")

")

Investing doesn’t have to be a popularity contest, and in reality, buying quality names that are temporarily beaten down in price can produce terrific results, especially if they pay a high dividend yield.

Such may be the case these days with REITs and income stocks in general, which continue to trade near their 52-week lows despite the broader market indices flying near all-time highs.

This brings me to Broadstone Net Lease (NYSE:BNL), which I last covered in May of last year, noting the attractiveness of its 7% yield at that time and solid portfolio profile including its high occupancy.

The stock has since fallen by 5.5% since my last piece (-0.2% total return including dividends) and at the current price of $15.44, it currently sits below its IPO price of $16 from back in 2020, as shown below.

Seeking Alpha

In this article, I revisit BNL with key updates on business fundamentals and portfolio transformation and discuss why now may be a great time to pick up this name for high yield while it’s out of favor with the market, so let’s get started!

Why BNL?

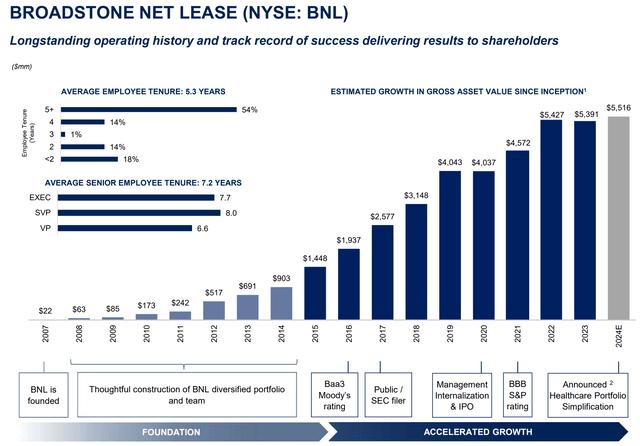

Broadstone Net Lease is self-managed and is one of the newest publicly-traded net lease REITs on the block. It has a diverse portfolio of 796 net leased properties that are spread across 44 U.S. States and Canada (7 properties in 4 provinces). As shown below, BNL has grown its property portfolio significantly since its founding in 2007, although growth has slowed since the start of 2023 due to higher cost of capital.

Investor Presentation

It also has a long weighted-average lease term of 10.5 years, putting it on par with most other net lease REITs, and gets financial reporting from 94% of its tenants, thereby enabling BNL to address tenant issues before they become bigger worries.

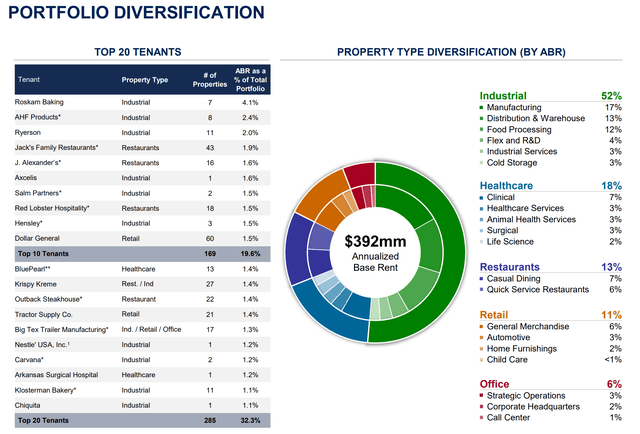

One of the advantages of being a recently formed REIT is that BNL is able to craft a portfolio that fits with the times. This includes having high exposure to fast-growing industrial properties, which comprise just over half (52%) of BNL’s annual base rent. As shown below, healthcare (18%), restaurants (13%), retail (11%), and office (6%) make up the remainder of BNL’s portfolio.

Investor Presentation

Meanwhile, BNL continues to enjoy a high leased rate of 99.4% as of the end of Q4’23, of which results were released on February 21st. This is on par with that of other quality net lease REITs like Realty Income Corp. (O), and is unchanged since when I last visited the stock after its Q1’23 results. BNL also made strategic investments during Q4, including $64 million in 3 industrial properties and 2 restaurant properties.

The new properties came with a weighted average lease term of 12.7 years, which sits longer than the aforementioned 10.5-year portfolio average, and came with an attractive weighted average cap rate of 7.5%. These acquisitions were funded in part by portfolio dispositions on 5 properties for $16.5 million, which had a lower cash cap rate of 6.7%, thereby implying an 80 basis points investment spread on the recycled capital.

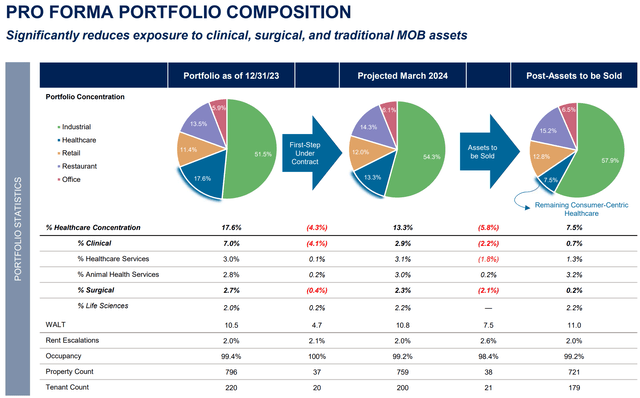

Looking ahead, investors can expect a material change in BNL’s property portfolio over the next 12 months, as management seeks to reduce its exposure to healthcare properties. This may be a smart move, considering that the healthcare segment is more nuanced than other property sectors, thereby requiring more specialized knowledge to be successful.

At present, healthcare represents 18% of BNL’s total ABR, and 75 healthcare assets representing 11% of ABR have been identified for sale. Half of that number (37 properties) are under executed contract to sell during the first quarter of this year alone with the remainder of these healthcare asset sales being targeted to close by the end of this year.

As shown below, BNL’s Pro Forma healthcare property composition is expected to decline from 17.6% to 7.5%, while industrial properties are expected to rise from 51.5% to 57.9% by the end of this year.

Investor Presentation

Risks to BNL include execution risk related to the aforementioned portfolio change, as this could result in near-term dilution to the bottom-line FFO/share should it take longer than expected to redeploy capital. Moreover, there’s no guarantee that BNL would be able to deploy capital at the same cash cap rates as that of the disposed healthcare properties, and that also presents earnings dilution risk to the bottom line.

Over the next few quarters, I would look for BNL’s progress towards capital redeployment and whether if it’s able to achieve cash cap rates over 7%, which is what I would view as being ideal and on par with what it achieved on new property acquisitions during Q4’23. In addition, I would also look for favorable interest rates due to the Fed’s stated goal of 3 rate cuts this year, which could reduce BNL’s cost of debt for new property acquisitions.

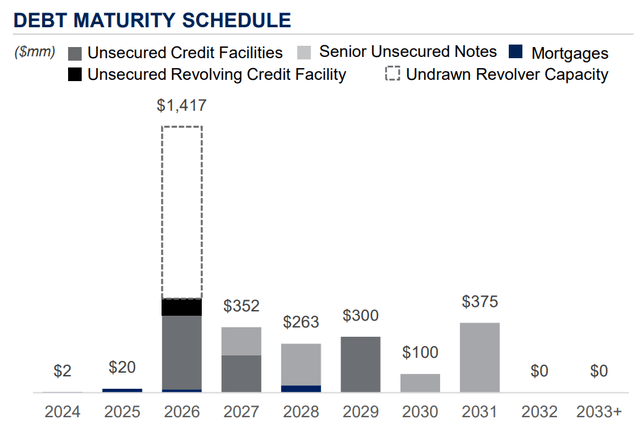

Importantly in this higher rate environment, BNL carries a strong balance sheet to support its portfolio transition. This includes BBB/Baa2 credit ratings from S&P and Moody’s and $929 million of liquidity. BNL also carries a safe net debt-to-EBITDAre ratio of 5.0x and a strong fixed charge coverage ratio of 4.5x. As shown below, BNL has minimal debt maturities between now and the end of 2025.

Investor Presentation

As for income investors, BNL sports a 7.4% dividend yield, which sits well above that of peers like Realty Income and W.P. Carey (WPC). The dividend is also covered by a 77% payout ratio, leaving some retained capital to fund growth.

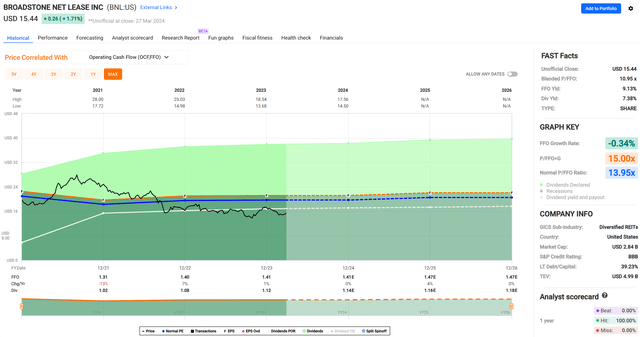

Turning to valuation, I continue to find BNL to be appealing at the current price of $15.44 with a forward P/FFO of 10.4, which sits cheaper than the 10.8 P/FFO from when I last visited the stock. At this valuation, BNL sits cheaper than its closest peer (by property composition) WPC, which carries a forward P/FFO of 11.9. As shown below, BNL also currently trades below its normal P/FFO of 13.95.

FAST Graphs

I believe BNL remains undervalued by the market because income stocks remain out of favor compared to growth stocks. In addition, the market is pricing in lower growth for BNL has higher interest rates and a lower share price raises BNL’s cost of capital to fund acquisitions. Nonetheless, BNL has 2% average rent escalators on its portfolio and could resume external growth should interest rates come down. In the meantime, investors are paid a well-covered 7.4% yield to wait for BNL’s growth prospects to turn around.

Investor Takeaway

Overall, BNL remains a solid choice for income investors seeking exposure to the net lease REIT sector. It has high exposure to industrial properties and this segment should grow as BNL seeks to dispose of its healthcare real estate exposure. It currently offers an attractive 7.4% dividend yield and has a strong balance sheet to support future growth should opportunities arise. While there are some risks involved with its portfolio transition and interest rate environment, I believe that BNL’s current valuation provides an attractive entry point for long-term investors, who are well-paid during this transition period for the REIT. As such, I maintain a ‘Buy’ rating on BNL.

")

Q1 2024 Earnings Call Transcript")

")