")

Buying companies with breakthrough science or technologies can be difficult as their stock is often priced highly with respect to its revenues, earnings, and cash flows. As much as I’d like to be on the ground floor, any time there’s excitement about a product, it’s difficult to not overpay. This is a lesson I learned with CRISPR Therapeutics AG (NASDAQ:CRSP), which has been priced highly for years in anticipation of unleashing its groundbreaking CRISPR-Cas9 gene editing technology. With two recent FDA approvals for treatment of sickle cell disease (SCD) and transfusion-dependent beta-thalassemia (TDT), one would think the stock would be reacting positively. Instead, the opposite has occurred since the beginning of the year, and I believe the drawdown is a perfect opportunity to initiate a position in CRISPR.

Background

Since its founding in 2013, it has taken just over 10 years for CRISPR, in this case with its partner Vertex Pharmaceuticals Incorporated (VRTX), to receive its first regulatory approvals, which occurred in the UK in November 2023 and the US in December 2023 and January 2024. This is an industry that moves slowly to ensure safety and efficacy for everyone’s benefit, and it has been a long road for the company, its stockholders, and more importantly its future patients. But the good news is that the pipeline is finally moving to the stage of commercialization and there are many more treatments behind these first two approvals that are moving through the various phases of clinical trials.

What have we learned from the approval of Casgevy? For starters, we learned that the FDA along with other regulatory bodies around the world will approve this class of treatments, which was not a foregone conclusion back in the fall. CRISPR-Cas9 is a revolutionary gene editing tool which enables changing a DNA sequence, a process that is a huge breakthrough but also raises significant ethical concerns. These first approvals were a major milestone in the journey of this technological advancement.

The commercial viability of these drugs is another matter entirely, and that should play out over the next couple of years, but with indications of how successful it will be in the next six to twelve months. The safest way to invest in a company like this would be to see real demand for these new treatments by patients, along with the associated revenues and cash flows. The problem is, by the time that happens, this stock will likely be much higher if it is indeed successful. I discuss the commercial viability in the risk section below, as this is one of the key factors that investors will be following in the coming quarters.

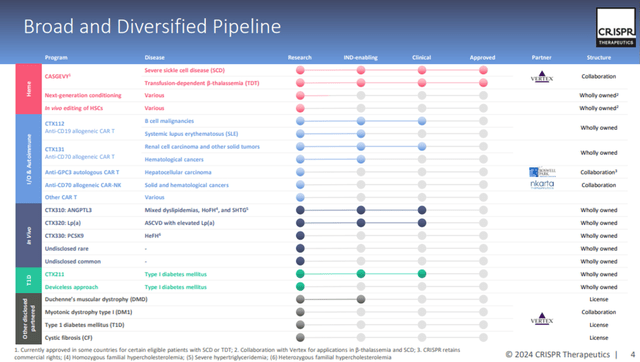

CRISPR Therapeutics isn’t about one or two treatments and approvals. However, the thesis is around a whole new way of treating a myriad of diseases. Now that the first two treatments have been approved, what else does CRISPR have in the pipeline?

CRISPR Pipeline (CRISPR Therapeutics Investor Relations)

This is where I really began to get excited about CRISPR Therapeutics. While SCD and TDT are very serious diseases and have a major impact on the lives of those that are afflicted, the number of patients expected to be treated under the current conditioning regimen is just not all that large from a financial perspective. While they are trying to broaden this population, utilizing gene editing technology in oncology or cardiovascular events expands the market size of patients significantly. That is really what an investor in CRISPR is betting on; that the approvals that we’ve seen so far can be replicated in areas with much larger addressable markets.

If CRISPR is able to break into these larger markets and offer novel treatment options for areas that have not had successful treatments before, the potential for rapid share appreciation is high. In addition, while the currently approved treatments for SCD and TDT are ex vivo, meaning the patient’s treatment must be performed outside the body which is long, painful, and complicated, CRISPR has several new treatments in their pipeline that are administered in vivo, or directly to the patient. According to the National Institute of Health, “Although some diseases are very likely to quickly benefit from CRISPR-Cas9 technology through ex vivo manner, the more profound clinical success of CRISPR-Cas9 therapeutics can only be accomplished if the system can be directly administered to patients.” From a commercial standpoint, treatment ex vivo is also driving significant costs due to the length of the conditioning. Thus, the company is exploring in vivo editing, partially funded by a $14.5 million grant from the Bill and Melinda Gates Foundation which will allow a more mass adoption of this treatment around the world.

Managing Financial Risks

Despite the binary results that often occur from an FDA submission, CRISPR has been very conservative in their operations. They have developed deep partnerships, principally with Vertex Pharmaceuticals but also with Bayer, which has given them much needed upfront funding in addition to a much larger, established company to commercialize and market the treatment. This comes at a cost, of course, in terms of the ongoing revenues that it’s ceding to its partner. But it certainly de-risks the process significantly for CRISPR and gives them much needed liquidity to continue funding these very expensive trials. CRISPR currently has enough cash on hand to finance operations for at least 24 months according to their latest 10-K filed in February. This is all happening on the cusp of real commercial revenues that will move them closer to a self-funding entity once treatments begin.

Risks

Now that we have our first FDA approvals, one risk that is off the table is the question of whether the FDA is willing to approve this class of treatments. There were some that were skeptical that gene editing would lead down a slippery slope and would make it difficult to approve. The next question is whether it is commercially viable, which is quite different and is the very essence of being a successful company. The initial list price of $2.2 million is almost unthinkable, but the counterargument is that it replaces years of expensive treatments that will cost much more over time. It will still be a tough pill to swallow for insurance companies and Medicare, but one that the company and Vertex are working on. Blue Cross Blue Shield has announced that some of its plans will cover these treatments and the Centers for Medicare and Medicaid Services has rolled out a pilot program to cover the treatments that are based on patient outcomes.

Another significant risk is competing treatments that are similar to CRISPR’s version. bluebird bio, Inc. (BLUE) has a newly approved treatment for SCD with similar efficacy, but it also comes with a “black box” safety warning and a higher price tag. Bluebird Bio’s treatment isn’t actually a gene editing treatment either, but it is similar in that its goal is a one-time treatment and “cure”, though no one can say for certain if that cure is permanent.

Aside from the competing treatment by Bluebird, there are other CRISPR/Cas-9 companies as well such as Editas Medicine, Inc. (EDIT), Intellia Therapeutics, Inc. (NTLA), and Beam Therapeutics Inc. (BEAM) that will eventually offer competing products using the same gene editing technology. I believe the market for these treatments is massive and there’s plenty of room for all these companies to be successful. I prefer CRISPR due to their strong balance sheet and as the leader in regulatory approvals at this point.

Buy the Rumor, Sell the News?

The regulatory approvals should be seen as welcome news for the stock, but the reaction this year has been anything but strong as seen by the chart below.

CRSP YTD Stock Chart (Seekingalpha.com)

While this did follow a strong run at the end of the prior year, there hasn’t been much in the way of negative company-specific news for CRISPR since the beginning of the year. That’s why I believe this is a good time to initiate a position with the stock pulling back.

What to Look for in Q1

With Q1 earnings expected at the beginning of May, I don’t think we’re going to see anything meaningful in the financial results at this point given the recency of the approvals. But I will be very interested in listening to the call, along with the Vertex call, to understand how the rollout of Casgevy is going. This is critical to not only the financial benefits of Casgevy, but also will provide insights into the commerciality of other treatments that are approved down the road. With all that being said, I have a hard time believing any information, good or bad, can really be that significant this early. Look for updates in the second half of the year for more meaningful feedback.

Valuation

How do you value a company with no consistent sales, earnings, cash flow, or other traditional metrics? I could try to come up with projections of future cash flows and discount them, a traditional valuation technique. That is very difficult to do and often very unreliable in mature companies; it’s almost impossible here as it’s pretty much guesswork. Yes, I may have some limited information in terms of market opportunity, list price and CRISPR’s share of that, but trying to project how many patients of that market they will gain, as well as the discounts off list price that will inevitably be given is unrealistic. But if I look at the market cap, which currently sits around $4.7 billion and then back out the $1.7 billion of cash, there’s only a $3 billion enterprise value which I would think would be valued at a pretty hefty multiple given the potential of future growth. It doesn’t take much cash flow, ($100m – $200m) to make this valuation seem pretty low. But again, it’s hard to predict the timing of these cash flows, and it would matter as they would need to be discounted. Some recent predictions show Casgevy reaching $1 billion in sales by 2027 and over $2 billion by the end of the decade. I don’t think anyone can say whether those predictions are right, but those are some large numbers that would throw off enough cash flow to make the current valuation enticing.

Conclusion

If all this sounds pretty speculative, that’s because it is and that’s OK. Not every investment in an investor’s portfolio has to be a consistent earnings machine that churns out profits year after year. There’s room for a more speculative play in the right sizing and I believe that CRISPR has been conservative to the extent that a company like this can be. I wouldn’t stake a huge chunk of my portfolio here, but there’s a lot of upside and this seems like the perfect time to initiate a position with the decline in the stock price in recent months.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

")