")

Introduction

One of my most successful investments in recent years is Carlisle Companies (NYSE:CSL), a stock I bought at $211 in May of last year. Since then, shares have appreciated 90%.

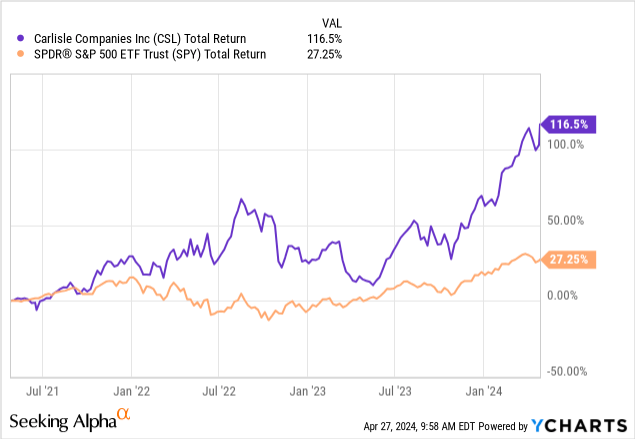

Including dividends, CSL shares have returned 117% over the past three years, beating the S&P 500 by roughly 90 points.

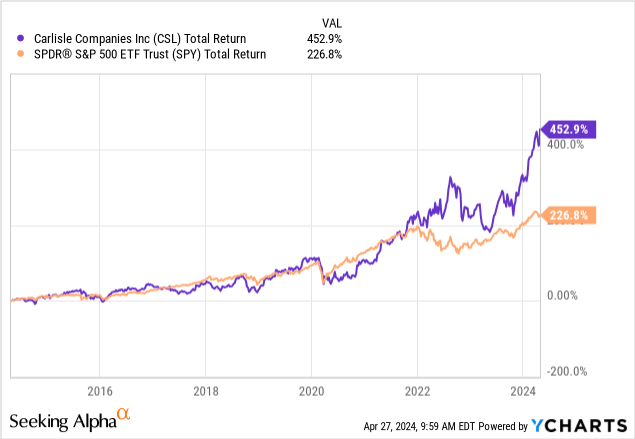

Over the past ten years, CSL has returned more than 450%, beating the S&P 500’s stellar performance by more than 200 points.

My most recent article on the company was written on December 8, when I went with the title “Carlisle Companies: A Dividend Aristocrat With A Realistic Path To >14% Annual Returns.”

The good news is that despite the company’s fantastic returns, I believe it has room to double again through 2030, boosted by significant secular growth opportunities, a streamlined business with significant growth in profitability, a healthy balance sheet, and a focus on shareholder distributions.

As the company just reported its earnings, I have a lot of new data to update my very bullish thesis.

So, without further ado, let’s get right to it!

Rapid Growth, Higher Margins, And M&A

Although its performance may suggest it, Carlisle is not a fancy technology stock. This Dividend Aristocrat, with 47 consecutive annual dividend hikes, is a giant in the building materials industry.

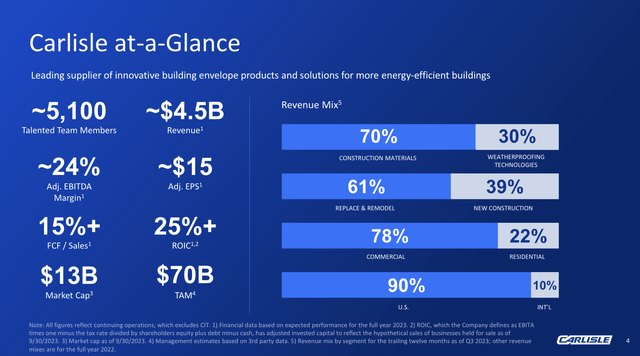

With a market cap of roughly $19 billion, the company is one of the largest suppliers of building envelope products and solutions to make buildings more energy efficient.

As we can see in the overview below, 90% of its sales are generated in the United States, where it operates two segments: Carlisle Construction Materials (“CCM”) and Carlisle Weatherproofing Technologies (“CWT”).

78% of its sales are commercial sales.

Slightly more than 60% of its sales come from replacement and remodeling projects, which is an area I am very bullish on, as the average commercial building in the United States was 53 years old in 2022!

Carlisle Companies

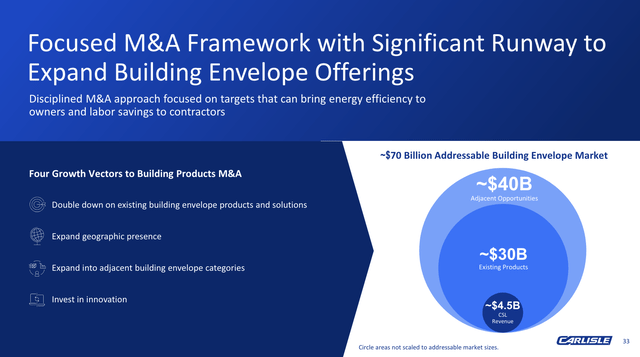

In its industry, the company has an M&A-focused strategy to improve its offerings and exploit a $70 billion total addressable market, where it currently has a market cap of less than 7%.

Carlisle Companies

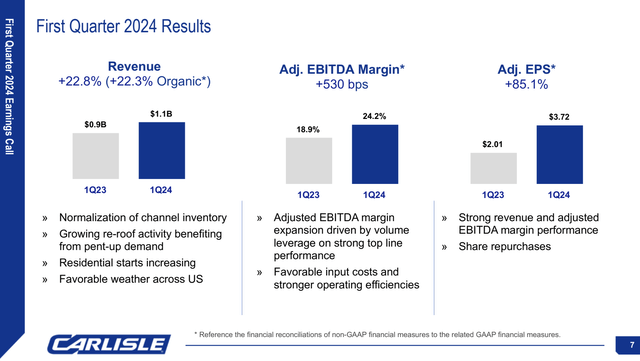

During its just-released earnings, the company reported $1.1 billion in sales, which is 23% more compared to the prior-year quarter.

This growth was driven by several factors, including the end of inventory destocking, a return to normal ordering levels, and strong reroofing activity.

Carlisle Companies

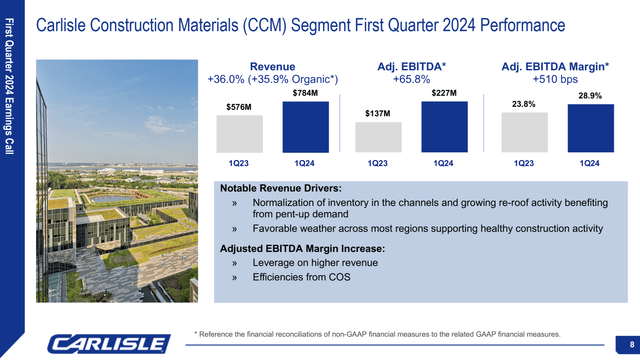

It saw significant sales growth of 36% in the CCM business segment.

Adjusted EBITDA in the CCM segment saw a significant 66% increase, reaching $227 million, with a margin expansion of 510 basis points to 28.9%.

Carlisle Companies

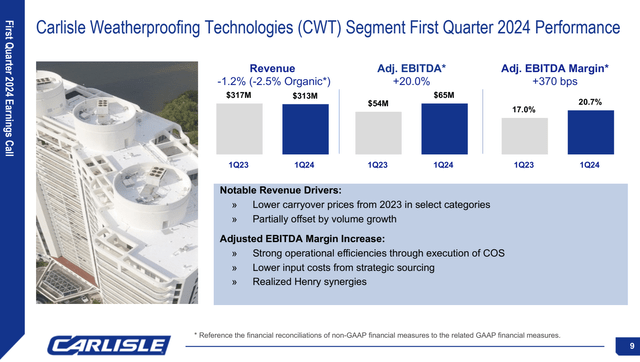

Unfortunately, revenue in the Construction Technologies segment saw a 1% year-over-year decline due to lower carryover prices in certain product categories.

The good news is that despite this mild decline, the segment managed to achieve a 20% growth in adjusted EBITDA, with an expanded margin of 20.7%. This is an improvement of 370 basis points compared to the prior-year quarter.

This improvement was attributed to operational efficiencies gained through the company’s operating system, strategic sourcing efforts leading to lower input costs, and synergies realized from recent acquisitions.

Carlisle Companies

Especially in this environment, I was very surprised to see that CSL turned 1% lower revenues into 20% higher adjusted EBITDA.

In general, the company is very upbeat about its pricing outlook for the remaining three quarters of this year, supported by successful price hikes of competitors.

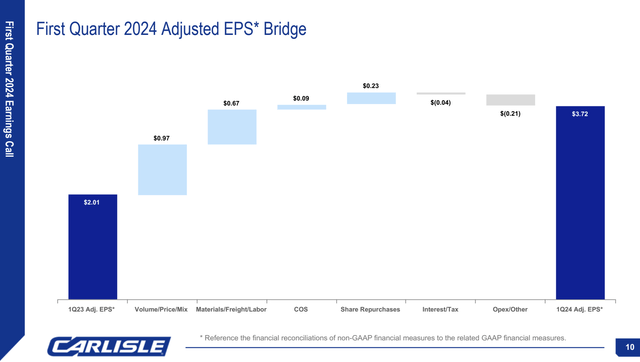

Putting all things together, the company achieved 85% year-over-year adjusted EPS growth, supported by volumes, pricing, operating costs, input costs, and share buybacks, which improve the per-share value of a business.

Carlisle Companies

Having that said, the company is looking for new M&A opportunities.

It recently sold its Interconnected Technologies business to Amphenol (APH) for roughly $2 billion in proceeds, which are used to fund new deals and buybacks. This deal also turned it into a pure-play building products provider.

Roughly $1 billion of these proceeds went to buybacks, while the company also announced the acquisition of MTL, a specialty manufacturer based in Wisconsin.

This business was bought for less than 9x EBITDA and should allow Carlisle to penetrate its target market.

MTL establishes Carlisle as one of the industry’s most comprehensive providers of architectural metal products, including “roof-to-grass” color coordinated metal building envelope solutions. MTL generated revenue of $132 million for the twelve months ended February 29, 2024. – CSL

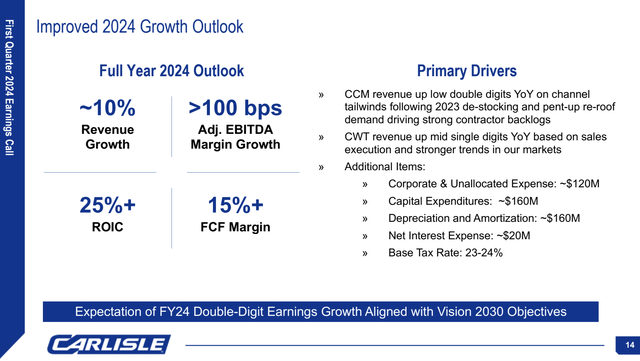

Moreover, the company revised its full-year 2024 revenue outlook upwards to approximately 10% growth over the prior year, double its initial projection(!).

This upward revision was driven by the strong performance in the first quarter and anticipated higher demand for reroofing activities for the remainder of the year.

Carlisle Companies

Even better, the company expects to grow adjusted EBITDA margins by at least 100 basis points. Its previous guidance was 50 basis points.

Shareholder Distributions And A Rosy Long-Term Outlook

As part of its success, the company bought back $150 million worth of stock in the first quarter and paid $42 million in dividends.

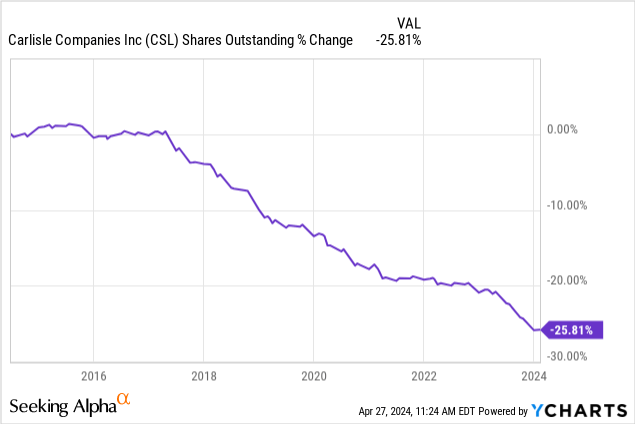

Over the past ten years, the company has bought back a quarter of its outstanding shares, which has tremendously added to its strong total return picture.

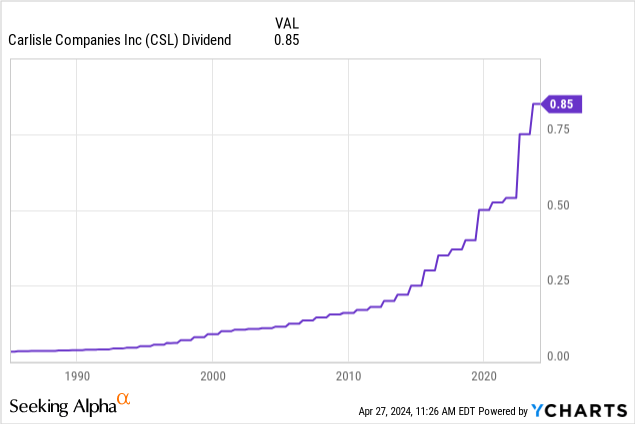

The dividend has been hiked for 47 consecutive years, which means it is just three consecutive hikes away from becoming a Dividend King!

Over the past five years, the dividend CAGR has been 16.0%, with a sub-20% payout ratio, which is very impressive. The most recent hike was 13.3% on August 3, 2023.

Unfortunately, for income-focused investors, the current yield is just 0.9%.

The good news is that the dividend yield is only so low because of its stellar stock price performance.

Carlisle can reward shareholders in line with its earnings growth because of its healthy balance sheet.

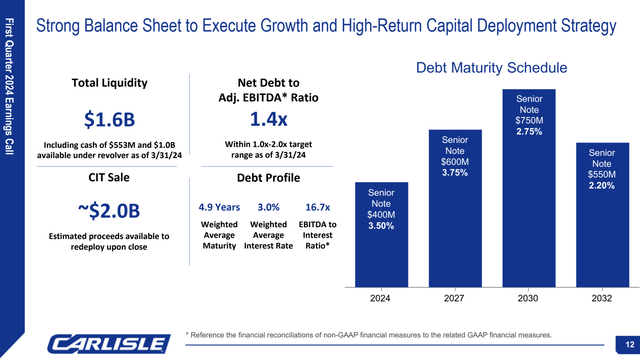

As of 1Q24, the company maintained a net leverage ratio of 1.4x, remaining within its target range of 1.0-2.0x EBITDA. It also holds $1.6 billion in liquidity, enough to service more than 90% of the debt that’s due through 2030 – technically speaking.

Carlisle Companies

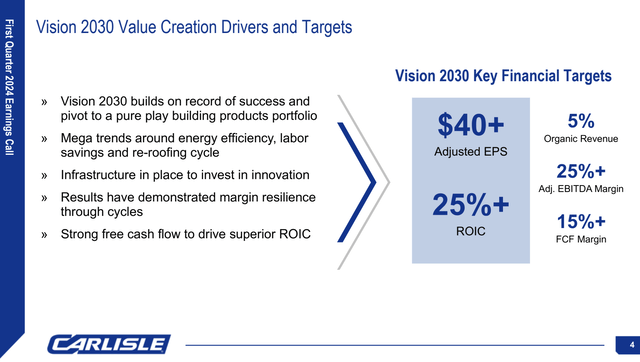

In light of everything said so far in this article – including 2024 guidance – the company is sticking to its 2030 outlook.

By 2030, the company aims to generate at least $40 in adjusted EPS, supported by 5% annual organic revenue growth, adjusted EBITDA margins north of 25%, and secular growth from megatrends in energy efficiency, labor-savings, and reroofing growth.

Carlisle Companies

This bodes well for its valuation.

Valuation

Even after its rally, CSL is still attractive.

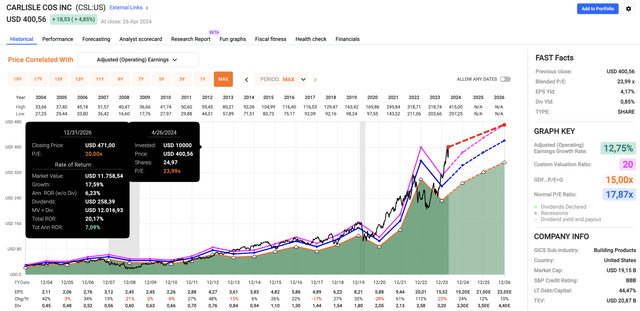

Using the data in the chart below, CSL currently trades at a blended P/E ratio of 24.0x. While this is above its long-term normalized P/E ratio of 17.9x, I believe a higher multiple is warranted.

Over the past ten years, the company has traded at roughly 20x earnings, which makes more sense. After all, it is now a pure-play building materials company with a better margin profile.

FAST Graphs

This year, analysts are looking for 24% EPS growth, potentially followed by 12% and 10% growth in 2025 and 2026, respectively.

Applying a 20x multiple to these numbers, the company has a fair mid-term price target of roughly $471, which is 18% above the current price.

On a longer-term basis, I expect CSL to double.

Its 2030 target of at least $40 in EPS implies an $800 price target (20x$40), which is almost exactly 100% above the current price. Including its dividend, investors are in a good spot to enjoy double-digit annual returns on a prolonged basis.

That’s why I will continue to buy CSL on any pullbacks.

Takeaway

With a focus on rapid growth, higher margins, and strategic mergers and acquisitions, CSL has improved its position in the building materials industry.

Despite its recent successes, the company remains poised for further expansion, driven by robust financials, a commitment to shareholder distributions, and a bullish long-term outlook.

With a track record of consistent dividend increases and a promising trajectory toward becoming a Dividend King, CSL presents an attractive opportunity for investors seeking sustainable growth and compelling returns well into the future.

Pros & Cons

Pros:

- Strong Growth Potential: CSL has shown impressive growth, with shares nearly doubling in just one year. Its focus on strategic acquisitions and operational efficiencies positions it for continued expansion.

- Steady Dividend Growth: As a Dividend Aristocrat, CSL has increased its dividend for 47 consecutive years, offering investors reliable income and a track record of shareholder value.

- Resilient Industry Position: With a market cap of $19 billion, CSL is a dominant player in the building materials industry, catering to the growing demand for energy-efficient solutions in the commercial sector.

- Robust Financials: CSL maintains a healthy balance sheet, with a net leverage ratio of 1.4x and $1.6 billion in liquidity.

Cons:

- Low Dividend Yield: Despite consistent dividend growth, CSL’s current yield of 0.9% may be unattractive to income-focused investors seeking higher yields.

- Valuation Concerns: While CSL remains attractive, its blended P/E ratio of 24.0x exceeds its long-term normalized ratio, which means it needs to show its ability to improve margins.

- Market Volatility: Like any investment, CSL is subject to market fluctuations and economic uncertainties, which could impact short-term performance.

Q1 2024 Earnings Call Transcript")