")

The VanEck CLO ETF (NYSEARCA:CLOI) focuses on investment-grade CLO tranches, sports a good 5.9% dividend yield, and has outperformed most bonds and bond sub-asset classes since inception. Although there is nothing significantly wrong with the fund, the Janus Henderson AAA CLO ETF (NYSEARCA:JAAA) is quite similar, and has a lower expense ratio of 0.20%, compared to 0.40% for CLOI. In my opinion, JAAA is stronger, cheaper choice, so I would not be investing in CLOI.

CLOs – Overview

A quick look at CLOs as an asset class before tackling the fund itself.

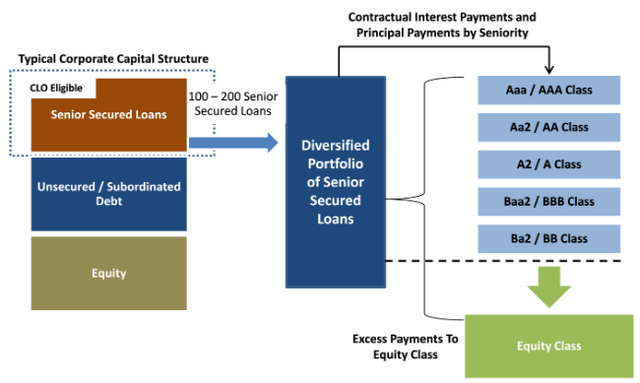

Senior secured loans are floating-rate loans from banks to medium-sized, riskier companies. These loans are senior to other debt and secured by company assets.

Senior loans are sometimes bundled together in CLOs. Each CLO, or bundle of senior loans, is divided into tranches. Income from the senior loans is used to make payments to all tranches. Senior tranches get paid first; junior tranches get paid last. CLO tranches are generally variable rate instruments, whose coupon rates fluctuate with Fed rates.

Investors can buy into these tranches and receive income from the bundle of senior loans. Quick graph of how these are structured.

Stanford Chemist SA Article

With the above in mind, let’s have a look at CLOI.

CLOI – Benefits and Investment Thesis

Extremely Low Credit Risk

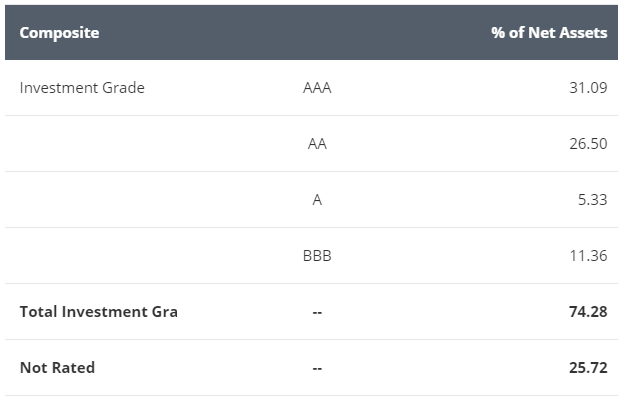

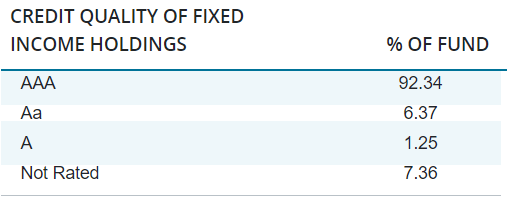

CLOI holds a diversified portfolio of CLO debt tranches, focusing on investment-grade, but with sizable non-investment grade holdings.

CLOI

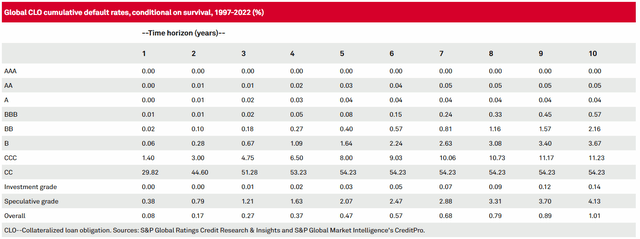

Default rates for CLOI’s underlying holdings are quite low, oscillating from effectively zero for AAA tranches, to 0.01% – 0.10% for those rated BBB.

S&P

Default rats are extremely low as the senior loans underlying these investments almost always generate enough income to make the relevant coupon / dividend payments. Default rates do increase during downturns and recessions but, in practice, rarely all that much, at least for the higher-quality CLOs which form the core of CLOI’s portfolio.

CLOI’s extremely low credit risk should lead to below-average losses during downturns and recessions, a significant benefit. As the fund is quite young, with inception in mid-2022, I can’t really gauge its performance during any such scenario. Still, I’m quite confident in my assessment.

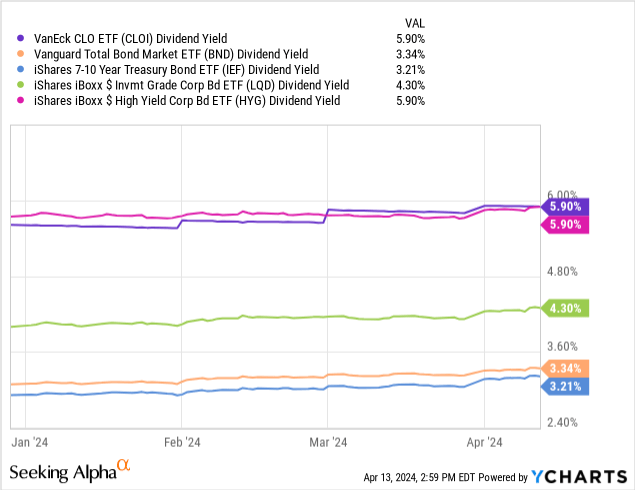

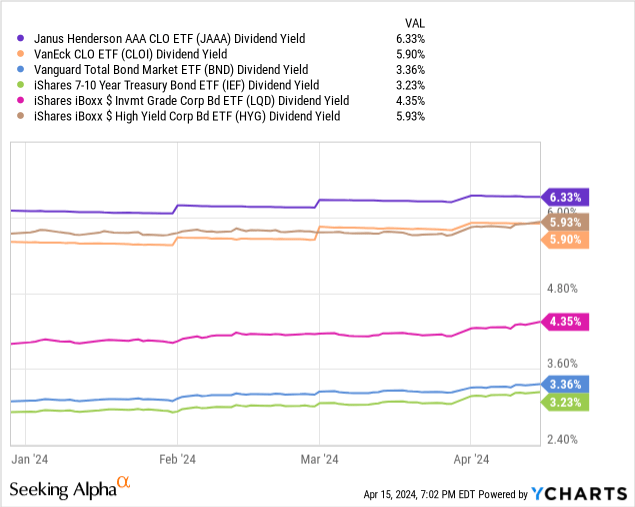

Above-Average 5.9% Dividend Yield

CLOI currently sports a 5.9% dividend yield, reasonably good on an absolute basis, and higher than that of most bonds and bond sub-asset classes, with the exception of high-yield bonds. Due remember that CLOI has much lower credit risk than the latter.

Data by YCharts

CLOI’s dividend yield seems somewhat lower than expected. JAAA focuses on similar CLOs, somewhat higher-quality, and has a higher yield.

Data by YCharts

CLOI’s underlying holdings have an average coupon of 7.5%, much higher than the fund’s dividend yield.

CLOI

I’m genuinely unsure why there is such a massive discrepancy between coupons and dividends. Part of the reason is that interest rates and coupons were lower twelve months ago, and these are TTM dividend yields. Annualizing the latest monthly dividend payment nets me a 6.8% yield, much closer to current coupon rates, although a gap remains.

In any case, CLOI’s expected returns are closer to the 7.5% coupon rate than the 5.9% dividend yield, as the coupons necessarily impact the fund and its returns. Coupons never disappear, even though these might not be reflected in dividend yields.

CLOI’s dividend yield and coupon rate are both quite good, especially considering the fund’s extremely low credit risk. Bonds with comparable yields, including high-yield bonds, tend to have high credit risk, CLOs and CLOI are something of an exception.

In my opinion, CLOI’s dividend yield is higher than those of its peers for two reasons.

First, due to perceptions of risk and illiquidity regarding CLOs. The higher quality CLOs have comparable credit risk to T-bills, but investors think they are riskier, and so demand higher yields. CLOs are less liquid than T-bills, so should trade at a spread regardless.

Second, as investors are expecting several rate cuts in the coming months, which should bring CLO yields closer to market averages (these are variable rate investments, remember). Which brings me to my next point.

Interest Rate Risk

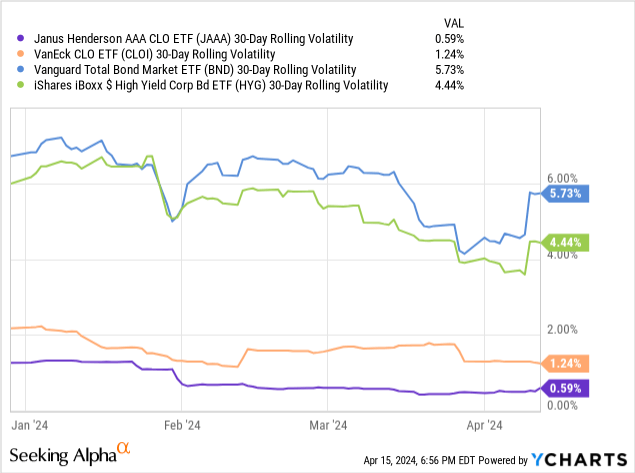

CLOs are variable rate investments with negligible interest rate risk and duration. Expect the fund to outperform when interest rates rise, as has been the case since inception. Returns were comparable to those of high-yield bonds, which have below-average duration too, albeit higher than that of CLOs.

Data by YCharts

CLOI’s negligible interest rate risk reduces portfolio risk and volatility, a straightforward benefit for investors. This is of particular relevance long-term, and when interest rates are in flux, as they currently are.

On a more negative note, CLOI’s negligible interest rate risk all but prevents significant capital gains when interest rates decrease, which could lead to underperformance. Importantly, this might not necessarily result in underperformance when the Fed cuts in the coming months, as Fed rates and market interest rates do not always move in tandem. Closest example I could find was from 2016 to 2019, during which the Fed hiked rates by more than 2.0%, and 10y treasury rates only increased by around 0.50%.

Data by YCharts

To expand on the above, market interest rates are dependent on several factors, including expectations of future Fed policy. If the market expects rate cuts in the near future, demand for longer-term treasuries could increase, leading to higher prices / lower yields in the present. This is the case right now, as evidenced by the inverted yield curve, with benchmark 10y treasury yields yielding less than T-bills.

Data by YCharts

In my opinion, and considering the above, CLO ETFs remain a buy even though the Fed is likely to cut rates in the coming months. I explained my thoughts in more detail here.

Performance Track-Record

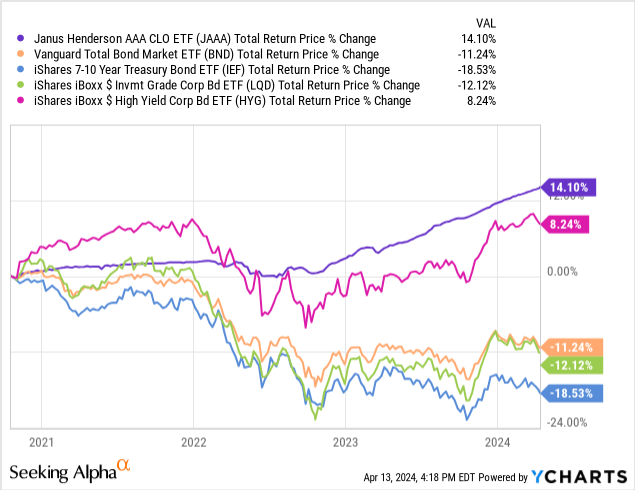

CLOI’s performance track-record is quite strong, with the fund outperforming most bonds and bond sub-asset classes since inception. Outperformance was mostly due to the fund’s low rate risk combined with interest rates rising these past two years. CLOI’s above-average yield also played a role.

Data by YCharts

On a more negative note, CLOI’s performance track-record is quite short, and excludes periods of market stress. CLOI is quite similar to JAAA though, and that fund was created in late 2020, and experienced the 2022 bear market. JAAA performed quite well during that year, and I believe the same would have been true of CLOI.

Data by YCharts

Overall, CLOI is a strong CLO ETF, but it pales in comparison with JAAA. Let’s have a quick look.

JAAA versus CLOI – Quick Comparison

Both JAAA and CLOI invest in CLO debt tranches.

JAAA focuses on those rated AAA.

JAAA

CLOI focuses on those rated AAA-AA, but holds sizable investments in lower quality CLOs.

CLOI

Although both funds have broadly low credit risk, CLOI is materially riskier in this regard, and hence more volatile. Compared to bonds and high-yield bonds both are safe, low-volatility choices though.

Data by YCharts

Both funds have negligible interest rate risk and duration.

Both funds have similar, above-average dividend yields. JAAA’s yield is slightly higher, somewhat inconsistent with their credit quality.

Data by YCharts

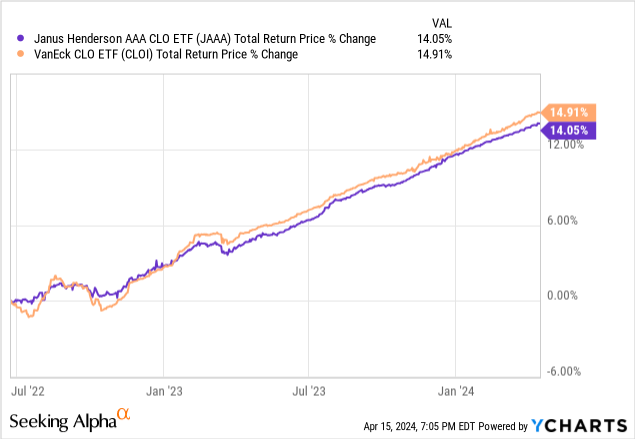

CLOI has slightly outperformed since inception, consistent with their credit quality.

Data by YCharts

CLOI’s performance has been slightly weaker than expected, due to the fund’s 0.40% expense ratio, twice that of JAAA.

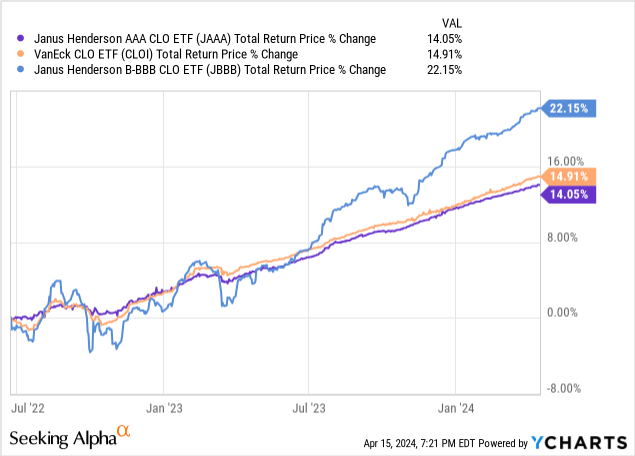

As should be clear from the above, both funds are broadly similar investments. JAAA seems stronger to me, due to the fund’s lower expenses. Although it is true that CLOI’s returns are slightly higher, this is entirely due to weaker credit quality. Investors can achieve stronger returns at comparable credit quality to CLOI by combining a significant position in JAAA with a smaller position in the Janus Henderson B-BBB CLO ETF (BATS:JBBB), which focuses on BBB-rated CLO tranches.

Data by YCharts

Conclusion

CLOI focuses on investment-grade CLO tranches, sports a good 5.9% dividend yield, and has outperformed most bonds and bond sub-asset classes since inception. Although there is nothing significantly wrong with the fund, JAAA seems like a stronger, cheaper choice. As such, I would not be investing in CLOI.

")

")