: high yield with high risk. Consider this – if the restructuring fails and the economic climate worsens, the company could face a cash shortage, threatening its coveted Dividend King title. Finally, I don’t think the company will be a good investment over the long term as it lacks a clear competitive advantage, but in the short term, it may be an opportunity for risk-tolerance income investors.