")

Investment Thesis

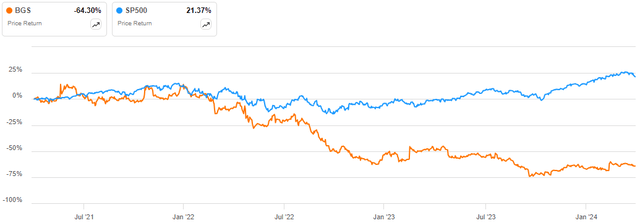

B&G Foods, Inc. (NYSE:BGS) has been on a downward trajectory, losing about 64.30% over the last three years and underperforming the S&P 500 by a margin of 85.67%.

Seeking Alpha

I largely attribute the company’s dismal performance to its poor financial health characterized by net losses and a high debt burden. However, despite the underwhelming performance, the company is adopting strategic measures to turn around its woes and positive signs are coming from the initiatives.

Although I am optimistic about its strategic moves, I am neutral on this stock because based on technical analysis, it has bottomed, and it is yet to show a trend reversal by crossing above the $17 price range which I consider as the buy and bullish confirmation mark as will explain later. Further, its strategic initiatives are yet to turn around the company’s setbacks, and therefore we need patience until the companies at least exhibits consistent positive net income or its debt load is significantly reduced. Until these conditions are met, I recommend patience here.

Company Overview

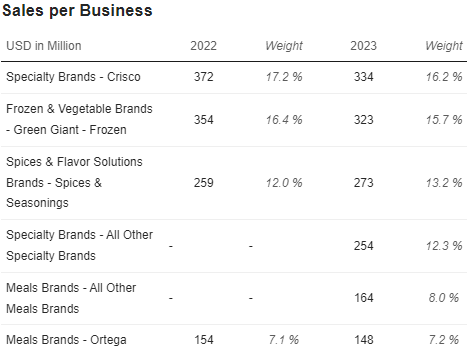

BGS produces and distributes branded shelf-stable and frozen food products in the US, Puerto Rico, and Canada. The company has a very diverse product portfolio made up of more than 50 brands. Below is a breakdown of the revenue contribution of its major brands for the 2022 and 2023 FYS.

Market Screener Market Screener

With such a diverse product range, BGS has been in business for more than 125 years, and it employs more than 2500 people. From this brief company profile, I have some observations which I believe I should share. First off, the company is very diverse, which is very healthy because it can help mitigate financial risk in the case of economic downturns by leveraging different market segments and capitalizing on the best-performing segment to cushion poorly performing segments. In addition, I believe its broad product offering contributes to its brand strength by building a robust visibility, which is essential for market presence. Another reason why I am pleased by its diversity is that with such a wide range of products, BGS has a higher potential to reach new markets and segments, something I believe can encourage customer satisfaction and loyalty as consumers are more likely to buy multiple products from a brand they trust.

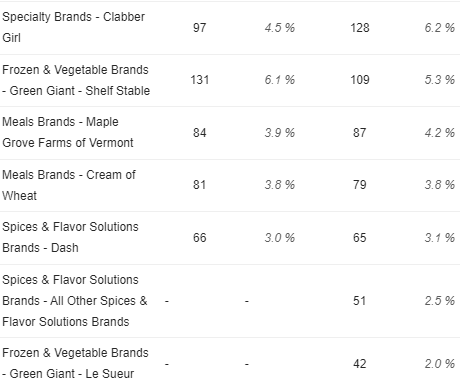

Even though I am attracted by the company’s broad product range, I also find weakness in it. The first weakness is product cannibalism. This is a case where closely related products compete against each other in the market. For example, within its offering, the company has Green Giant (frozen) and Le Sueur. Both brands are canned vegetable products, which implies that they are offered in the same market segment, hence competing against each other. In 2023, Le Sueur’s revenue contribution of 2% up from the reported none in 2023 saw Green Giant (Frozen) revenue decline by 8.78% and the Green Giant (shelf-stable) revenue decline by 17.16%, a clear demonstration that these three products are competing against each other.

The other weakness is increased costs. Different products have different marketing strategies and this could lead to inflated marketing costs. For example, different marketing campaigns tailored for a brand like Mrs. Dash and Back to Nature require separate budgets, which can translate to inflated overall expenses. I believe this is one if not the major reason as to why the SG&A expenses have increased from $152.9 million in 2018 to more than $196 million currently.

In a nutshell, BGS’s diversified business model has a lot of benefits, which I believe serves as its competitive advantage. However, it also has some drawbacks, but I think with its strategic initiatives, especially the disposal of some product lines, the company may tame what appears to me to be over-diversity to a manageable range which will be easily manageable, hence mitigating the above weakness to a greater extent.

Financial Health

One of the dark sides of BGS is its poor financial health, which, I believe, is the major reason behind its awful stock performance over the last couple of years. To begin with, the company has an awful 3-year CAGR both in its top and bottom lines as exhibited by revenue, EBITDA, and normalized net income values of 1.57%, -3%, and -18.21% respectively. This can be simply classified as a poor or rather weak financial performance which mostly culminates with bearish market sentiments and eventually low stock valuation and there is no surprise the stock has slumped over the last couple of years.

To add to its weak financial health is its weak balance sheet. With a total debt of $2.12 billion and a total equity of $835.5 million, it translates to a debt-to-equity ratio of 2.54 which is way above the recommended leverage of 1. This translates to a high debt risk, which isn’t pleasing to investors. Besides its high leverage, BGS has a weak interest coverage of 1.6 which shows that it may struggle to cover its interest expenses with its EBIT.

With its long-term liabilities of $2.02 billion covered 0.39x by its current assets, the company’s solvency is very precarious. This can be further supported by its weak debt coverage by its operating cash flow of $247.76 million which covers its total debt by about 11.7% which is a very weak coverage.

Given this weak financial health, I expect a low investor confidence in this company perhaps in the short and medium term until the financial health improves. In addition, Due to its weak financials, BGS has consistently cut its annual dividend from $1.90 in 2021 to $0.76 in 2023 and the potential for other cuts is likely because its payout ratio of 76.77% is high for this struggling company and especially when compared to the sector median payout ratio of 48.46%. Further, with such a high debt, this company lacks financial flexibility, something which means that the company is vulnerable to unforeseen macroeconomic adversities which is a great risk.

Based on this background, I think this stock’s short-term and midterm outlook is not appealing and therefore investors need to exercise patience here as the management works around turning things around.

Turn Around Initiatives

It is no doubt that BGS’s financial health is weak, characterized by weak profitability and high debt levels, as discussed in the above section. However, the management appears to be working to restore stability through several strategic initiatives, some of which I will discuss in this section.

Among the initiatives adopted are selling its Green Giant US shelf-stable vegetable product line, and reshaping its product portfolio among other measures while focusing on debt reduction. Let’s dive deeper into some of these initiatives. Firstly, I will focus on the Green Giant product line sale to Seneca Foods Corporation in November 2023. This strategic decision was in line with the company’s goal of divesting its non-core product lines to focus on high-margin and growth segments while reducing its debt. Below is a quote from the company CEO on this move.

BGS Website BGS Website

I am supporting this move for two major reasons, alongside the company’s intention to reduce debt with the proceeds from the deal. The first reason is my earlier worry about product cannibalism. In the opening sections of this article, I expressed my view of its diversity and one of its weaknesses was product cannibalism, where I had cited this specific product line as an example. Interestingly, this has been mitigated through the sale of one of the similar products, which means that the company will focus on the other products and therefore enhances their visibility and market presence. I view this ongoing plan of divesting the non-core product line as a deliberate attempt to scale down what I had termed as an over-diversified business to a more manageable and efficient organization something I believe will bring sustainable growth because the efficient allocation of resources will be improved as well as reducing debt through the proceeds of such product line sales.

The other reason why I am supporting this move is that by scaling down the business, BGS will concentrate its resources and efforts in areas of high potential for growth and profitability, while managing its liabilities more efficiently.

Another turnaround strategy is innovation through a strategic partnership with Sazerac. In August 2023, BGS was very innovative through the launch of licensing seasoning and grilling blends under the Buffalo Trace, Fireball, and Southern Comfort brands. I believe this innovation is an excellent move because the seasoning blends are non-alcoholic, which makes them accessible to a wider audience while still capturing the iconic flavor of the respective spirits. In addition, the new seasonings are designed to offer consumers unique familiar flavors to increase their culinary experiences.

In other words, this innovative move is aimed at offering a unique customer experience, a move which I believe signifies the company’s deliberate attempt to improve its customer satisfaction. Generally, the move signifies the company’s strategic effort to innovate within its product line to cater to evolving consumer tastes while maintaining market relevance. In my view, this will increase customer loyalty, market penetration, and customer satisfaction, something which bodes well for the company’s future growth. It is interesting to see that the company is adopting these measures when the market trends are favorable with the healthy food market size projected to grow with a CAGR of 8.05% by 2032, a market potential I believe BGS can exploit by its diverse portfolio and innovative products.

To summarize this section, BGS is strategically seeking growth in high-growth potential and margin segments while scaling down through the sale of its non-core business while paying down debt. This move is aimed at deleveraging, and achieving high margins and efficiencies. While the full benefits of these initiatives may take time to be seen. Let’s see what the early signs look like.

In terms of improvement in margins, BGS saw an increase of 130 bps in adjusted gross margin in Q4 2023, signifying that its profitability is improving. Further, the company reduced its net debt by $335 million in 2023, signaling the company’s commitment to deleveraging and disciplined debt management. Interestingly, BGS registered much improved net cash from operation of $248 million in 2023 up from $6 million the previous year. In my view, this signifies the company’s improving operational efficiency.

Given this background, it appears that the company could be on the right trajectory, but we need to see consistency in this path. Despite the positive signs, I still say that patience is needed here because the company still has a significant debt load and profitability challenges which, unless they improve substantially, the upside will likely remain constrained. As for me, I will consider this stock when the debt to equity ratio is below 2x and consistently improving and the company is above breakeven for at least 6 consecutive quarters. Until then, I am patient as I monitor the positive progress.

Justifying A Hold Decision Based On The Price Movement

Alongside fundamentally arriving at a hold decision, this stock is also a hold from a technical standpoint. From the price chart, it is clear that this stock has bottomed, and it is currently at its strongest support level since 2008. However, at its current price, I expect a consolidation phase with the marked support zone as the company improves its fundamentals. The consolidation may go as high as $15.33 which is the lower band of my buy entry point or the bullish confirmation point as shown below. Looking at the price currently, it is within the level where I expect consolidation to take place and therefore a hold decision is justified.

Trading View

In the event the bulls take charge and a trend reversal happens, I see a good entry point to be between the $15.33-$18.98 ranges, which were the breakout levels for the previous upward rallies. This buy decision should be accompanied by my marked price targets, as shown in the above chart. However, after achieving the first price target at about $36.69, I expect a pullback to about $29.52 as cautious investors close profits after the stock hits the mid-resistance zone before the upward rally resumes to the next resistance zone at about $51.42.

It should be noted that I am projecting the above target prices with the assumption that the company’s turnaround pays off through a low leverage level and improved financial leverage backed by consistent growth in its financials. Otherwise, as it stands, hold.

Conclusion

In conclusion, BGS is currently implementing turnaround measures which appear to be potentially fruitful. However, the company has to turn around its profitability and debt burden challenges before we consider this stock. From a technical standpoint, the stock has bottomed, but a buy signal is not yet achieved. My buy entry point is between $15.33-$18.98 with price targets at $36.69 and $51.42. However, the fundamentals are currently weak, and I expect the stock to enter a consolidation phase as the fundamentals improve. Given this background, this stock is a hold as we wait for the buy confirmation.

Q2 2024 Earnings Call Transcript")

")

")