Q2 2024 Earnings Call Transcript")

")

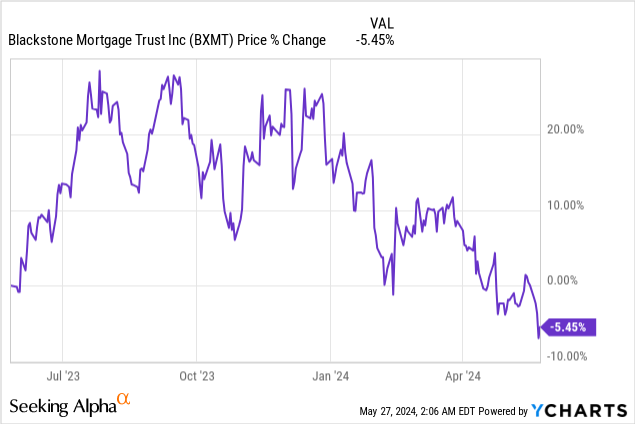

Shares of Blackstone Mortgage Trust (NYSE:BXMT) just hit a fresh 1-year low as the market seems to come to terms with the shock that the mortgage REIT could lower its dividend due to continual loan problems in its portfolio. Blackstone Mortgage Trust’s loan problems, especially in the office segment, have been the key reason why the REIT did not support its dividend with distributable earnings in the last quarter. I believe that Blackstone Mortgage Trust is now headed for a dividend cut in the next several quarters. Given that shares are already priced at a large discount to book value, I believe the price impact of a dividend announcement could be relatively small, however!

Previous rating

A quarter ago, I rated shares of Blackstone Mortgage Trust a hold as the REIT experienced headwinds in its office loan portfolio in previous quarters, resulting in a decline in the percentage of performing loans: 3 Reasons Why I Am Downgrading This 12% Yielder. Blackstone Mortgage Trust was forced to increase its CECL reserve drastically in Q1’24 and the REIT did not support its dividend with non-adjusted distributable earnings. For those reasons, I now expect that Blackstone Mortgage Trust could cut its dividend, possibly by 10-20%, in FY 2024.

BXMT moves into unchartered territory, dividend cut now likely

Blackstone Mortgage Trust’s balance sheet quality deteriorated further in the first fiscal quarter, and problems continue to be concentrated in the REIT’s office loan portfolio.

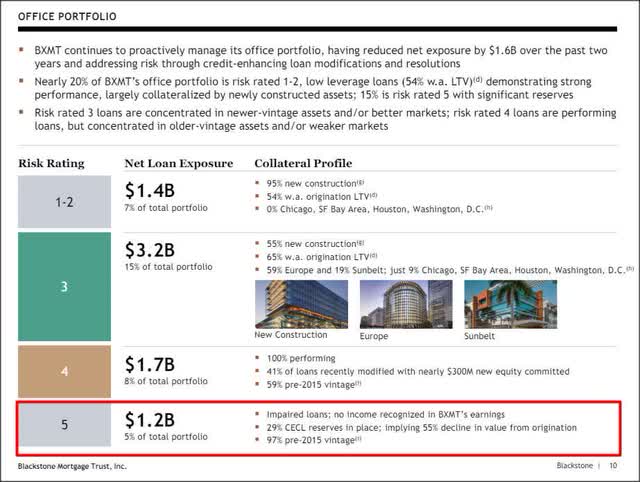

A full 5% of the office segment — which is the second-largest segment for BXMT with a net loan exposure of $5.5B (26% of total) — are impaired, which strongly indicates that the mortgage REIT will continue to write down the value of some of its office loans in the coming quarters as well. On the other hand, multi-family investments, which represent the largest net loan exposure of $5.8B (27% of portfolio total), were 100% performing. Only 92% of total loans were performing in Blackstone Mortgage Trust’s portfolio in Q1’24, which is down from 93% in the previous quarter.

BXMT

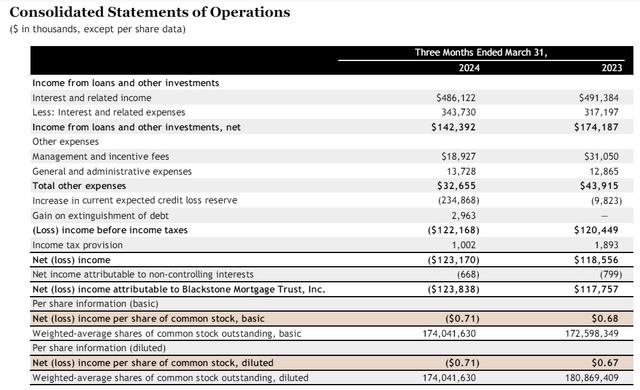

As a result to the continual loan issues in the office sector, Blackstone Mortgage Trust was forced to add to its current expected credit loss reserve, also known as CECL, a trend that has been going on for a while: the REIT increased its CECL reserve by a massive $234.9M in the March quarter… which represented a near 24-fold increase compared to the year-earlier period.

Office landlords in big cities suffer from rising office vacancies that are driven in part by work-from-home arrangements that were established during the COVID-19 pandemic. With office occupancy rates under pressure, investors in mortgages are seeing a rising number of loan charge-offs… the kind that caused Blackstone Mortgage Trust to report a serious decline in its distribution coverage ratio in Q1’24.

BXMT

This increase in the CECL reserve specifically led to a serious deterioration in the REIT’s distribution coverage in the first fiscal quarter, and Blackstone Mortgage Trust did not support its dividend of $0.62 per-share with distributable earnings.

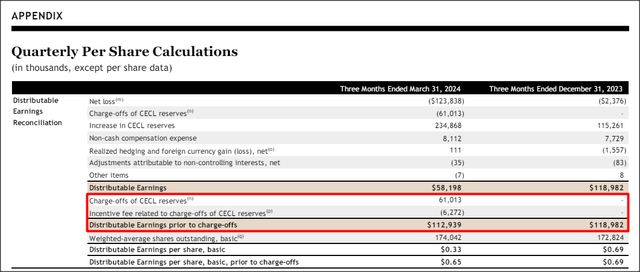

The REIT generated only $0.33 per-share in Q1’24 in (non-adjusted) distributable earnings from its loan portfolio. This means that the mortgage REIT underearned its $0.62 per-share dividend with distributable earnings by a massive 47%. As a result, the distribution coverage ratio in the first fiscal quarter was only 53% compared to 111% in Q4’23. On an adjusted basis, Blackstone Mortgage Trust’s distribution coverage ratio was still 105%, but some investors would describe the change in the coverage profile as concerning. The trend here is not a good one, and the significant deterioration in coverage due to BXMT’s loan charge-offs suggests that the REIT may respond with a dividend cut in FY 2024.

BXMT

Is a dividend cut priced in now?

Shares of Blackstone Mortgage Trust fell to a new 1-year low last week, which indicates to me that dividend investors are starting to be a bit more realistic when it comes to the possibility of a dividend cut. The fact that Blackstone Mortgage Trust’s distribution coverage ratio fell to just 53% on a non-adjusted basis in Q1’24 increases the probability that income investors will see a dividend cut in the next 1-2 quarters, in my opinion.

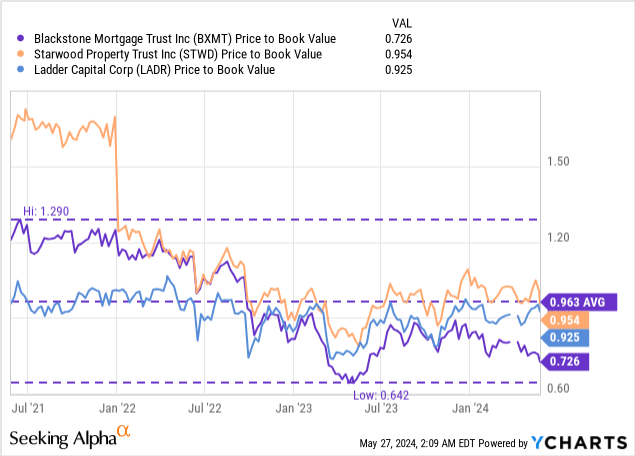

The question is to what extent is a possible dividend cut already reflected in Blackstone Mortgage Trust’s valuation. The REIT’s shares are trading at a 27% discount to book value, which is by far the highest in the industry group. Starwood Property Trust (STWD) and Ladder Capital (LADR) are priced at 5% and 7% discounts to book value, largely because they are more diversified and have stronger balance sheet quality (I discussed Starwood Property Trust here and Ladder Capital here).

Blackstone Mortgage Trust’s 27% discount to book value really stands out here given the concerns about dividend sustainability and the REIT’s share price is unlikely to return to book value in the short term, at least not as long as the REIT’s portfolio is plagued by loan problems.

Blackstone Mortgage Trust’s book value in Q1’24 was $23.83, showing a 5% quarter-over-quarter decline. I believe Blackstone Mortgage Trust will be priced at a sizable discount in the near future, especially if the REIT cuts its dividend down to a more manageable level. In my opinion, a 10-20% dividend cut may be realistic to give the REIT breathing space to work out its loan problems.

From a valuation and dividend risk point of view, I would need a discount from BXMT, however: I would have to get a relatively high 20% discount to book value (fair value $19.10 per-share) at this point of the credit cycle to take a risk on BXMT. With a 27% discount present right now, I believe shares of BXMT are actually slightly undervalued. This, however, does not mean that the share price cannot drop further if the REIT indeed realigns its dividend.

Risks with Blackstone Mortgage Trust

Obviously, the biggest risk right now is that management will cut its $0.62 per-share quarterly dividend, which in all likelihood would have a negative impact on the REIT’s valuation factor. What would change my mind about Blackstone Mortgage Trust are two things: 1) The loan quality situation in offices doesn’t deteriorate further or potentially reverses, and 2) The REIT avoids a dividend cut despite the severe drop-off in Q1 non-adjusted distributable earnings.

Final thoughts

Blackstone Mortgage Trust, in my opinion, is likely headed for a dividend cut in FY 2024 as the REIT continues to struggle with loan quality problems, especially in its office segment. It doesn’t help that offices are the second-biggest investment group for Blackstone Mortgage Trust, after multi-family real estate. The increase in the CECL reserve in Q1’24 was a nasty surprise because it directly led to a drop-off in the company’s important distributable earnings figure. As a result of the reserve increase, Blackstone Mortgage Trust underearned its dividend by a whopping 47% in Q1’24. This does not bode well for dividend sustainability, in my opinion, and income investors at this point have to expect for the REIT to announce a dividend cut in FY 2024.