")

Investment Thesis

Calix (NYSE:CALX) delivered unappetizing guidance together with its Q1 2024 results. More specifically, I argue that in the best-case scenario, investors are eyeing up double-digit negative revenue growth rates and having to pay approximately 40x forward EPS. This is simply too expensive a valuation for Calix.

On the other hand, it should be noted that Calix holds a debt-free balance sheet, with approximately 14% of its present market cap made up of cash. And yet, I question management’s ability to adequately return this capital to shareholders.

All in all, this stock is a sell, before things get even worse.

Calix’s Near-Term Prospects

Calix provides technology and services that help broadband service providers deliver better experiences to their customers. They offer a range of solutions, including platforms and cloud services, which make it easier for these providers to manage their operations.

In the near term, Calix confronts a few challenges. One pressing issue is the uncertainty surrounding customer decision-making regarding funding sources, such as BEAD or other governmental programs. This indecision hampers the company’s outlook and ability to plan inventory levels effectively. Additionally, the reduction in lead times to customers adds further complexity by diminishing visibility into future sales trends. This challenge is compounded by shifts in customer investment priorities, with some extending their sale cycle or redirecting resources towards subscriber acquisition rather than network expansion.

Also, while Calix continues to demonstrate robust growth in its platform, cloud, and managed services, the company faces headwinds in the appliance (hardware systems) portion of its business. The evaluation and adjustment of spending plans by some customers has led to a prolonged sales cycles.

Moreover, the trend of customers concentrating on adding new subscribers within existing network builds rather than aggressively expanding new networks poses a challenge to Calix’s growth strategy in the short term.

Given this background, let’s now delve into its financials.

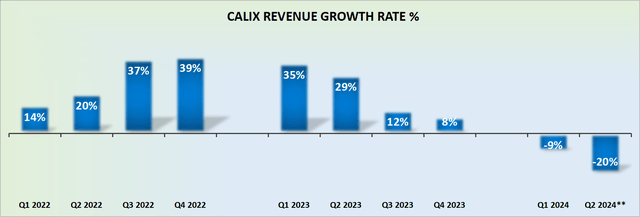

Revenue Growth Rates Fizzle Out

CALX revenue growth rates

The fact that Calix marginally missed analysts’ expectations for Q1 2024 undoubtedly weighed on the stock, but investors would have probably shrugged this off in a few days or around a week, provided that Calix’s guidance would have been somewhat similar to what the Street had been previously expecting as the company headed into this earnings report.

Incidentally, looking back to Calix’s previous Q4 2023 results, this is what management had stated:

We currently expect this will mark the low point for the year and believe we will grow sequentially thereafter. (emphasis added)

But this wasn’t to be. In fact, analysts following Calix had been expecting to see around negative 11% y/y revenue growth rates in its guidance for Q2 2024. However, naturally, investors would have liked, or even expected, to have been positively surprised and for Calix’s guidance for Q2 to have been guided towards a negative 8% y/y.

What investors had not expected to see was for Calix to guide to be down approximately 20% y/y in Q2 2024. Moreover, this figure already takes in the high end of its revenue target and adds a little more on the assumption that management is being conservative.

In other words, negative 20% y/y growth for Q2 is the absolute best-case scenario. With room for an even worse quarter to be delivered in 90 days.

Given this context, let’s now delve into its valuation.

CALX Stock Valuation – 40x Forward EPS

Here’s where matters get slightly complicated. The fact of the matter is that it’s not all bad with Calix. Indeed, Calix’s balance sheet is impressively clean, with $230 million of cash and equivalents and no debt. Hence, this means that approximately 14% of its market cap is made up of cash (including premarket sell-off).

But this element also plays a role in Calix’s future valuation. Consider this, management had been actively repurchasing its shares throughout 2023. Case in point, during 2023, Calix repurchased approximately $86 million worth of stock at prices higher than $35 per share. Accordingly, given that the share price today is $25 per share, many shareholders will be frustrated with management’s poor capital allocation strategy. Hence, how much is that cash on Calix’s balance sheet actually worth, if management has had a poor track record of being astute capital deployers?

Moving on, according to my estimates, Calix may be able to over the next twelve months reach around $0.60 of non-GAAP EPS per share. That’s a generous estimate that presumes that its prospects rapidly improve from Q2 2024. This leaves the stock priced at 40x forward EPS. Hardly a cheap stock.

The Bottom Line

In conclusion, despite Calix’s impressive balance sheet with a debt-free status and a significant portion of its market cap represented by cash reserves, the current valuation remains unattractive. With a forward EPS multiple of approximately 40x, the stock is overpriced, especially considering the challenging revenue growth outlook.

While the company’s past share repurchase initiatives reflect a commitment to returning capital to shareholders, with the share price now meaningfully below those repurchase, it forces questions about management’s capital allocation strategy.

In sum, this stock isn’t worth buying the dip.

")