for $2 Billion, Tether (USDT) Increases Investment in CityPay, Does Rollblock (RBLK) Have The Potential To Surge 1200%")

")

Abeona Therapeutics (NASDAQ:ABEO) is a gene therapy company based in Cleveland, Ohio. The company’s lead product candidate is Pz-cel, a gene therapy for recessive epidermolysis bullosa, RDEB.

Pz-cel has shown higher efficacy than the competition in larger skin lesions in RDEB.

Epidermolysis bullosa (EB) is a genetically heterogeneous skin disorder characterized by increased skin fragility. Dystrophic EB is a variant of EB associated with blistering skin lesions. The disease is inherited as either autosomal dominant or recessive. The U.S. prevalence of the recessive DEB, RDEB, is 3850 patients.

The current treatment for RDEB involves treating skin lesions, such as dressing and treating infections. Recently, Krystal Biotech (KRYS) received FDA approval for its gene therapy, Vyjuvek, which can treat both dominant and recessive DEB.

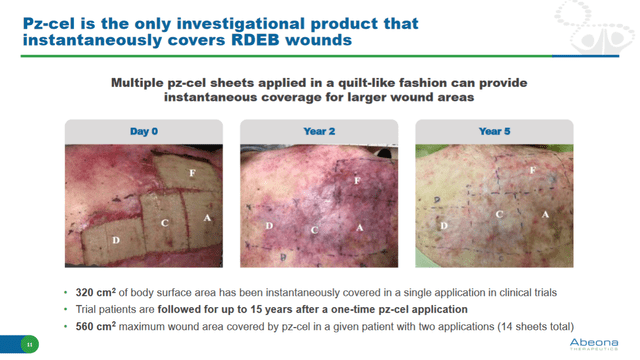

Compared to Vyjuvek, Pz-cel has the advantage of being efficacious against large skin lesions, even >500 cm2 in size. It also has the advantage that multiple Pz-cel sheets can be used in a quilt-like fashion for instantaneous coverage of larger wounds. In clinical trials, 320 cm2 of skin wounds have been covered in a single application. The maximum wound area covered by Pz-cel was 560 cm2 using two applications (14 sheets).

Pz-cel efficacy in large skin wounds in RDEB (Investor presentation)

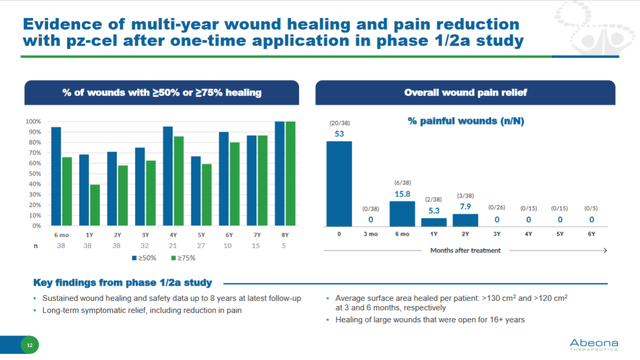

In a Phase 1/2a study, 100% of skin wounds showed >=75% healing at a long follow-up of 8 years.

Long-term efficacy of Pz-cel in wound healing in RDEB after one application (Investor presentation)

The recent CRL is resolvable and the dip in the stock is a good buying opportunity

Despite showing excellent efficacy in treating its target RDEB skin lesions with no major safety issues, the FDA recently issued a complete response letter, CRL, to Pz-cel’s application for approval. The FDA, however, did not ask for any new studies and did not raise any questions about the therapy’s efficacy or safety. Gene therapy manufacturing is a complex process, and the FDA’s CRL is related to manufacturing issues. The company considers these issues to be resolvable and anticipates submitting a response to the FDA by the third quarter of this year.

Usually, the time period from submitting a response to the FDA for CRL and the FDA’s decision is an average of 2 months. I am bullish that the FDA will accept the revised BLA sometime in Q4 this year and assign a PDUFA date after six months of review (around mid-2025). This would translate to around a year and a quarter’s delay in the drug’s commercial launch due to the recent CRL.

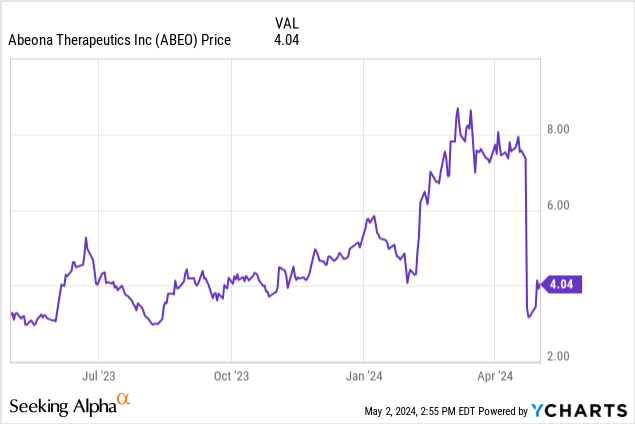

The stock fell 50% after the approval, and the company has a current enterprise value of just $42 million. The management’s estimate of Pz-cel’s peak annual revenue five years after launch is $500 million. The company has identified 1200 RDEB patients in the U.S. and expects two treatment cycles per patient. If Pz-cel is priced similarly to the rival KRYS gene therapy ($630,000/year), it could be a $1.1 billion/year U.S. revenue opportunity at 100% of the market (1200*2*630000*0.74, input price = 74% of wholesale price of $630K per treatment cycle per patient in line with Pharmagellan guide). At 50% of the market share, Pz-cel could gain $500 million/year in peak U.S. revenue, which aligns with the management’s estimates.

To evaluate Pz-cel in RDEB, I used a discounted EV/sales method. I expect Pz-cel to launch in the U.S. in 2026 and reach peak sales five years after the launch in 2031 (in line with the management’s estimate for reaching peak revenue). Biotech companies usually trade at an enterprise value/sales of 6 (NYU-Stern data from Damodaran). This would translate into the company reaching an enterprise value of $3 billion in 2031. Currently, I assign a 90% probability of approval (in line with the Pharmagellan guide). Using a discount rate of 15% at its current stage (in line with the Pharmagellan guide), this would translate into a fair value of $1 billion for Pz-cel in RDEB (500*6*0.9)/(1.15^7), which makes its current enterprise value of just $42 million undervalued.

Sell-side analysts have supported the stock after the CRL. Cantor Fitzgerald issued a $36 price target on the stock after the CRL (current stock price is $3.44). This update to the stock is in line with my calculations.

The current cash reserves are expected to be $42 million (including short-term investments) at the current operating cash burn rate of around $36 million in the last four quarters. I expect the cash reserves to be an adequate cash runway until the revised PDUFA in mid-2025. There is no long-term debt.

In conclusion, I consider Abeona Therapeutics to be an excellent contrarian biotech idea for patient investors with the potential for significant upside.

Risks in this investment:

These include repeat FDA rejection for issues not anticipated at present, and failure to gain market share after approval. Investing in biotech/pharma sector is risky and may not be suitable for all investors. This note represents my own opinion and is not professional investment advice. Please conduct your own due diligence or consult your financial advisors before making any investment decision.

")